Control Valve Market Summary

The Control Valve Market reached USD 7.85 Billion in 2025 and is forecast to climb from USD 8.47 Billion in 2026 to USD 16.79 Billion by 2035, advancing at a 7.90% CAGR during 2026–2035. Rising global investment in water-treatment infrastructure—the U.S. EPA alone allocated over USD 50 Billion under the Bipartisan Infrastructure Law for clean water programs—and tightening fugitive-emission regulations across OECD economies are channeling procurement budgets toward higher-specification flow-control hardware[2].

A generational technology shift is redefining the Control Valve Market. Legacy pneumatic-only valve assemblies are giving way to digitally integrated units equipped with smart positioners, predictive-diagnostics firmware, and low-emission packing systems. The European Commission's updated Industrial Emissions Directive (IED-2024) imposes packing-leakage limits below 100 ppm, compelling plant operators to retrofit or replace tens of thousands of aging valve stations across refining and petrochemical complexes [3]. Simultaneously, the rise of hydrogen-ready and small modular reactor (SMR) piping specifications is pulling R&D spend toward cryogenic trim, high-alloy body materials, and fail-safe electric actuation.

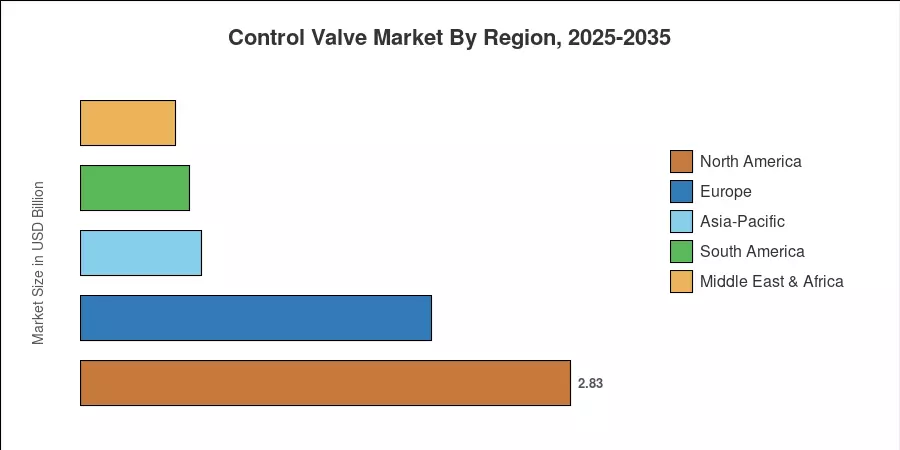

North America commanded a 36.0% share of the Control Valve Market in 2025, anchored by midstream pipeline expansions and pharmaceutical facility build-outs. Asia-Pacific is positioned as the fastest-growing region at an 8.95% CAGR through 2035, driven by China's "Dual Carbon" decarbonization strategy and India's Jal Jeevan Mission water program. Europe holds the second-largest share at 25.8%, buoyed by green-hydrogen valve demand. These regional dynamics suggest the Control Valve Market will diversify revenue sources considerably over the coming decade.

Key Report Takeaways

• By Valve Type

- Butterfly valves accounted for 32.1% of Control Valve Market revenue in 2025, reflecting their widespread adoption in HVAC and water-distribution systems.

- Plug valves are projected to post an 8.35% CAGR through 2035, supported by increasing deployment in isolation and throttling duties across chemical plants.

• By Actuation Technology

- Pneumatic actuators held a 43.9% share of the Control Valve Market in 2025, favored for their fast stroking speeds in safety-critical loops.

- Electric actuators are set to register the fastest growth at a 10.75% CAGR, fueled by plant electrification and digital-twin integration.

• By Region

- North America captured 36.0% of the Control Valve Market in 2025.

- Asia-Pacific is forecast to expand at an 8.95% CAGR, the highest among all regions.

Market Size and Forecast (2021–2035)

Market Research Future derives its sizing estimates from bottom-up demand analysis across thirteen end-use verticals, cross-validated with import/export customs databases, OEM shipment disclosures, and distributor channel checks in over 40 countries. All historical values are based on confirmed shipment and installation data; forecast figures incorporate macroeconomic projections from the IMF, regional capex pipeline trackers, and policy scenario modeling[4].