Market Summary

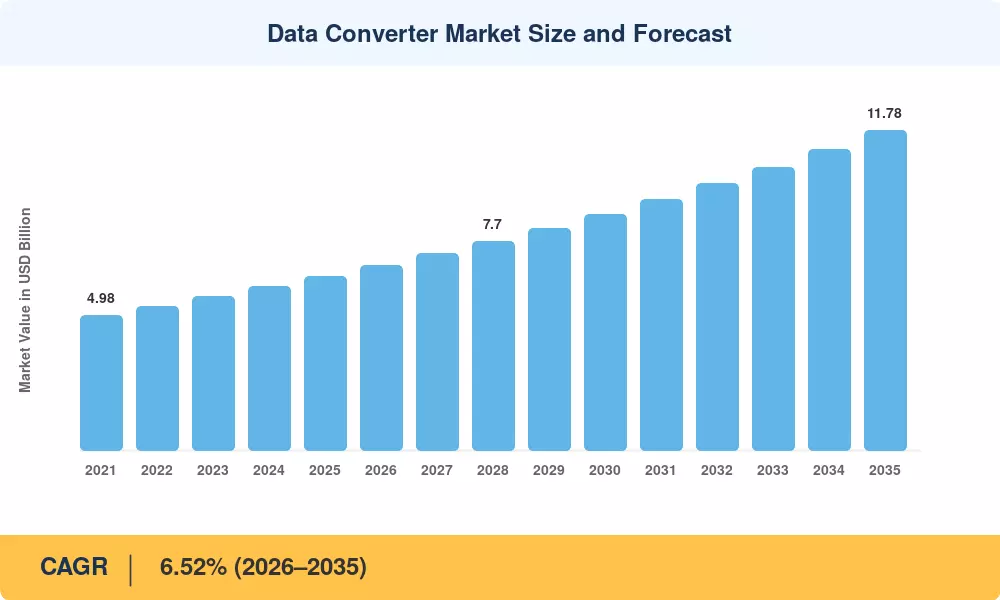

The data converter market reached an estimated USD 6.42 billion in 2025 and is projected to grow from USD 6.81 billion in 2026 to USD 11.78 billion by 2035, advancing at a 6.52% CAGR across the forecast period. Governments worldwide continue channeling infrastructure budgets into 5G rollouts and smart grid modernization — China alone earmarked over USD 26 billion for next-generation telecom buildouts through 2025 — generating sustained demand for high-speed ADC DAC converters for RF applications and precision analog-to-digital conversion across the signal chain [1]. These policy-driven capital cycles, combined with automaker commitments exceeding USD 500 billion toward electrification platforms through 2030, anchor the data converter market on a durable multi-year growth trajectory.

A sweeping technology transformation is reshaping converter architectures. Legacy standalone ADC and DAC devices are yielding to integrated mixed-signal system-in-package modules that consolidate converter cores with power management, digital filtering, and interface logic on a single substrate. Semiconductor vendors are investing heavily in advanced packaging — Texas Instruments committed over USD 11 billion to new 300 mm analog fab capacity in Texas, while Analog Devices expanded its Beaverton facility to scale production of sigma-delta ADC for high-resolution sensing products [ 2 ][ 3 ] . These investments reflect a broader pivot away from discrete signal-chain designs toward monolithic solutions that compress board area and shorten qualification timelines for OEMs deploying precision DAC for industrial control systems.

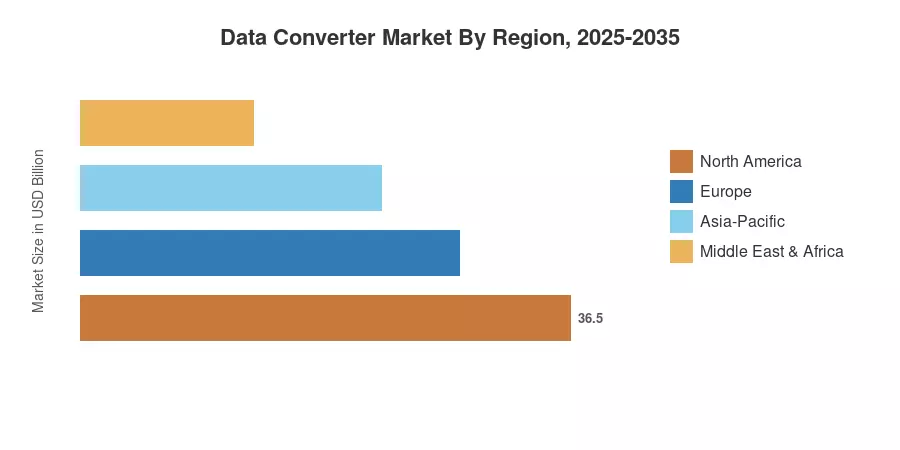

Asia-Pacific commands roughly 43% of the data converter market, propelled by dense semiconductor manufacturing ecosystems in Taiwan, South Korea, and mainland China alongside accelerating 5G subscriber uptake. The region simultaneously ranks as the fastest-growing geography, posting an anticipated 7.15% CAGR through 2035 as RF data converters for 5G base stations scale across urban and semi-rural networks North America holds the second-largest share at approximately 27%, buoyed by defense electronics procurement and a robust fabless design cluster. Europe rounds out the top three, with automotive electrification driving converter attach rates per vehicle upward even as overall unit sales stabilize. Looking ahead, the convergence of edge AI inference workloads and ultra-low-power sensing will push low-power ADC for IoT sensor nodes into volume adoption, opening fresh revenue pools beyond the data converter market's traditional strongholds.

Key Report Takeaways

• By Converter Type

- Analog-to-digital converters accounted for approximately 63% of the data converter market in 2025, reflecting their universal role in telecom, medical, and industrial signal chains

- Mixed-signal converters are the fastest-growing category, projected to expand at a 7.98% CAGR through 2035 as OEMs consolidate discrete ADC/DAC pairs into single-package solutions

• By Resolution

- 10–12-bit devices represented the largest resolution band in 2025, valued at approximately USD 2.56 billion, serving mainstream wireless and consumer applications

- Greater-than-16-bit precision converters are forecast to register the steepest growth, driven by demand from MRI scanners and geophysical instruments requiring sigma-delta ADC for high-resolution sensing

• By Sampling Rate

- Mid-speed converters (50–500 MSPS) captured around 45% of the data converter market share in 2025, underpinned by industrial automation and ultrasound imaging

- High-speed devices above 500 MSPS are poised for an 8.45% CAGR through 2035 as massive MIMO and phased-array radar platforms migrate to multi-gigahertz bandwidths

• By End-User Industry

- Telecommunications applications held roughly 27% of the data converter market in 2025, anchored by RF data converters for 5G base stations and backhaul infrastructure

- Automotive demand is advancing at a 7.35% CAGR through 2035, fueled by electrification mandates and ADAS sensor fusion requirements

• By Region

- Asia-Pacific dominated with approximately 43% of the data converter market share in 2025

- North America contributed the second-highest regional revenue, supported by defense modernization budgets and precision DAC for industrial control systems deployments

Market Researcch Future (MRFR)'s estimates blend bottom-up shipment data from leading converter vendors with top-down cross-referencing against end-market capital expenditure cycles. Historical values (2021–2024) draw on published financial disclosures, while forecast figures (2026–2035) apply the calibrated 6.52% CAGR adjusted for segment-level growth differentials. All values are in current USD billions.

.webp?v=1782888023)