Coffee Pods and Capsules Market Summary

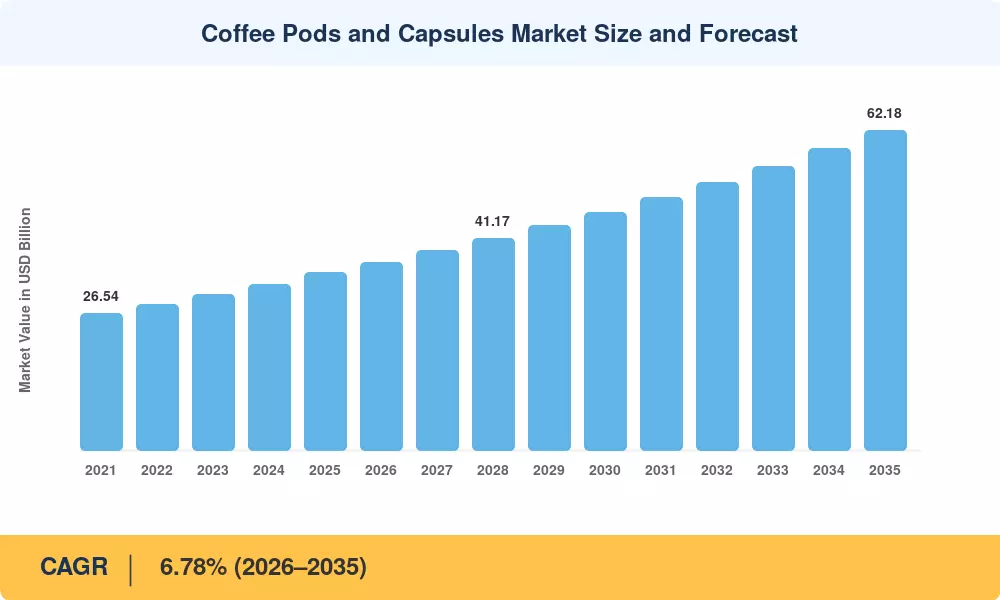

The Coffee Pods and Capsules Market stood at an estimated USD 34.50 billion in 2025 and is projected to reach USD 36.72 billion in 2026 before climbing to USD 62.18 billion by 2035, registering a CAGR of 6.78% over the 2026–2035 forecast window. This trajectory reflects a deep structural shift in how consumers interact with coffee at home and in commercial settings, propelled by the rapid proliferation of single-serve coffee capsule machines and a global premiumization wave that has redefined daily brewing rituals. Policy tailwinds — particularly the EU's Single-Use Plastics Directive and its 2025 amendments targeting non-recyclable food packaging — have accelerated investment in compostable coffee pods and aluminum-based formats, reshaping the competitive playbook across major geographies [2].

Legacy drip and pour-over systems are steadily giving way to closed-system home espresso pod system platforms that deliver barista-grade extraction with one-touch convenience. Nestlé's Nespresso division alone invested over EUR 1.3 billion in production capacity between 2022 and 2024, while rival systems from JDE Peet's, Lavazza, and Illy expanded Nespresso compatible pods lines to capture switching consumers [3]. The coffee capsule subscription model has simultaneously matured, with direct-to-consumer brands reporting 35–40% subscriber retention rates and average order values climbing 12% year-on-year through 2024.

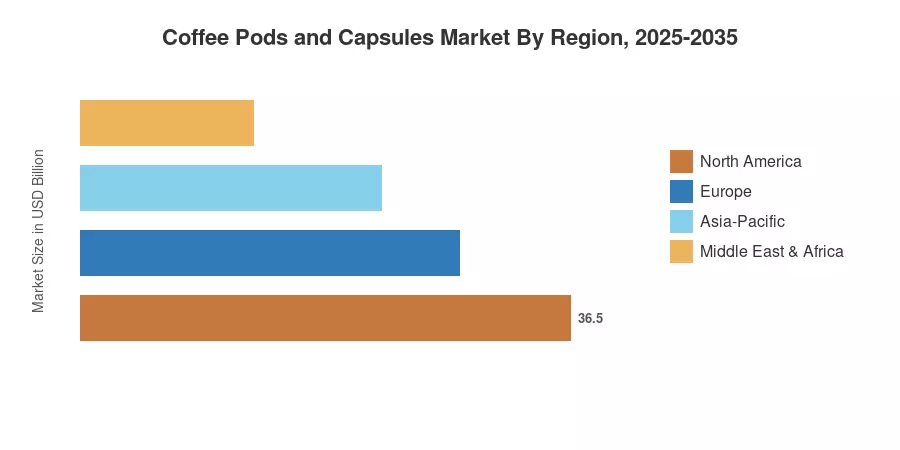

Europe commands the largest share of the Coffee Pods and Capsules Market at roughly 38.4% of 2025 revenue, anchored by Italy, France, and Germany, where pod penetration in households exceeds 45%. Asia-Pacific represents the fastest-growing region with a projected CAGR of 7.58%, driven by rising disposable incomes in China, Japan, and South Korea. North America holds the second-largest position, with the United States alone accounting for over 60% of regional demand as retailers expand private-label single-serve coffee capsule offerings

Key Report Takeaways

• By Product Type

- Capsules held a dominant 55.2% share of the Coffee Pods and Capsules Market in 2025, supported by Nespresso compatible pods and proprietary closed systems

- Pods are forecast to register a CAGR of 7.12% through 2035, fueled by open-system ESE pod adoption and compostable coffee pods innovation

• By Category

- Conventional coffee accounted for USD 30.08 billion in 2025, reflecting broad consumer preference for familiar blends

- Organic variants are expanding at a 7.84% CAGR to 2035 as health-conscious buyers seek certified single-serve coffee capsule options

• By Packaging Material

- Plastic packaging retained a 57.2% share in 2025, though environmental scrutiny is intensifying

- Aluminum formats are set to grow at a 7.32% CAGR through 2035, driven by recyclability and superior flavor preservation

• By Distribution Channel

- Off-trade channels commanded 66.1% of the Coffee Pods and Capsules Market in 2025 as grocery and e-commerce volumes surged

- On-trade is forecast to log a 7.10% CAGR between 2026–2035, with HoReCa operators adopting home espresso pod system platforms for consistency

• By Region

- Europe captured 38.4% of global revenue in 2025

- Asia-Pacific is expected to post the fastest CAGR of 7.58% through 2035, led by China and Japan

Coffee Pods and Capsules Market Size and Forecast (2021–2035)

MRFR's sizing methodology combines bottom-up revenue analysis of 45+ capsule and pod manufacturers with top-down cross-validation against trade data from Euromonitor, ICO export databases, and retail scanner panels. Historical figures (2021–2024) rely on audited company filings, while the 2026–2035 forecast applies a calibrated compound annual growth model adjusted for regional demand curves, regulatory shifts, and innovation pipelines.