Crop Protection Chemicals Market Summary

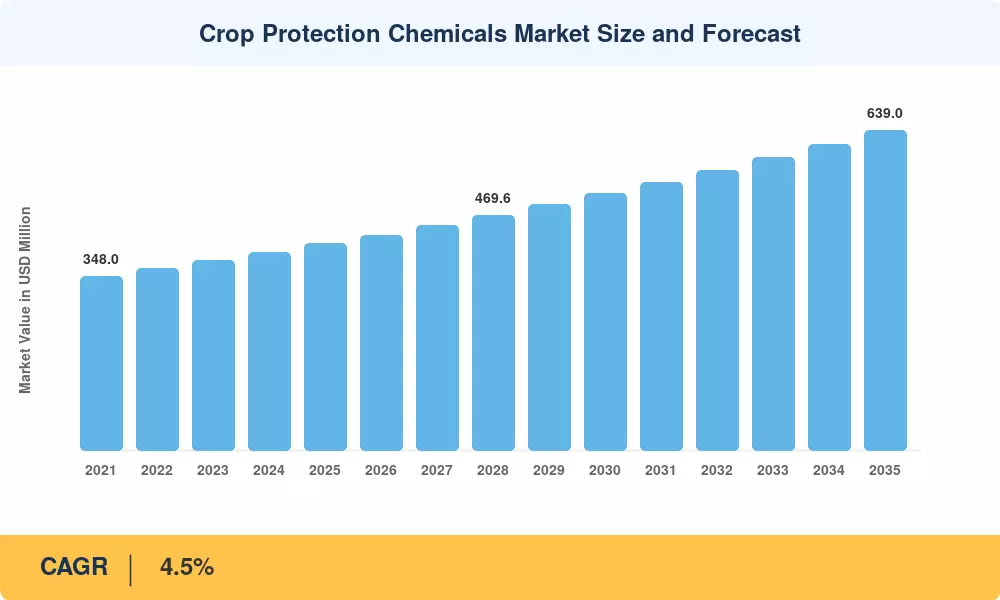

The Crop Protection Chemicals Market reached USD 413.00 Million in 2025 and is projected to grow from USD 430.00 Million in 2026 to USD 639.00 Million by 2035, registering a CAGR of 4.5% during the forecast period (2026–2035). Rising pest pressure driven by shifting climate patterns, alongside accelerating government precision-agriculture subsidies in key producing nations, continues to reshape input purchasing across the global farming sector. Regulatory bans on legacy active ingredients such as paraquat and chlorpyrifos have forced growers to adopt newer, lower-residue chemistries at premium price points, lifting overall market value even as volume growth moderates[2].

Within the Crop Protection Chemicals Market, a subtle but significant technological revolution is taking place. Data-driven variable-rate application systems combined with drone-assisted reconnaissance are replacing traditional broad-spectrum spraying programs, reducing chemical usage per hectare while increasing efficacy. By directing an estimated EUR 1.8 billion in public funding into integrated pest control and biological alternatives, the EU's Farm to Fork strategy alone aims to reduce the use of chemical pesticides by 50% by 2030 [3]. Access gaps for smallholders in Southeast Asia and Sub-Saharan Africa are being further reduced via digital farm-input marketplaces.

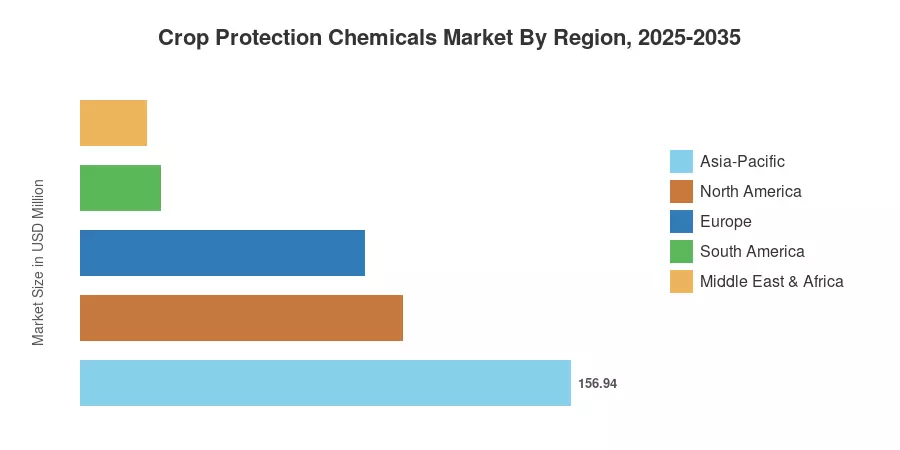

With intense rice and horticultural acreage in China, India, and ASEAN countries, the Asia-Pacific holds the highest share of the Crop Protection Chemicals Market, accounting for around 38% of 2025 revenue. With double-cropping expansion in Brazil's Cerrado belt driving growth at an anticipated 6.2% CAGR through 2035, South America is the fastest-growing continent. Herbicide-tolerant trait adoption and row-crop dominance maintain consistent demand in North America, which has the second-largest share at about 25%. Businesses that combine proven chemical efficacy with biological crop protection stacks and digital stewardship platforms will be rewarded more and more in the upcoming ten years.

Key Report Takeaways

• By Origin

- Synthetic chemistries accounted for approximately 78% of the Crop Protection Chemicals Market share in 2025, reflecting continued reliance on proven active ingredients for broad-acre crops.

- Biological formulations are advancing at a 10.2% CAGR through 2035, driven by residue-free export certification requirements and retailer sustainability mandates.

• By Product

- Herbicides led the Crop Protection Chemicals Market with a 47% share in 2025, underpinned by the global expansion of herbicide-tolerant cropping systems.

- Bio-pesticides represent the fastest-expanding product category at an 11.8% CAGR, as integrated pest management programs gain regulatory backing worldwide.

• By Application Method

- Foliar spray captured roughly 58% of the Crop Protection Chemicals Market value in 2025, remaining the dominant delivery mechanism for field and orchard crops.

- Seed treatment is growing at a 9.7% CAGR, offering growers a targeted, lower-dose approach that aligns with tightening maximum residue limits.

• By Region

- Asia-Pacific dominates the Crop Protection Chemicals Market by revenue, driven by rice paddy acreage and intensive vegetable production across China and India.

- South America is expanding at a 6.2% CAGR, fueled by soybean and sugarcane area expansion in Brazil and Argentina.

Crop Protection Chemicals Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a combination of proprietary demand models, trade-flow analysis, and company-reported revenue benchmarks calibrated against government agricultural statistics from FAO, USDA, and Eurostat[4]. Historical figures (2021–2024) reflect audited data; the base year (2025) blends preliminary actuals with survey-derived estimates; and the forecast period (2026–2035) applies a compound growth methodology anchored to crop-area projections, pest-pressure indices, and regulatory phase-out schedules.

.webp?v=1783951643)