Coding and Marking Equipment Market Summary

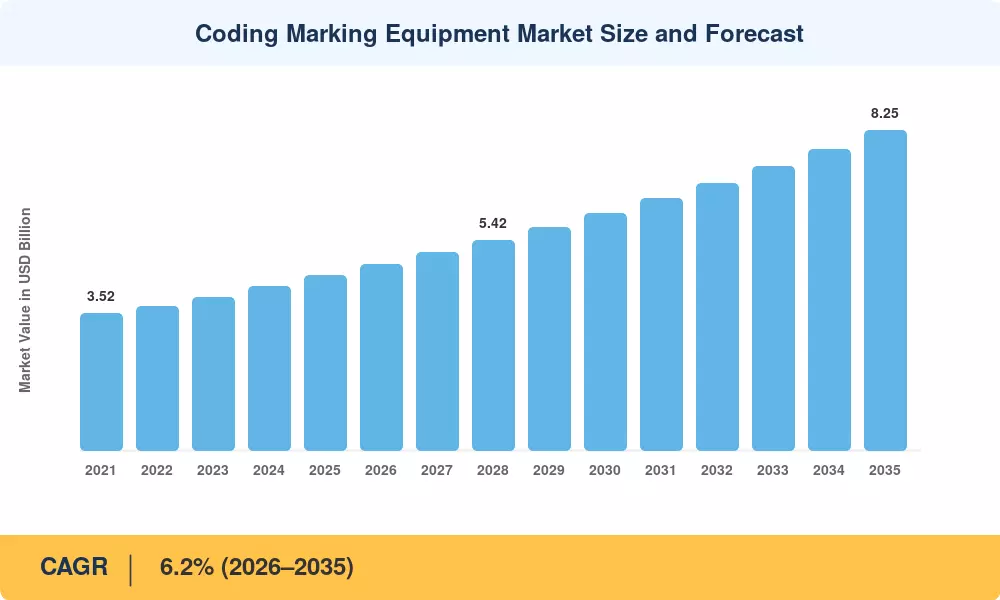

The global Coding and Marking Equipment Market reached an estimated USD 4.52 billion in 2025 and is projected to grow from USD 4.80 billion in 2026 to USD 8.25 billion by 2035, registering a CAGR of 6.2% during the forecast period (2026–2035). Two forces are accelerating this trajectory: tightening product traceability regulations under the EU Falsified Medicines Directive and the U.S. Drug Supply Chain Security Act (DSCSA), and a global packaging output surge driven by e-commerce volumes that exceeded USD 6.3 trillion in 2024 [1]. The Coding and Marking Equipment Market sits at the intersection of regulatory compliance and operational efficiency, making it resilient across economic cycles.

A substantial technological transformation is currently in progress. Legacy contact-based printers, such as roller coders and hot stampers, are gradually being replaced by non-contact inkjet and laser systems that offer a higher throughput, variable data capability, and a lower per-mark cost. Manufacturers prioritized Industry 4.0 integration, resulting in a 12% year-on-year increase in capital expenditure on digital coding platforms in 2024, surpassing USD 1.9 billion globally [2]. Remote diagnostics and real-time line monitoring are now possible with cloud-connected coding platforms, which have reduced unplanned outage by as much as 30% in early adopter facilities [3].

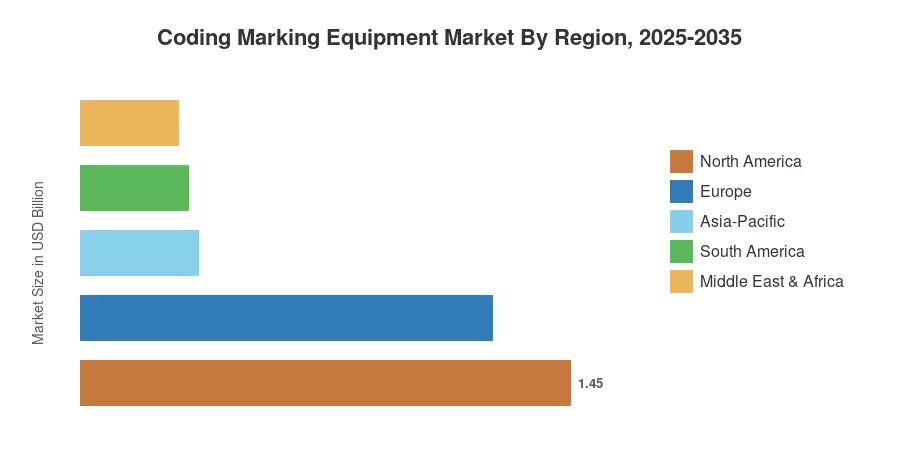

The Coding and Marking Equipment Market is dominated by North America, which holds an approximate 32% revenue share. This dominance is attributed to the mature food-safety infrastructure and stringent FDA serialization mandates. Propelled by the mandatory product traceability standards in China and the expansion of pharmaceutical manufacturing in India, the Asia-Pacific region is the fastest-growing, with a projected CAGR of 7.8%. Europe's second-largest share, approximately 27%, is based on the harmonization of GS1 standards and the EU's Green Deal packaging reforms [4]. The Coding and Marking Equipment Market is poised for consistent double-digit investment growth through 2035 as sustainability and digital transformation intersect.

Key Report Takeaways

• By Technology

- Continuous inkjet (CIJ) technology holds the largest share of the Coding and Marking Equipment Market at approximately 38% of 2025 revenue, driven by versatility across substrates and line speeds.

- Laser coding systems are the fastest-growing technology segment, registering a CAGR of 8.1% during 2026–2035 as manufacturers seek consumable-free marking solutions.

- Thermal transfer overprinter (TTO) systems account for an estimated USD 0.52 billion in 2025, anchored by flexible packaging demand.

• By End-Use Industry

- Food and beverage remains the dominant end-use vertical in the Coding and Marking Equipment Market, representing roughly 36% of total demand.

- The pharmaceutical sector is expanding at a CAGR of 7.4%, the fastest among end-use verticals, as serialization requirements cascade across emerging markets.

• By Geography

- North America leads the Coding and Marking Equipment Market with an estimated USD 1.45 billion in 2025 revenue.

- Asia-Pacific is the fastest-growing region at a 7.8% CAGR, with China and India representing more than 60% of regional demand.

- Europe maintains the second-largest position in the Coding and Marking Equipment Market, supported by strict traceability legislation.

Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining manufacturer revenue disclosures, end-user procurement surveys across 22 countries, and cross-validation against packaging-line installation data tracked by independent industry associations. Historical figures (2021–2024) reflect reported outcomes, while 2025 represents the calibrated base year. Forecast values (2026–2035) apply a compound annual growth model informed by regulatory pipeline analysis and capital-expenditure benchmarks.