Cookies Market Summary

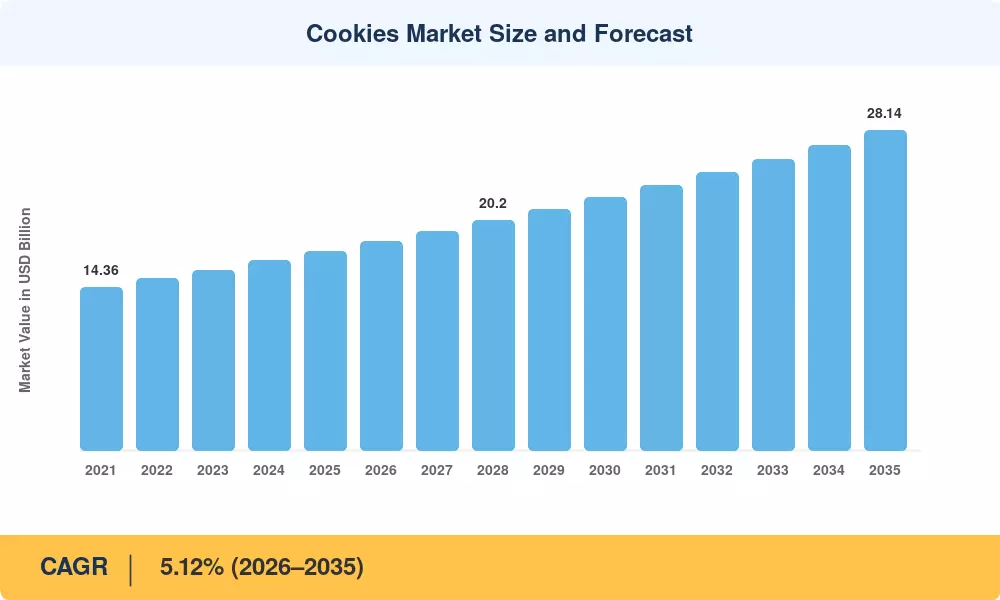

The global Cookies Market reached an estimated USD 17.53 billion in 2025 and is projected to grow from USD 18.43 billion in 2026 to USD 28.14 billion by 2035, reflecting a compound annual growth rate of 5.12% over the forecast period. This expansion is anchored in persistent snacking demand across both developed and emerging economies, reinforced by updated front-of-pack labeling regulations in the EU and the U.S. FDA's revised voluntary sodium-reduction guidelines that have pushed manufacturers toward healthier reformulations [2]. Rising consumer spending on premium indulgence categories — including soft-baked premium cookies and protein-enriched cookies — provides an additional tailwind that keeps value growth ahead of volume growth.

Product innovation is fundamentally changing the Cookies Market. Mass-produced legacy cookie and plain cookie lines are being replaced by reformulated options, including plant-based vegan cookie options with oat milk and chickpea flour, a healthy snack version of oat cookies with added fiber and prebiotics, and chocolate chip cookie line extensions with monk-fruit blend instead of refined sugar . Mondelēz International alone has invested approximately USD 1.2 billion in its global biscuit modernization effort from 2023 to 2025, renovating 14 plants with AI-guided baking lines that reduce energy use by 18% [4].

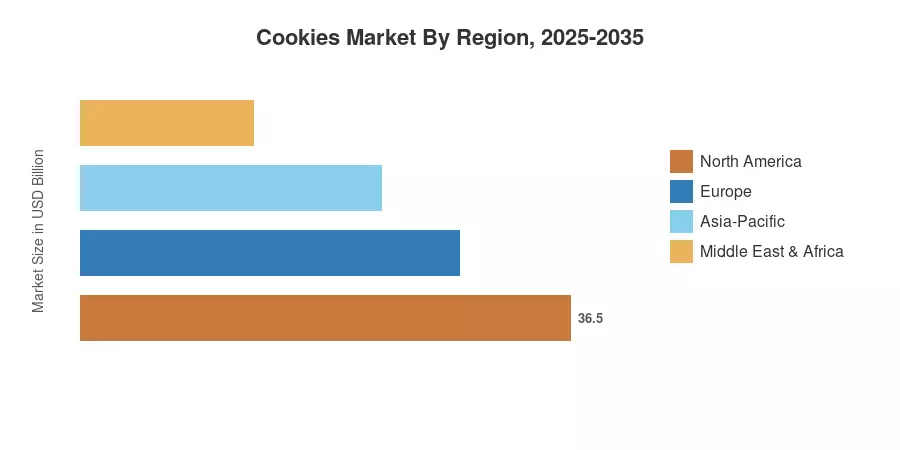

In 2025, Europe will remain the largest Cookies Market, accounting for about 32.1% of the worldwide revenue. The key players in the Cookies Market in the region are Germany and the UK, both of which have mature private label ecosystems. The fastest growing geography is South America, which is expected to post a CAGR of 7.18% through 2035, led by booming organized retail in Brazil and Argentina. The Asia-Pacific region is the second largest, with a share of around 26.4%. The region’s volume gains are driven by China and India, where middle-class discretionary spending is growing The coming decade will reward producers who blend enjoyment with transparency and nutritional fortification.

Key Report Takeaways

• By Product Type

- Butter/shortbread and plain cookies commanded a leading 35.6% share of the Cookies Market in 2025, reflecting entrenched consumer preference for classic flavors

- Bar cookies are forecast to expand at 6.35% CAGR through 2035, propelled by on-the-go snacking habits and protein-enriched cookies innovation

- Molded/drop cookies are gaining traction among artisan and direct-to-consumer chocolate chip cookie brand operators

• By Category

- The conventional segment held 96.8% of the 2025 Cookies Market value, although the free-from segment is accelerating faster at 7.12% CAGR through 2035

- Plant-based vegan cookies and healthy oat cookie snack products anchor the free-from category's incremental gains

• By Distribution Channel

- Hypermarkets and supermarkets captured 41.7% share in 2025, while online retail is expected to post a 7.02% CAGR as brand-run subscription programs deepen reach

• By Packaging Format

- Pouches and sachets accounted for 67.2% of the 2025 Cookies Market, reflecting portion-control trends

• By Geography

- Europe contributed 32.1% of global revenue in 2025; South America is projected to achieve the highest regional CAGR at 7.18%

Cookies Market Size and Forecast (2021–2035)

The following market sizing draws on Market Research Future's proprietary demand-side modeling, cross-validated against trade-level shipment data, retail scanner panels, and publicly filed corporate revenues. Historical figures (2021–2024) reflect actual reported data; 2025 represents the calibrated base year; and the 2026–2035 forecast applies the 5.12% CAGR with adjustments for anticipated raw-material cycles and regulatory shifts.