Cosmetic Surgery Market Summary

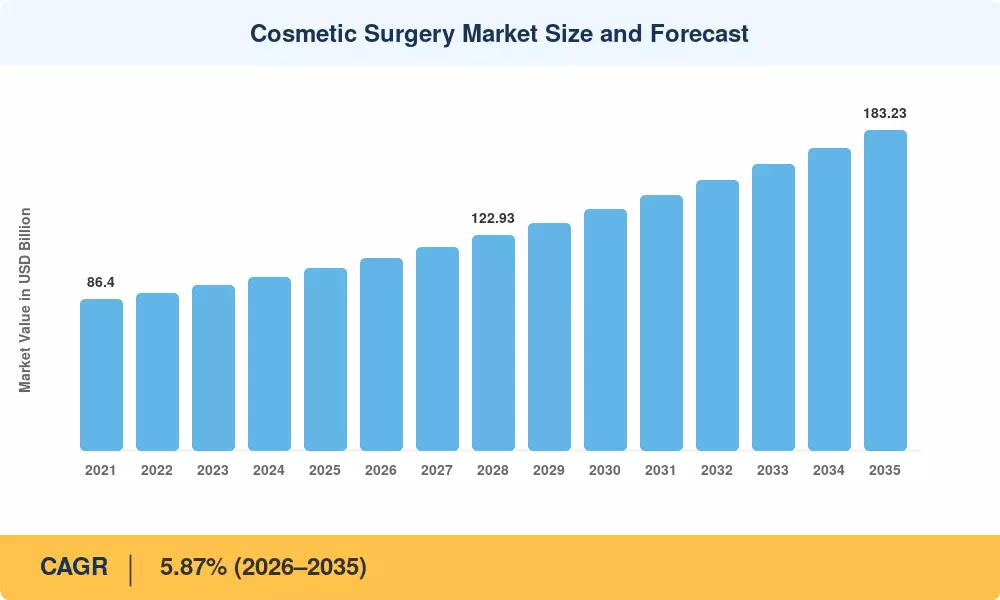

The Cosmetic Surgery Market reached a valuation of USD 104.02 billion in 2025 and is projected to grow from USD 109.67 billion in 2026 to USD 183.23 billion by 2035, registering a CAGR of 5.87% across the forecast period. Demand acceleration is rooted in two mutually reinforcing catalysts: the global proliferation of minimally invasive treatment platforms, which have cut average recovery times by half over the past five years, and the downstream procedural demand created by the rapid adoption of GLP-1 receptor agonist weight-loss therapies — a category whose prescriptions have surged roughly 300% since 2021, generating a growing pipeline of patients seeking contouring and skin-tightening procedures post-weight-loss [1].

A technology transformation is reshaping the Cosmetic Surgery Market at both the clinical and patient-acquisition levels. Legacy open-incision techniques are giving way to energy-based devices, robotic-assisted grafting, and injectable platforms that expand the addressable patient pool by lowering risk thresholds. The American Society of Plastic Surgeons reported that U.S. providers collectively invested over USD 2.3 billion in new aesthetic device infrastructure during 2024 alone, while AI-powered imaging platforms now influence pre-procedural planning in more than 40% of accredited clinics [2].

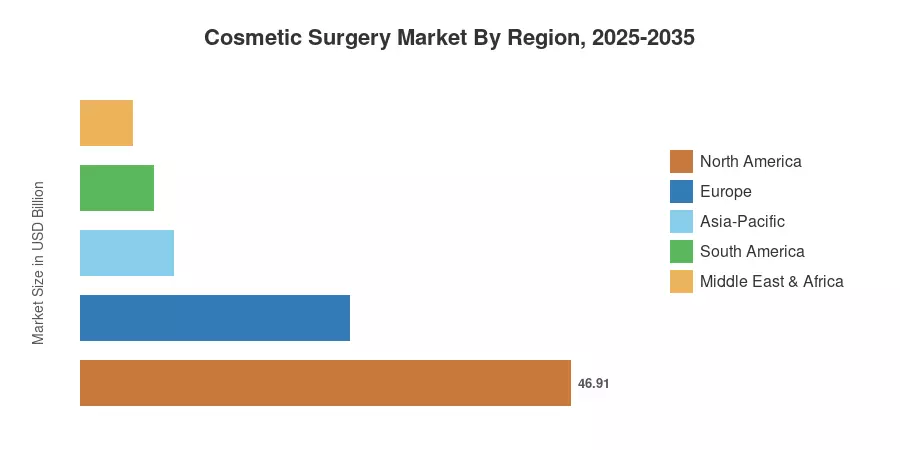

North America commands the largest share of the Cosmetic Surgery Market at approximately 45.1% of 2025 revenue, underpinned by high per-capita discretionary spending and broad insurance-adjacent financing options. Asia-Pacific stands as the fastest-growing region, propelled by expanding middle-class demand across China, South Korea, and India. Europe holds the second-largest position with roughly a 24.8% share, driven by regulatory harmonization under the EU Medical Device Regulation and strong medical-tourism inflows. The decade ahead will be defined by platform consolidation, personalized treatment sequencing, and the integration of regenerative biologic modalities into mainstream aesthetic practice.

Key Report Takeaways

• By Procedure Type

- Surgical interventions accounted for approximately 62.0% of total Cosmetic Surgery Market revenue in 2025, led by body contouring and facial reconstruction categories.

- Non-surgical modalities — including injectables, laser resurfacing, and energy-based treatments — are forecast to register the fastest CAGR of 7.84% through 2035 as patient preference shifts toward lower-downtime options.

• By Gender

- Female patients represented roughly 72.6% of Cosmetic Surgery Market demand in 2025

- Though male clientele is expanding at a 7.40% CAGR as social stigma diminishes.

• By Age Group

- The 35–50 age cohort captured the largest segment share at approximately 51.4%

- While the 18–34 demographic is growing the fastest at a 7.70% CAGR.

• By Region

- North America dominated the Cosmetic Surgery Market in 2025 with a 45.1% share, fueled by advanced clinic infrastructure and aggressive consumer financing.

- Asia-Pacific is projected to be the fastest-growing region through 2035, supported by medical-tourism ecosystems in South Korea and Thailand and rising domestic demand across India and China.

Market Size and Forecast (2021–2035)

Data for historical years (2021–2024) is derived from audited industry revenue filings, national health-expenditure databases, and proprietary primary interviews with clinic operators across 28 countries. Forecast projections (2026–2035) apply a bottom-up model calibrated against procedure-volume growth, average-selling-price trends, and regional regulatory timelines, cross-validated with top-down macroeconomic indicators.