Coconut Oil Market Summary

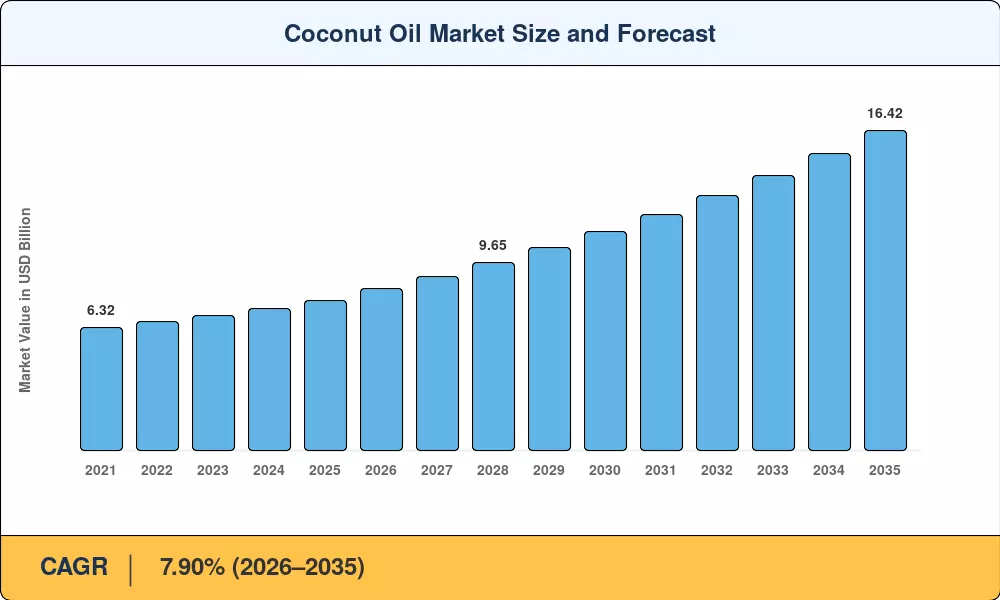

The global Coconut Oil Market reached a valuation of USD 7.68 billion in 2025 and is projected to grow from USD 8.29 billion in 2026 to USD 16.42 billion by 2035, registering a CAGR of 7.90% during the forecast period (2026–2035). Rising consumer demand for clean-label fats in packaged food products and accelerating adoption across pharmaceutical excipient applications are driving this trajectory. The Philippine Coconut Authority's 2024 replanting initiative, which earmarked PHP 6.2 billion for hybrid seedling distribution, exemplifies the kind of supply-side policy intervention that is stabilizing raw-material access and reinforcing confidence across the Coconut Oil Market value chain [1].

Processing technology across the Coconut Oil Market is undergoing a meaningful shift. Traditional copra-drying kilns and expeller-press setups are steadily giving way to centrifuge-based and enzyme-assisted cold-press lines capable of preserving higher lauric acid content at a commercial scale. Indonesia's Ministry of Agriculture co-funded a USD 48 million downstream processing modernization program in 2024, targeting small-holder cooperatives and mid-size refiners in Sulawesi and North Maluku [2]. These investments are improving extraction yields by 12–15% while meeting the purity thresholds demanded by European and North American organic retailers.

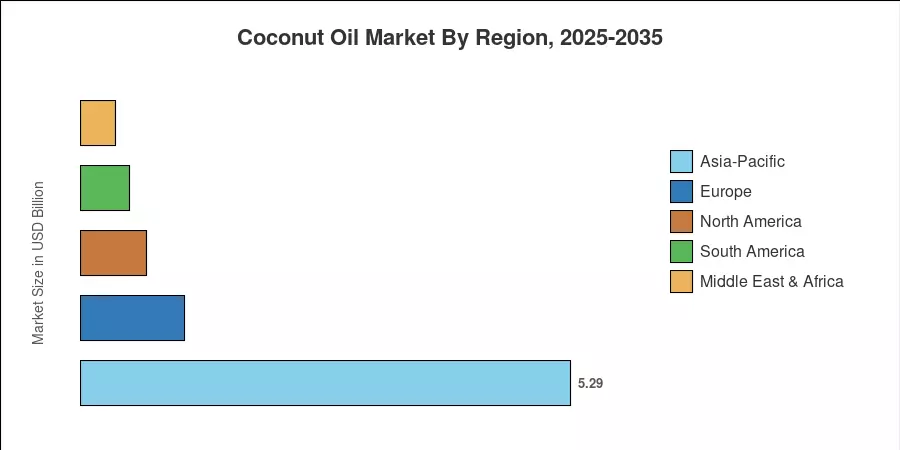

From a regional standpoint, Asia-Pacific dominates the Coconut Oil Market with an estimated 68.82% of global volume in 2025, anchored by the Philippines, Indonesia, and India. North America is the fastest-growing region at a projected CAGR of 9.28% through 2035, fueled by premium personal-care launches and the keto-diet trend that elevated coconut oil into mainstream grocery aisles. Europe holds the second-largest import share, with Germany, the UK, and France collectively accounting for over half of regional demand. The Coconut Oil Market is positioned for a decade of sustained expansion as both food-grade and industrial-grade applications broaden [3].

Key Report Takeaways

• By Product Type

- Refined grades held 57.53% of the Coconut Oil Market in 2025, driven by shelf-stability requirements in packaged food manufacturing.

- Un-refined variants are the fastest-growing product category, advancing at a 9.05% CAGR through 2035 as health-conscious consumers gravitate toward minimally processed oils.

• By Nature

- Conventional production captured 68.72% of the Coconut Oil Market in 2025, reflecting the entrenched supply base across Southeast Asian plantations.

- Organic grades are expanding at a 9.15% CAGR through 2035, propelled by certification mandates from retailers in North America and the EU.

• By Application

- Food and beverages accounted for 58.94% of demand in 2025, anchored by frying oils, confectionery coatings, and plant-based dairy alternatives.

- Cosmetics and personal care represent the fastest-growing application segment at an 8.40% CAGR, as brands leverage lauric acid's antimicrobial profile in hair and skin formulations.

• By Region

- Asia-Pacific commanded 68.82% of global volume in the Coconut Oil Market in 2025.

- North America leads growth with a 9.28% CAGR through 2035, while Europe holds approximately USD 1.12 billion in 2025 trade value.

Market Size and Forecast (2021–2035)

Market Research Future estimates derive from a triangulated methodology combining trade-flow analysis (UN Comtrade HS 1513.11/1513.19), producer-country export data from the Philippine Statistics Authority and BPS-Statistics Indonesia, and demand-side modeling informed by FMCG scanner data and personal-care formulation audits. Historical figures reflect actual trade volumes; forecast values apply the calibrated 7.90% CAGR with adjustments for El Niño yield disruptions and organic-certification adoption curves.