Data Center Accelerator Market Summary

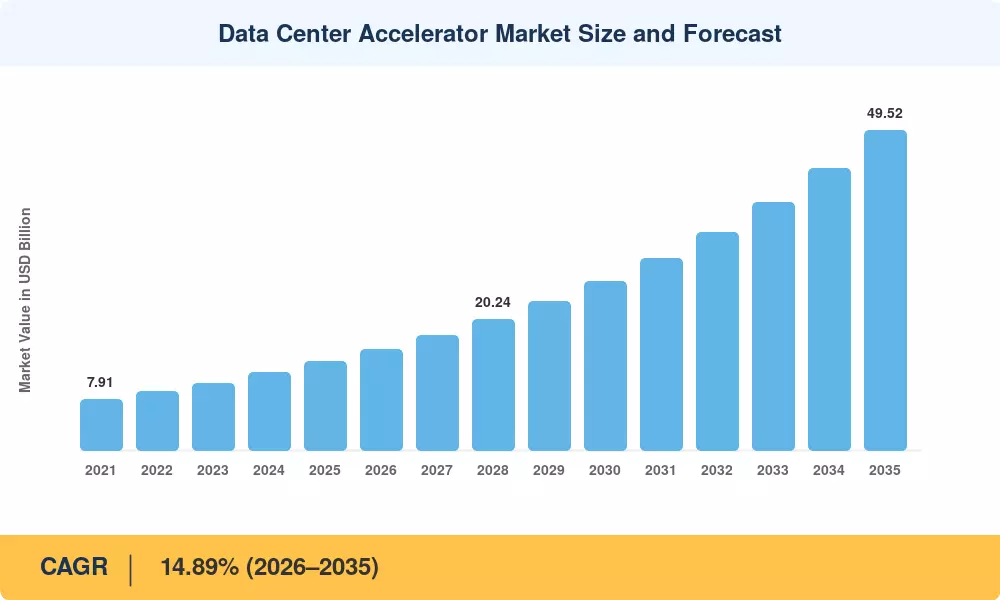

The data center accelerator market reached an estimated USD 13.79 billion in 2025 and is projected to climb from USD 15.68 billion in 2026 to USD 49.52 billion by 2035, expanding at a CAGR of 14.89% during the forecast period. Two forces are compressing adoption timelines: sovereign-cloud mandates that require domestically manufactured AI inference accelerator ASICs for servers, and hyperscaler capital-expenditure pledges that collectively exceeded USD 160 billion in 2024 alone [1]. These policy and investment tailwinds are pulling forward procurement cycles that would otherwise stretch into the next decade, making the data center accelerator market one of the fastest-moving segments in enterprise IT infrastructure.

A generational hardware transition is under way. Legacy general-purpose CPUs that once shouldered mixed workloads are giving way to domain-specific silicon—GPU accelerators for AI data centers, custom ASICs, and FPGA-based network acceleration for data centers—that deliver ten to fifty times the throughput-per-watt on training and inference tasks [2]. The U.S. CHIPS and Science Act alone has earmarked over USD 52 billion for domestic semiconductor manufacturing, while the EU Chips Act targets EUR 43 billion in public and private investment through 2030 [3]. These programs are re-routing global supply chains and encouraging fabless designers to co-invest in advanced packaging capacity.

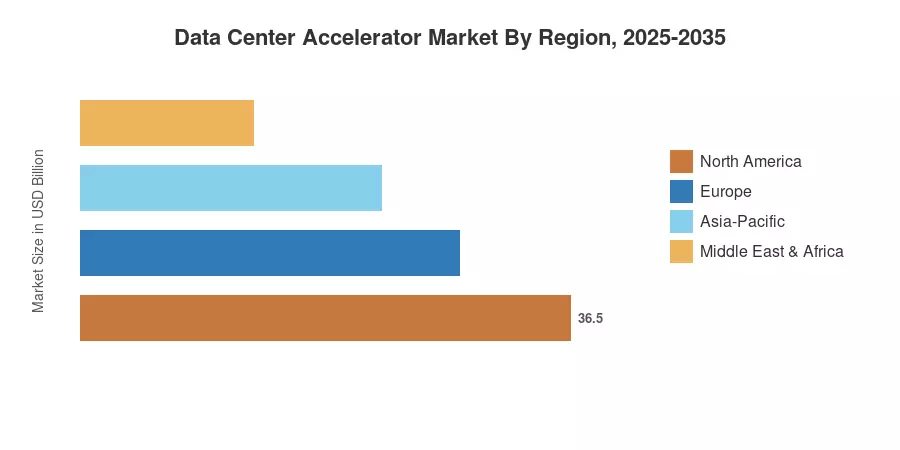

North America retained the largest regional share at roughly 38% of global revenue in 2025, driven by hyperscale cloud operators concentrated in Virginia, Oregon, and Texas. Asia-Pacific is the fastest-growing region, projected to register a CAGR exceeding 16% through 2035, fueled by China's push for GPU self-sufficiency and India's expanding colocation footprint Europe holds the second-largest share near 27%, anchored by sustainability-driven data center builds across the Nordics and the Netherlands. As AMD Instinct and Intel Gaudi AI accelerators enter volume production alongside SmartNIC DPU for data center offloading solutions, competitive intensity will reshape vendor rankings well before the decade closes.

Key Report Takeaways

• By Processor Type

- GPU accelerators for AI data centers commanded roughly 77% of data center accelerator market revenue in 2025, underpinned by NVIDIA's dominance in training clusters

- AI inference accelerator ASICs for servers are forecast to expand at a 16.4% CAGR through 2035, reflecting hyperscaler interest in custom silicon

- FPGA-based network acceleration for data centers is gaining traction in latency-sensitive financial and telco workloads

• By Application

- AI training represented approximately 52% of the data center accelerator market share in 2025

- AI inference is advancing at a 16.6% CAGR through 2035, as real-time generative-AI services scale

• By Region

- North America retained the dominant regional position in the data center accelerator market during 2025

- Asia-Pacific is projected to record the fastest CAGR through 2035, driven by semiconductor localization policies

Market Size and Forecast (2021–2035)

MRFR estimates are derived from a bottom-up build combining semiconductor vendor shipment data, hyperscaler CapEx disclosures, and regional policy-funding databases. Historical figures (2021–2024) are reconciled against audited company filings; forecast values apply the calibrated 14.89% CAGR with year-specific adjustments for supply-chain events and policy triggers.