Cybersecurity Insurance Market Summary

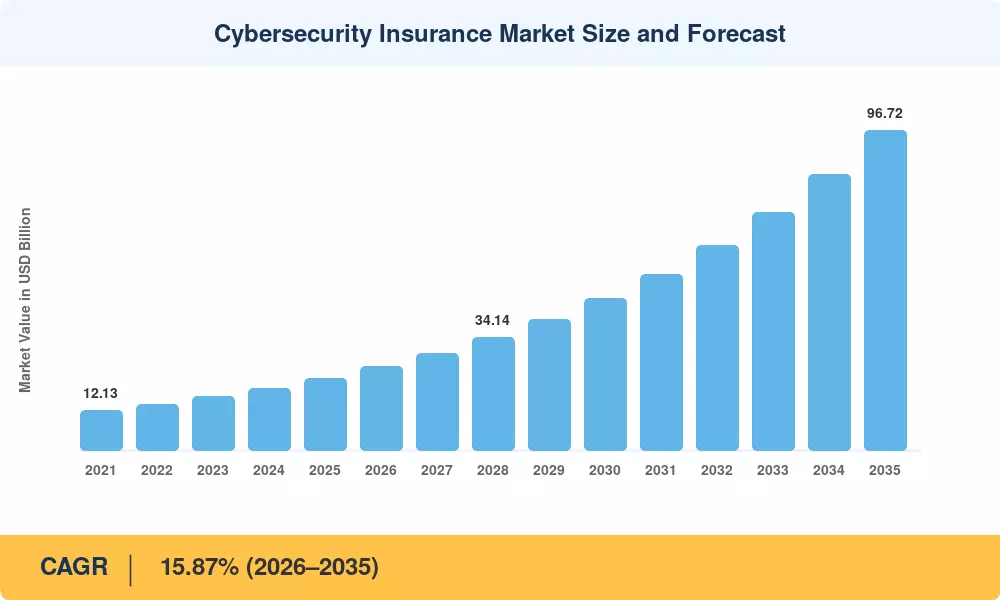

The cybersecurity insurance market reached an estimated USD 21.85 billion in 2025 and is forecast to climb from USD 25.11 billion in 2026 to USD 96.72 billion by 2035, registering a CAGR of 15.87% across the forecast window. This expansion is anchored in a wave of mandatory cyber-risk disclosure rules—the SEC's 2023 incident-reporting mandate [2] and the EU's Digital Operational Resilience Act (DORA) effective January 2025 [3]—that are compelling boards to quantify and transfer digital risk through dedicated insurance instruments. Premium rate moderation after the hard-market cycle of 2020–2022 has also reopened buying appetite among mid-cap firms that previously self-insured.

A structural shift is rewriting how the cybersecurity insurance market operates. Legacy indemnity-only policies are giving way to integrated InsurSec models where carriers embed endpoint detection, vulnerability scanning, and incident-response retainers directly into policy terms. Munich Re's 2024 Cyber Risk Survey estimated that insurers channelling at least 12% of gross written premium into embedded security controls reduced loss ratios by roughly 18 percentage points [4]. Parametric products—triggered by measurable event thresholds rather than loss adjustment—are compressing claims cycles from months to days and drawing first-time buyers in under-penetrated verticals such as manufacturing and logistics.

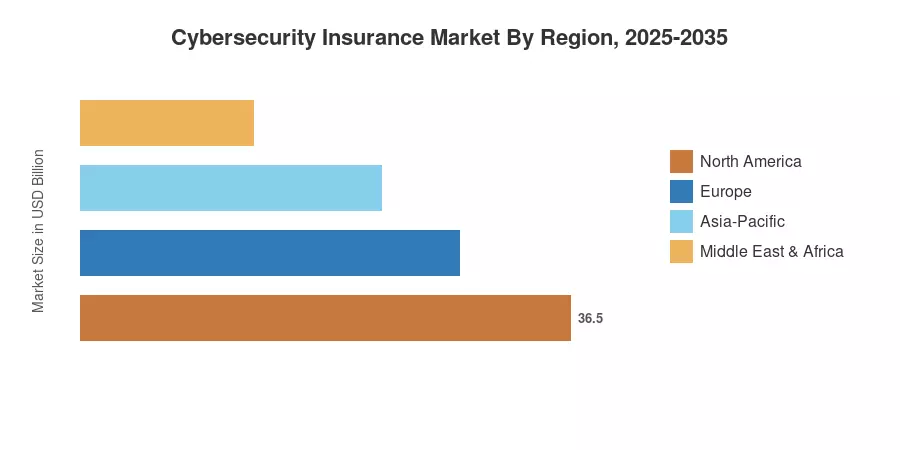

North America commanded approximately 43% of global premiums in 2025, underpinned by a mature broker ecosystem and high litigation exposure. Asia-Pacific is the fastest-growing region, with a projected CAGR of 17.48% through 2035, driven by new data-protection statutes in India, Vietnam, and Thailand. Europe holds the second-largest share at roughly 27%, propelled by NIS2 compliance deadlines that are pushing mid-market firms toward standalone cyber liability insurance for data breaches coverage. As digital supply chains deepen, the cybersecurity insurance market is poised to become a core pillar of enterprise risk architecture through the end of the decade

Key Report Takeaways

• By Coverage Type

- First-party protection accounted for 45.6% of 2025 premiums, reflecting strong demand for ransomware coverage in cybersecurity policies and business interruption coverage for cyberattacks

- Third-party liability is expanding at a 16.58% CAGR through 2035 as regulatory-fine reimbursement and class-action defence clauses widen policy scope

- Bundled/hybrid policies are gaining traction among SMEs seeking simplified procurement of cyber insurance underwriting risk assessment and incident response

• By Insurance Type

- Stand-alone cyber policies held roughly 56% of the cybersecurity insurance market in 2025, outpacing packaged endorsements as underwriters demand granular risk data

• By Organization Size

- Stand-alone cyber policies held roughly 56% of the cybersecurity insurance market in 2025, outpacing packaged endorsements as underwriters demand granular risk data

- Large enterprises captured USD 14.35 billion in premiums in 2025, yet SME-focused cybersecurity insurance products are forecast to grow fastest at a 17.02% CAGR through 2035

• By Region

- North America remains dominant with the largest premium pool, driven by litigation frequency and breach-notification laws across all 50 U.S. states

- Asia-Pacific is the fastest-growing region at a 17.48% CAGR, fuelled by India's DPDPA implementation and Japan's revised APPI guidelines

Market Research Future (MRFR)'s projections combine primary insurer interviews, gross-written-premium filings, and reinsurance treaty data with top-down macroeconomic modelling. Historical figures (2021–2024) reflect audited market results; 2025 is the base-year estimate; 2026–2035 values apply a calibrated compound growth rate verified against multiple independent benchmarks.

.webp?v=1785560414)