Decorative Laminates Market Summary

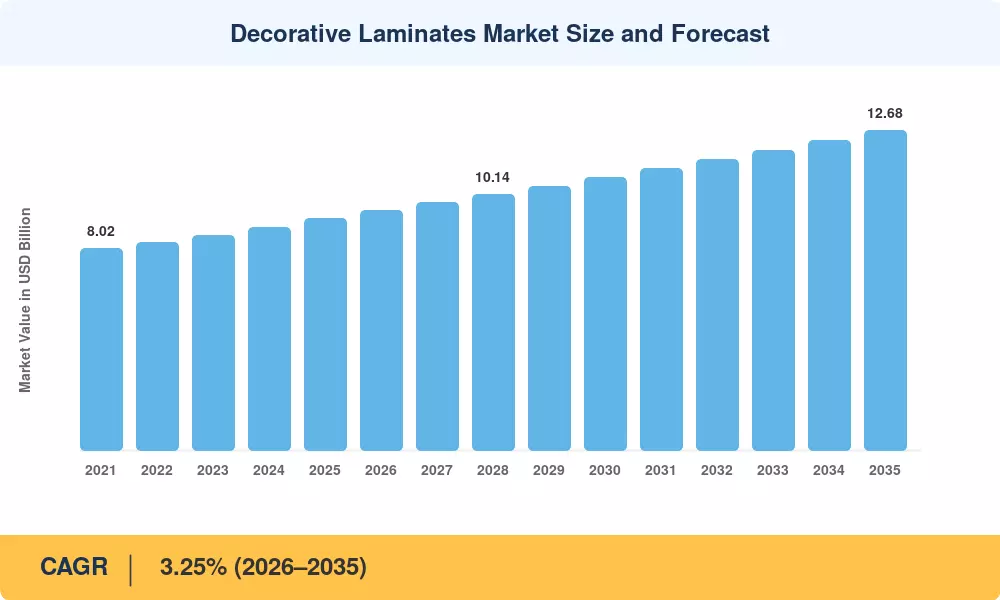

The global Decorative Laminates Market was valued at USD 9.21 billion in 2025 and is projected to reach USD 9.51 billion in 2026 before climbing to USD 12.68 billion by 2035, expanding at a CAGR of 3.25% during the 2026–2035 forecast window. Two forces anchor this trajectory: aggressive urbanization targets set by India's Pradhan Mantri Awas Yojana housing program, which aims to deliver 20 million urban housing units by 2028 [1], and tightening formaldehyde-emission ceilings across the European Union under the revised Construction Products Regulation [2]. Together, these policy catalysts are pulling investment into both residential surfacing and industrial compliance upgrades across converter facilities. The Decorative Laminates Market is transitioning from analog to digital at the production floor level.

Digital printing and emboss-in-register press lines are superseding conventional rotogravure equipment as they reduce tooling changeover costs by 40-60% and accommodate short-run bespoke décor programs increasingly demanded by contract decorators [3]. Overlay paper that offers an ultra-realistic reproduction of wood and stone is taking market share from standard kraft-core construction and exacting a price premium of 12 to 18% per sheet, thanks to its better visual authenticity. The global capital spending on high-pressure laminates manufacturing lines surpassed USD 1.3 billion in 2024, a clear indicator of the converters’ confidence in continued demand [4].

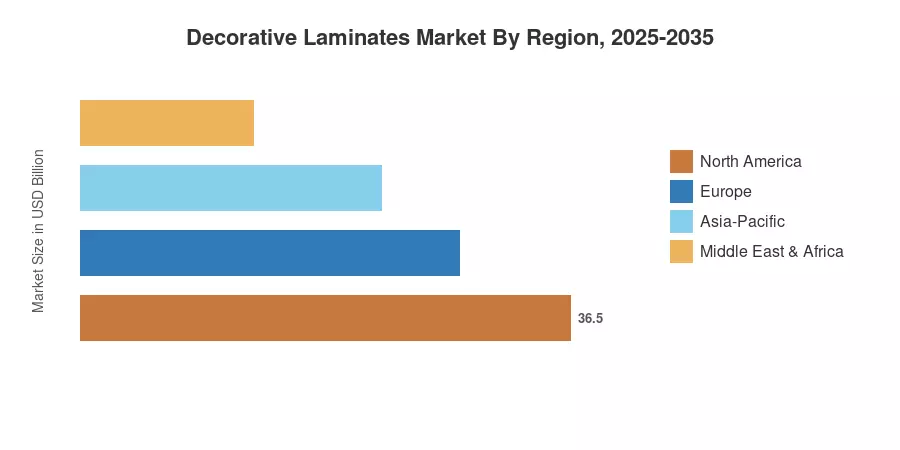

Asia-Pacific is the largest market for decorative laminates and accounts for almost 41.0% of the worldwide revenue, driven by home building in China, India and ASEAN countries. The Middle East & Africa region is the fastest expanding geography at a CAGR of 3.77% through 2035, fuelled by hospitality mega-projects in Saudi Arabia and the UAE. Europe has the second biggest share at roughly 25.5%, with investment in renovations and strict emissions rules aiding replacement cycles. The Decorative Laminates Market will see an upsurge in specification activity across both new-build and retrofit channels, owing to the wider adoption of modular building methods and prefabricated interior systems around the globe.

Key Report Takeaways

• By Raw Material

- Plastic resin commanded a 43.8% share of the Decorative Laminates Market in 2025, anchored by its cost efficiency and broad compatibility with printing technologies.

- Overlays are expanding at the fastest pace among raw material segments, registering a projected CAGR of 3.70% through 2035 as demand for photorealistic surface textures intensifies.

• By Application

- Furniture accounted for 49.4% of the Decorative Laminates Market revenue in 2025, driven by residential fit-out programs across Asia-Pacific.

- Wall panels are forecast to grow at a 3.47% CAGR to 2035, reflecting commercial interior renovation cycles in North America and Europe.

• By End-User Industry

- The residential segment represented 57.4% of the Decorative Laminates Market in 2025, underpinned by government-backed affordable housing schemes.

- Non-residential end users are projected to record a 3.89% CAGR through 2035 as hospitality, healthcare, and education infrastructure investment accelerates.

• By Geography

- Asia-Pacific held the largest regional share at 41.0% in 2025, led by construction activity in China and India.

- The Middle East & Africa region is expected to post the highest CAGR of 3.77% through the forecast period, fueled by mega-project pipelines.

Decorative Laminates Market Size and Forecast (2021–2035)

The market sizing methodology is a combination of bottom-up revenue modelling from converter shipments and top-down cross-validation with trade flow data from UN Comtrade and national building material organizations. Historical data is obtained from audited annual reports and customs databases. Forecast statistics are based on a calibrated 3.25% CAGR applied to the confirmed 2025 base.