Connected Living Room Market Summary

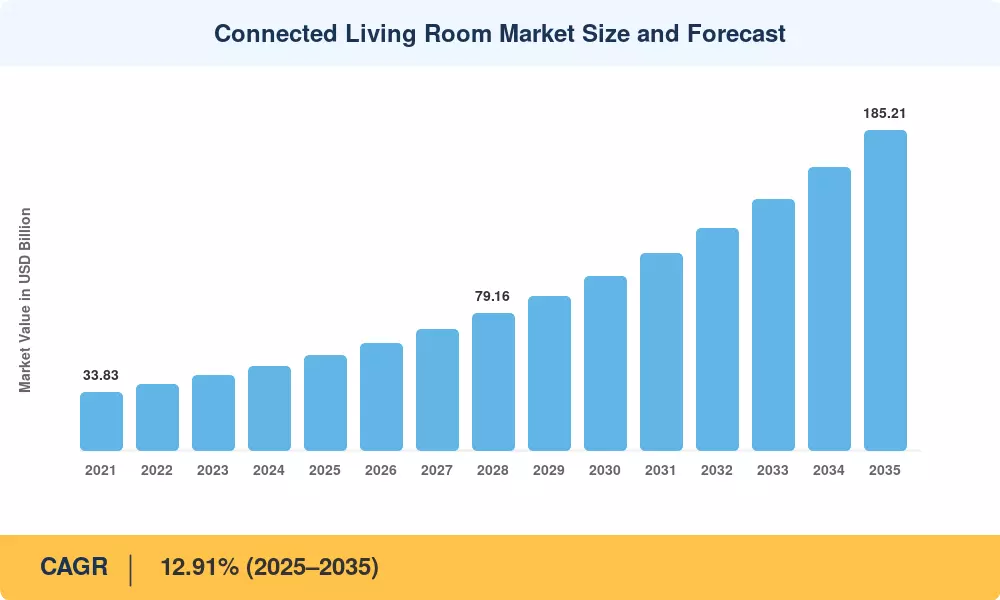

The connected living room market reached USD 64.92 billion in 2025 and is positioned to begin its forecast journey at roughly USD 70.51 billion in 2026, climbing to USD 154.18 billion by 2035 at an 8.61% CAGR. Two catalysts anchor this trajectory: the accelerating rollout of Wi-Fi 6E and Wi-Fi 7 infrastructure across residential broadband upgrades, and aggressive device-price compression driven by vertically integrated Asian manufacturers. Government broadband subsidy programs — including the US Broadband Equity, Access, and Deployment (BEAD) program with its USD 42.45 billion allocation — have widened the installed base of homes capable of supporting high-bandwidth connected home media devices.

Platform-centric ones are replacing hardware-centric business models. Integrated smart home display hubs and operating-system-driven smart TV home entertainment platforms that monetize via retail media and shoppable formats are replacing legacy standalone televisions and single-purpose set-top boxes. From 2023 to 2025, the industry invested more than USD 6 billion in cloud-delivered gaming infrastructure, growing the addressable base for the living room IoT ecosystem beyond traditional console users.

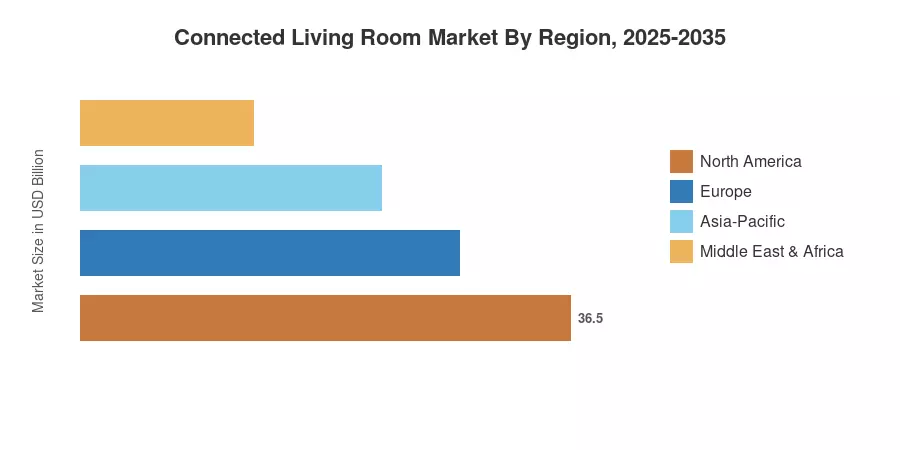

The Asia-Pacific region will account for 40.6% of revenues in the connected living room market in 2025, due to its high concentration of manufacturing and fast-growing urban broadband adoption. The Middle East & Africa is the fastest expanding segment, projected to increase at a CAGR of 12.78% through 2035, with the scaling up of smart home retrofit programs. North America is still the second largest contributor, driven by mature streaming entertainment platforms and high per-home device numbers. The next decade is the decade of adoption driven by interoperability.

Section 2 — Key Report Takeaways

By Technology

- Smart TVs led the connected living room market with a 45.8% device-type revenue share in 2024, anchored by large-screen replacement cycles

- Digital Media Streamers are projected to expand at a 13.42% CAGR through 2035 as low-cost streaming entertainment platforms broaden reach

- Wi-Fi connectivity is heading toward an 11.05% CAGR, reflecting Wi-Fi 6E/7 upgrades across the living room IoT ecosystem

By Application

- Video Streaming and OTT accounted for a 59.7% application-share of the connected living room market in 2024

- Gaming and eSports are advancing at a 10.06% CAGR, driven by native cloud-gaming apps on smart home display hubs

By Region

Section 3 — Market Size and Forecast (2021–2035)

Market sizing combines bottom-up shipment modeling for connected home media devices with top-down revenue triangulation against publicly reported vendor financials, broadband-penetration datasets, and OTT subscription benchmarks. Historical years (2021–2024) are reconciled against shipment data; forecast years apply the calibrated 8.61% CAGR with demand-elasticity adjustments for device-price compression.

.webp?v=1782975713)