Dairy Blends Market Summary

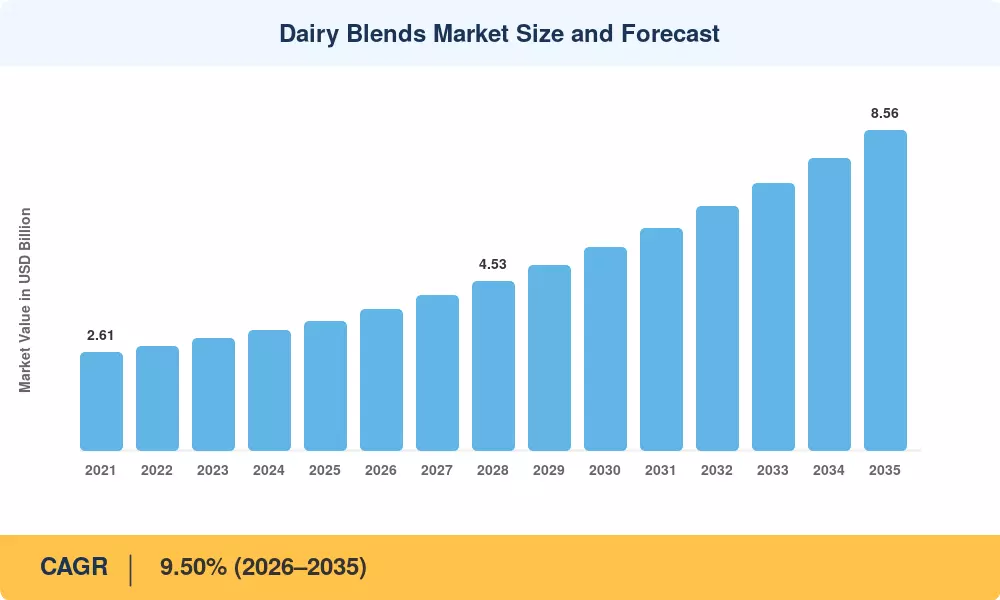

The global Dairy Blends Market was valued at USD 3.45 billion in 2025 and is projected to reach USD 3.78 billion in 2026 before climbing to USD 8.56 billion by 2035, expanding at a CAGR of 9.50% during the forecast period (2026–2035). This trajectory reflects a fundamental recalibration of how food manufacturers manage input costs, reformulate product lines, and satisfy evolving nutritional labeling requirements. Government nutrition programs across both developed and emerging economies — including the EU's Farm to Fork Strategy and India's Poshan Abhiyaan initiative — have accelerated demand for blended dairy ingredients that deliver cost-efficient protein fortification [1][2].

A pronounced transformation is underway in ingredient supply chains. Traditional single-origin dairy fats are steadily giving way to engineered blends combining dairy proteins with vegetable oils and functional additives. The International Dairy Federation estimates that blended formulations now account for over 28% of industrial dairy ingredient procurement globally, up from 19% in 2019, driven by spreadable product innovation and clean-label reformulation mandates [3]. Capital expenditure in spray-drying and fractionation infrastructure exceeded USD 1.8 billion globally in 2024 alone [4].

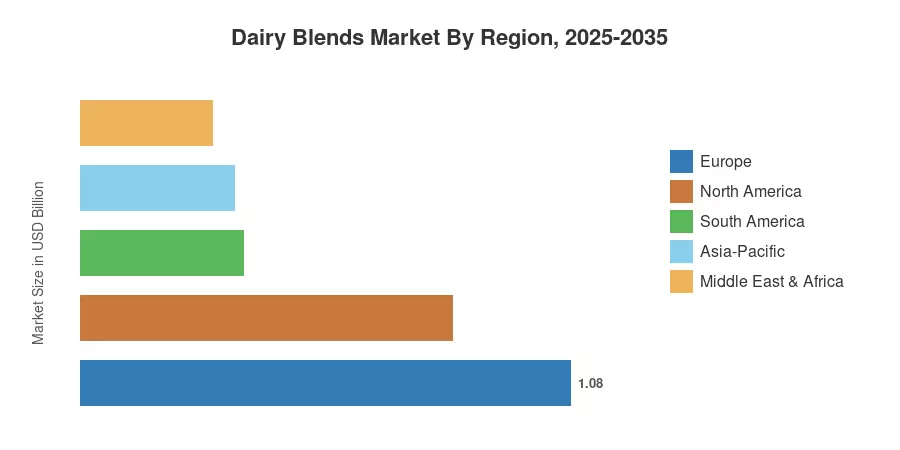

Europe commands the largest share of the Dairy Blends Market at approximately 31.23% of 2025 revenue, anchored by established dairy processing infrastructure in Germany, France, and the Netherlands. Asia-Pacific is the fastest-growing region at a projected CAGR of 9.92%, propelled by surging infant nutrition demand in China and India. North America holds the second-largest position with nearly 23.77% of the global market, driven by functional food reformulation trends across the bakery and confectionery sectors. The decade ahead promises continued double-digit regional growth rates in Southeast Asia and Sub-Saharan Africa as urbanization expands processed food consumption.

Key Report Takeaways

• By Product Type

- Milk blends captured 45.26% of the Dairy Blends Market share in 2025, reinforcing their dominance as the primary base ingredient for reconstituted and recombined dairy products.

- Butter blends are projected to expand at a 10.59% CAGR through 2035, driven by demand for affordable spreadable formats and pastry-grade fats.

• By Form

- Powder form held 43.50% of the Dairy Blends Market in 2025, reflecting the logistics advantages of shelf-stable, long-transport formulations in export-driven markets.

- Liquid blends are advancing at a 10.27% CAGR through 2035, fueled by ready-to-use formulations for bakery and beverage applications.

• By Application

- Food applications accounted for 55.20% of 2025 revenue in the Dairy Blends Market, led by bakery and confectionery end uses.

- Infant formula is forecast to grow at a 9.96% CAGR between 2026 and 2035, reflecting tightening nutritional standards and rising birth rates in developing regions.

• By Region

- Europe occupied 31.23% of the 2025 volume in the Dairy Blends Market, supported by cooperative dairy processing networks.

- Asia-Pacific is on track for a 9.92% CAGR to 2035, with China and India collectively accounting for over half of regional demand.

Dairy Blends Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated estimation methodology combining bottom-up revenue modeling from manufacturer shipment data, top-down validation against international trade databases (UN Comtrade, Eurostat), and proprietary demand surveys across 22 countries. Historical data (2021–2024) reflects actual reported figures; forecast data (2026–2035) applies a calibrated CAGR anchored to supply-side capacity expansion and consumption trend extrapolation.