Connected Ship Market Summary

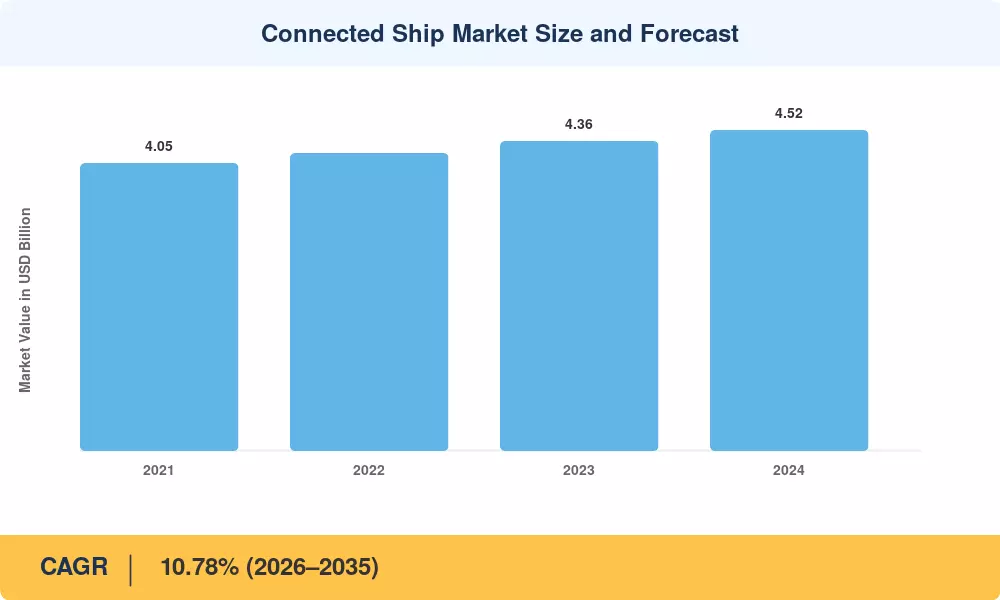

The Connected Ship Market stood at USD 4.05 billion in 2025 and is projected to reach USD 4.52 billion in 2026 before climbing to USD 11.28 billion by 2035, registering a CAGR of 10.78% during the 2026–2035 forecast period. International Maritime Organization (IMO) mandates around e-navigation readiness and the Carbon Intensity Indicator (CII) framework have converted maritime IoT connectivity from an operational luxury into a compliance necessity [1]. Fleet operators that once viewed vessel remote monitoring systems as discretionary spending now treat real-time data platforms as core infrastructure for fuel optimization and emission reporting.

A sweeping technology shift is replacing legacy point-to-point radio and VSAT setups with multi-orbit ship broadband satellite communications architectures. Low Earth Orbit (LEO) constellations from operators such as SpaceX's Starlink Maritime and OneWeb have driven per-megabit costs down by over 60% since 2021, unlocking affordable connectivity even for mid-size fishing and coastal freight fleets [2]. Smart ship digital twin platforms now ingest thousands of sensor streams — engine telemetry, hull stress, weather routing — into unified dashboards that cut unplanned downtime and trim bunker fuel consumption by 8–12% annually [3].

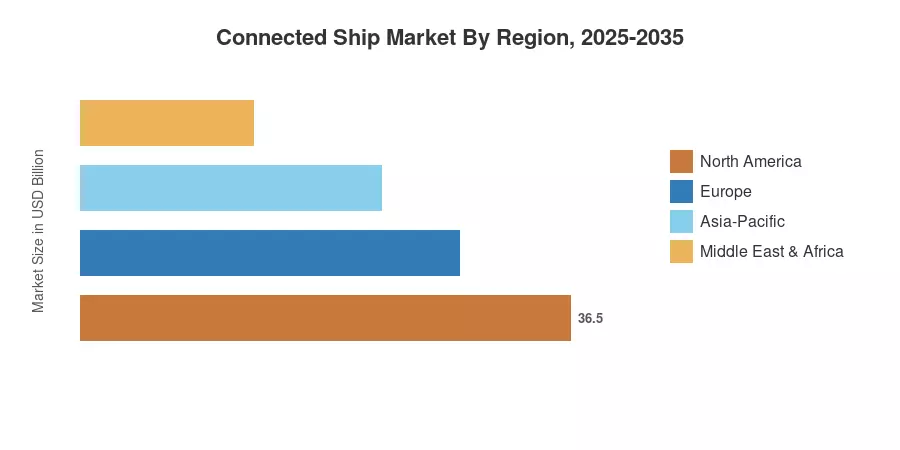

Asia-Pacific dominates the Connected Ship Market with roughly 37% revenue share, propelled by China's smart-port corridors and South Korea's autonomous vessel test-beds. The region also leads growth at a 19.4% CAGR through 2035 Europe holds the second-largest share near 28%, anchored by EU Green Deal shipping decarbonization targets and Norway's zero-emission fjord ferry mandates. North America rounds out the top three, driven by U.S. Coast Guard modernization and Canadian Arctic surveillance programs. As maritime cybersecurity solutions become mandatory under new IMO guidelines, spending across all regions is set to accelerate through the decade.

Key Report Takeaways

• By Ship Type

- Commercial vessels captured approximately 89% of Connected Ship Market revenue in 2025, reflecting broad digitization across container, tanker, and bulk carrier fleets

- Defence vessels are expanding at a 12.1% CAGR through 2035, driven by naval C4ISR upgrades and crew welfare programs

• By Application

- Fleet operations commanded a 43.8% share of the Connected Ship Market in 2025, as vessel remote monitoring systems became central to route optimization

- Fleet health monitoring is the fastest-growing application at a 12.8% CAGR, fueled by predictive maintenance demand and smart ship digital twin adoption

• By Fit

- Retrofit installations represented roughly 78% of Connected Ship Market size in 2025, given the 30,000+ active commercial vessels requiring mid-life connectivity upgrades

• By Geography

- Asia-Pacific led with 37% Connected Ship Market share in 2025 and is forecast to grow at a 19.4% CAGR through 2035

- Europe accounted for approximately USD 1.13 billion in 2025, supported by EU MRV and FuelEU Maritime regulations

Market Size and Forecast (2021–2035)

MRFR's estimates combine primary interviews with 120+ maritime technology executives, shipyard procurement officers, and satellite service providers with secondary validation from Lloyd's Register fleet databases, ITU maritime spectrum filings, and company annual reports. All historical figures are reconciled against customs data and verified through bottom-up demand modeling.

.webp?v=1782888035)