Copper Alloy Foils Market Summary

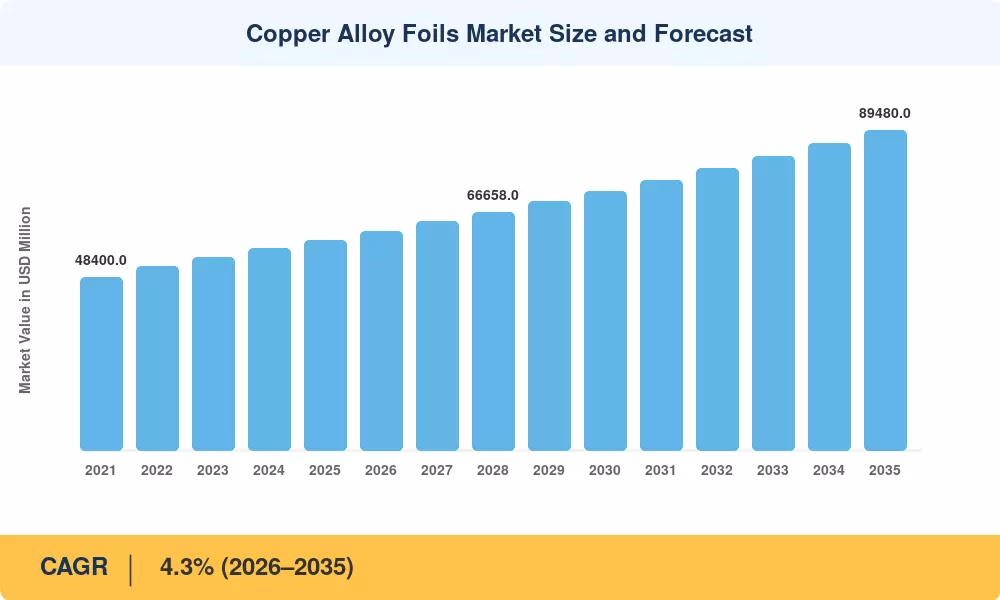

The Copper Alloy Foils Market reached an estimated USD 58,750 Million in 2025 and is projected to grow from USD 61,275 Million in 2026 to USD 89,480 Million by 2035, registering a CAGR of 4.3% across the forecast window. This trajectory reflects sustained global investment in electrification infrastructure — the International Energy Agency's World Energy Outlook 2024 flagged copper-intensive grid upgrades worth over USD 680 billion through 2030, a catalyst that directly feeds demand for high-conductivity alloy grades [1]. Government mandates tied to the energy transition, including the U.S. Inflation Reduction Act and the EU Green Deal Industrial Plan, have locked in multi-decade procurement pipelines for copper-based components used in EV charging stations, renewable energy systems, and smart-grid interconnects .

The Copper Alloy Foils Market is undergoing a quiet but meaningful transformation in processing technology. Traditional batch-melt casting lines are steadily giving way to continuous-strip casting and precision powder-metallurgy routes that deliver tighter tolerances and reduce scrap rates by 12–18% . This shift matters because downstream OEMs in electronics and automotive are specifying thinner, lighter alloy profiles that older equipment simply cannot produce at scale. Investments in digital twin-enabled smelters — Aurubis committed EUR 530 million to its Hamburg site modernization program through 2026 — signal where the industry is heading [4].

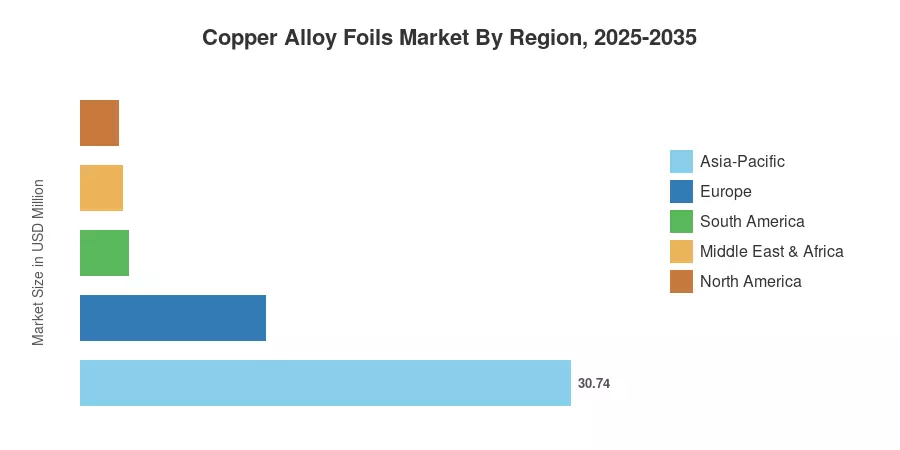

Asia-Pacific commands roughly 53% of the Copper Alloy Foils Market and also represents the fastest-growing region, propelled by China's infrastructure stimulus packages and India's push to expand domestic copper smelting capacity under its Production-Linked Incentive scheme [5]. Europe holds the second-largest share at approximately 20%, anchored by Germany's automotive and industrial-machinery sectors. North America, accounting for around 17%, is gaining momentum as onshoring policies redirect supply chains back to domestic alloy producers. The decade ahead will reward market participants who can scale sustainable production while meeting increasingly stringent alloy-purity specifications.

Key Report Takeaways

• By Type

- Brass accounts for the largest share of the Copper Alloy Foils Market at roughly 41% of global revenue, driven by plumbing, architectural hardware, and ammunition casing demand.

- Bronze is expanding at a CAGR of 4.6% through 2035, fueled by marine propulsion and heavy-bearing applications that prize corrosion resistance.

- Copper-Nickel alloys represent approximately USD 10,800 Million in 2025, reflecting strong pull from desalination plants and offshore energy infrastructure.

• By End-Use Industry

- Construction is the top end-use vertical for the Copper Alloy Foils Market, contributing around 30% of demand through plumbing tube, roofing sheet, and HVAC componentry.

- Electrical and Electronics holds a CAGR of 4.7%, the fastest among end-use segments, underpinned by 5G rollout and data-center expansion.

- Automotive demand is valued at approximately USD 11,750 million in 2025, with EV-related content per vehicle climbing steadily.

• By Region

- Asia-Pacific dominates the Copper Alloy Foils Market, contributing over 53% of global revenue in 2025.

- North America is growing at a CAGR of 4.1%, supported by re-shoring incentives and grid-modernization spending.

- Europe maintains a share of roughly 20%, with Germany alone accounting for nearly a third of regional consumption.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining top-down trade-flow analysis (ICSG, World Bureau of Metal Statistics), bottom-up production audits from the 25 largest smelters and rolling mills, and proprietary demand modeling calibrated against GDP, construction-output, and vehicle-production indices across 42 countries.

.webp?v=1784027266)