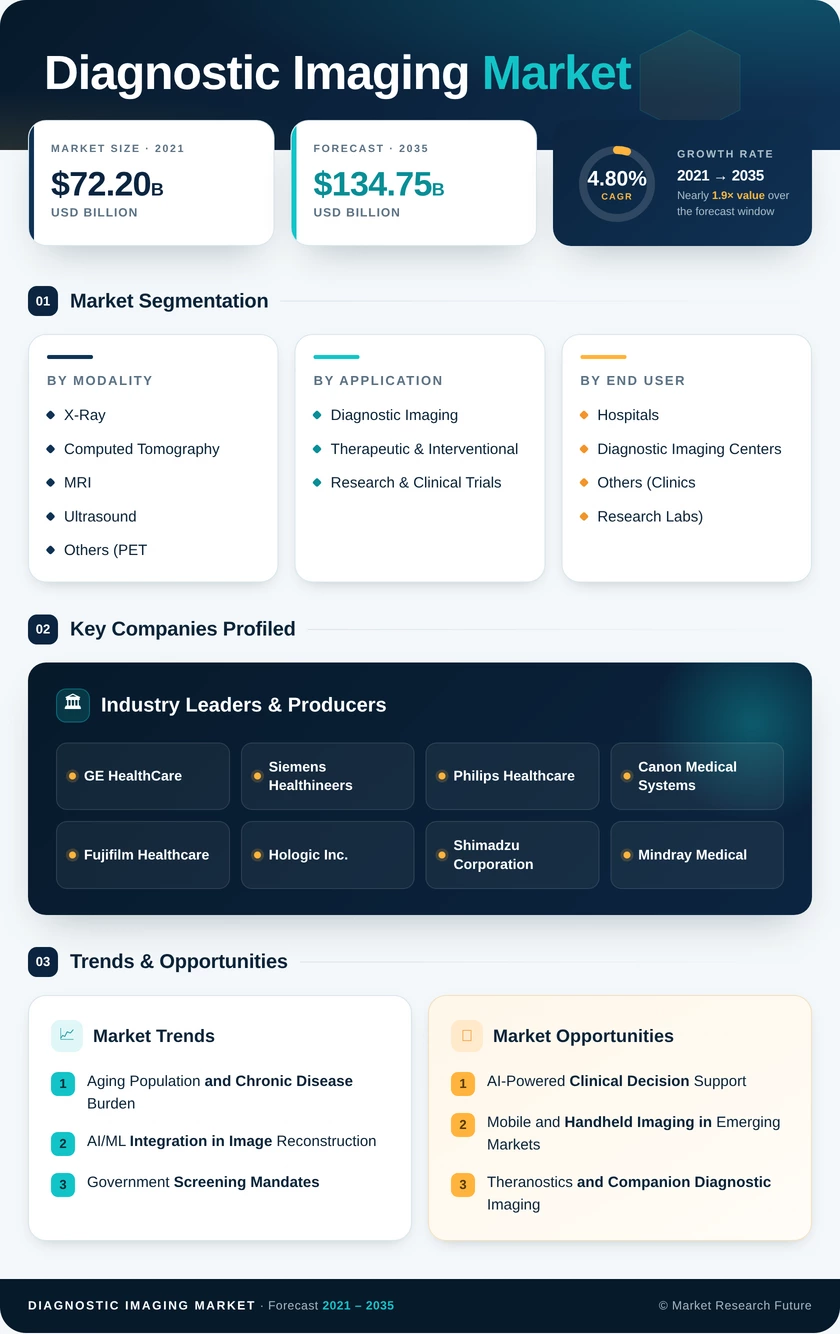

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Modality | X-Ray, Computed Tomography, MRI, Ultrasound, Others (PET, SPECT, Mammography) | X-Ray | Computed Tomography |

| By Application | Diagnostic Imaging, Therapeutic & Interventional, Research & Clinical Trials | Diagnostic Imaging | Therapeutic & Interventional |

| By End User | Hospitals, Diagnostic Imaging Centers, Others (Clinics, Research Labs) | Hospitals | Diagnostic Imaging Centers |

Market Segmentation Overview

By Modality

| Sub-Segment | Key Trend |

| X-Ray | Flat-panel digital detector replacement cycle; dose-reduction algorithms |

| Computed Tomography | Photon-counting detector transition; AI-assisted triage |

| MRI | Helium-free magnet adoption; ultra-high-field clinical expansion |

| Ultrasound | Handheld and portable devices; edge-AI embedded processing |

| Others (PET, SPECT, Mammography) | Theranostics-driven PET demand; 3D tomosynthesis screening |

X-ray continues to lead by installed-base volume, while computed tomography captures the strongest growth trajectory as spectral and AI capabilities expand clinical utility across emergency, oncology, and cardiology settings.

By Application

| Sub-Segment | Key Trend |

| Diagnostic Imaging | Screening program expansion; population-health analytics integration |

| Therapeutic & Interventional | Hybrid OR adoption; image-guided minimally invasive procedures |

| Research & Clinical Trials | Imaging biomarkers as surrogate endpoints; multi-center standardization |

Diagnostic applications dominate the application landscape with the largest share, while therapeutic and interventional use cases are gaining as real-time image guidance becomes essential in surgical and interventional suites.

By End User

| Sub-Segment | Key Trend |

| Hospitals | Multi-modality integration; enterprise PACS migration |

| Diagnostic Imaging Centers | Payer-driven outpatient shift; as-a-service procurement models |

| Others (Clinics, Research Labs) | Specialty-practice adoption of portable imaging; academic research funding |

Hospitals maintain the dominant position through comprehensive service lines and 24/7 operational requirements, while freestanding diagnostic imaging centers capture the fastest growth as cost-conscious payers redirect referral patterns.