Crypto Asset Management Market Summary

The Crypto Asset Management Market reached an estimated USD 2.52 billion in 2025 and is projected to grow from USD 3.27 billion in 2026 to USD 18.41 billion by 2035, registering a CAGR of 24.86% during the forecast period. Institutional capital flows have fundamentally reshaped the Crypto Asset Management Market over the past eighteen months, with spot Bitcoin ETFs alone attracting over USD 43 billion in net inflows during their inaugural year [2]. Regulatory frameworks such as the EU's Markets in Crypto-Assets (MiCA) regulation, fully enforced from December 2024, and the US SEC's evolving stance on digital asset classification have created the policy scaffolding that pension funds and sovereign wealth vehicles require before committing capital at scale [3].

A generational technology shift is underway as legacy portfolio management systems built for equities and fixed income give way to multi-chain crypto asset management platforms capable of reconciling positions across dozens of Layer-1 and Layer-2 networks in real time. Cloud-native architectures now dominate deployment, replacing on-premise custody stacks that once required months-long integration cycles. Institutional-grade digital asset custody solutions for enterprises have matured to the point where insured cold-storage vaults and MPC-based key management are table stakes rather than differentiators. DeFi asset tracking and analytics capabilities are being embedded directly into institutional dashboards, bridging the gap between centralized and decentralized finance.

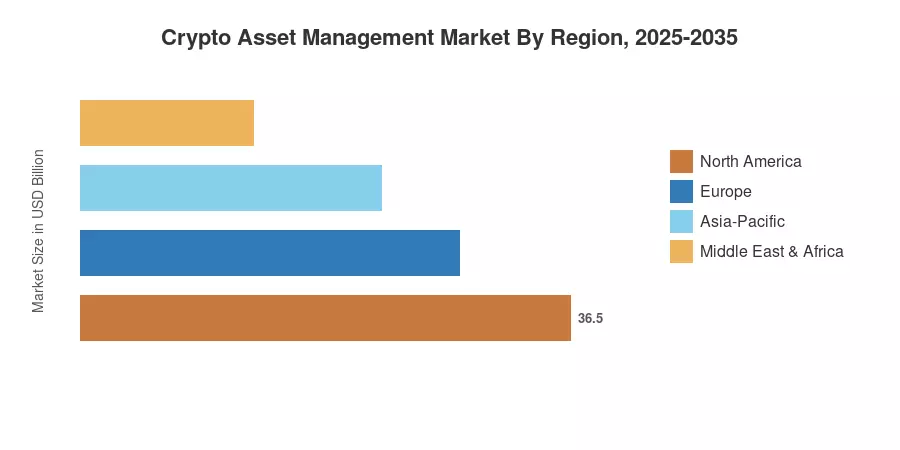

North America commands the largest share of the Crypto Asset Management Market at approximately 42% of global revenue, anchored by the concentration of ETF issuers, regulated exchanges, and venture capital in the United States [5]. Asia-Pacific represents the fastest-growing region with a projected CAGR of 27.10%, driven by crypto-forward regulatory regimes in Singapore, Hong Kong, and Japan. Europe holds the second-largest share at roughly 26%, buoyed by MiCA's harmonized licensing framework that gives asset managers passporting rights across 27 member states. The decade ahead will be defined by convergence — of CeFi and DeFi rails, of traditional and digital asset classes, and of regional regulatory standards.

Key Report Takeaways

• By Type

- Solutions captured approximately 72% of the Crypto Asset Management Market revenue in 2025, reflecting heavy enterprise demand for integrated platforms that unify institutional crypto portfolio management, reporting, and compliance in a single interface

- Services are forecast to expand at a CAGR of 26.52% through 2035, fueled by growing outsourced demand for crypto tax reporting and compliance tools, advisory and managed custody services

• By Deployment Mode

- Cloud deployment models led the Crypto Asset Management Market with roughly 86% share in 2025, as firms prioritize elastic scalability and reduced infrastructure overhead

- Hybrid architectures are projected to grow at a 26.08% CAGR through 2035, appealing to regulated entities that need on-premise key custody alongside cloud-based analytics

• By Region

- North America accounted for USD 1.06 billion of the Crypto Asset Management Market in 2025, reinforced by the first wave of spot crypto ETF approvals

- Asia-Pacific is set to register the highest regional CAGR of 27.10%, with institutional crypto portfolio management adoption accelerating across Singapore, Japan, and South Korea

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s market sizing blends bottom-up revenue analysis of platform licensing, custody fees, and managed-service contracts with top-down validation against institutional AUM growth and on-chain transaction volumes.

.webp?v=1783339232)