Dental Prosthetics Market Summary

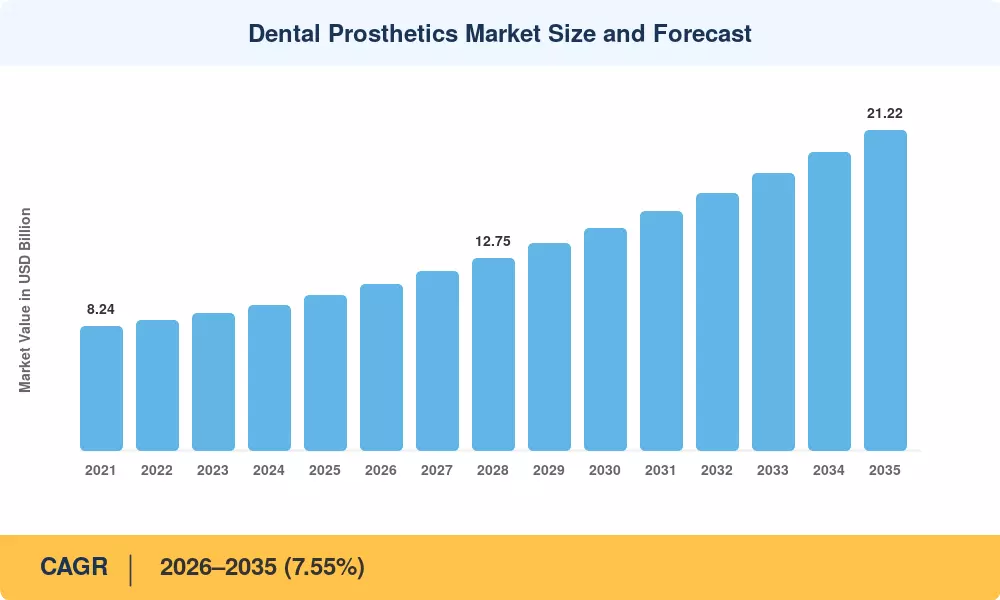

The Global Dental Prosthetics Market size was valued at USD 10.25 Billion in 2025, and the market is projected to grow from USD 11.02 Billion in 2026 to USD 21.22 Billion by 2035, registering a CAGR of 7.55% during the forecast period 2026–2035. Structural healthcare reforms across Asia-Pacific and expanded dental-insurance mandates in the Middle East are pulling millions of previously uninsured adults into the restorative care funnel, creating sustained volume demand for crowns, bridges, and full-arch prosthetic solutions. The United States' 2025 tariff on Chinese dental imports has simultaneously catalyzed nearshoring of prosthetic manufacturing to Mexico and Canada, reshaping procurement patterns for hospital networks and group dental practices alike [1].

Digital workflows are rewriting how prosthetics move from design to chairside delivery. Laboratories that once relied on manual wax-up techniques are migrating to integrated scan-to-mill platforms, with an estimated USD 1.8 Billion invested globally in dental digitization infrastructure between 2023 and 2025 [2]. This transition cuts turnaround from five days to under 48 hours for single-unit restorations, a compression that directly lifts case acceptance rates among cost-conscious patients.

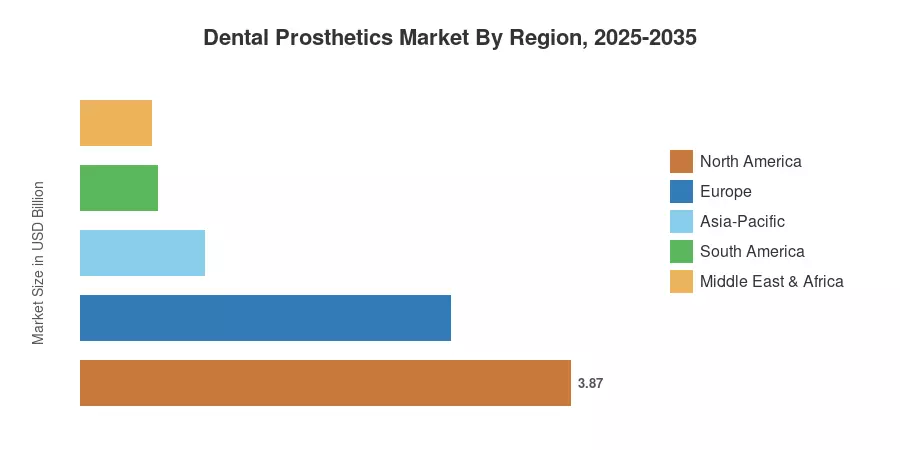

North America held roughly 37.8% of the Dental Prosthetics Market in 2025, anchored by high per-capita dental spending and mature payer networks. Asia-Pacific stands as the fastest-growing region at a projected 9.58% CAGR through 2035, driven by India's Ayushman Bharat dental-coverage expansion and Japan's aging demographics. Europe captured the second-largest share at approximately 28.5%, supported by Germany's statutory insurance model and France's "100% Santé" zero-copay crown program [3]. As aesthetic preferences reshape consumer expectations across generations, the Dental Prosthetics Market is poised for a decade of accelerating growth.

Key Report Takeaways — Dental Prosthetics Market

By Product Type

- Crowns captured 46.1% of the Dental Prosthetics Market in 2025, driven by single-visit chairside milling adoption across North America and Europe.

- The dentures segment is advancing at a 7.38% CAGR through 2035, fueled by geriatric population growth and removable full-arch demand in emerging economies.

By Material

- Ceramic and zirconia materials accounted for 51.8% of the Dental Prosthetics Market in 2025.

- Hybrid and composite materials are growing at a 10.12% CAGR through 2035 as cost-sensitive laboratories adopt them for posterior restorations.

By Region

- North America generated 37.8% of global revenue in 2025.

- Asia-Pacific is forecast to expand at a 9.58% CAGR between 2026 and 2035, with India and China driving volume.

Dental Prosthetics Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework integrates bottom-up laboratory output data, dental insurance claims databases across 32 countries, trade-flow analysis for zirconia and cobalt-chromium feedstock, and validated interviews with 150+ dental laboratory operators and prosthodontists. Historical figures (2021–2024) are derived from audited revenue disclosures and import/export customs data; forecast values (2026–2035) reflect scenario-weighted modeling anchored to demographic, regulatory, and technology-adoption variables.