Diethylene Glycol (DEG) Market Summary

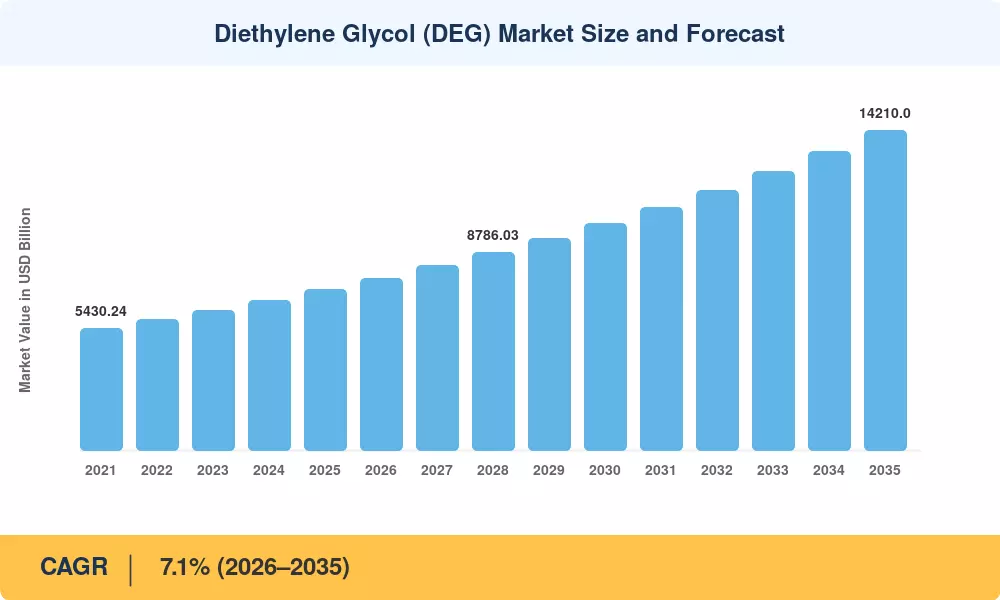

The Diethylene Glycol Market reached an estimated USD 7,150 million in 2025 and is projected to grow from USD 7,660 million in 2026 to USD 14,210 million by 2035, registering a CAGR of 7.1% during the forecast period (2026–2035). This growth trajectory reflects persistent demand for industrial glycol chemicals across construction, automotive, and packaging sectors. Government-backed infrastructure spending in Asia-Pacific—where China's 14th Five-Year Plan earmarks over USD 1.3 trillion for urbanization projects [1]—has created a structural demand floor for polyester resin materials and plasticizer chemicals that feed directly into the Diethylene Glycol Market pipeline.

A quiet but significant shift is reshaping the industrial solvent landscape. Legacy solvent formulations with higher toxicity profiles are gradually giving way to refined glycol ether materials and bio-based chemical intermediates that deliver comparable performance with improved safety margins. The European Chemicals Agency's (ECHA) revised REACH guidelines have accelerated reformulation timelines, pushing producers of antifreeze compounds and unsaturated polyester resins to invest in cleaner process technologies [2]. BASF alone committed EUR 780 million between 2023 and 2027 toward sustainable chemical processing upgrades across its Ludwigshafen complex [3].

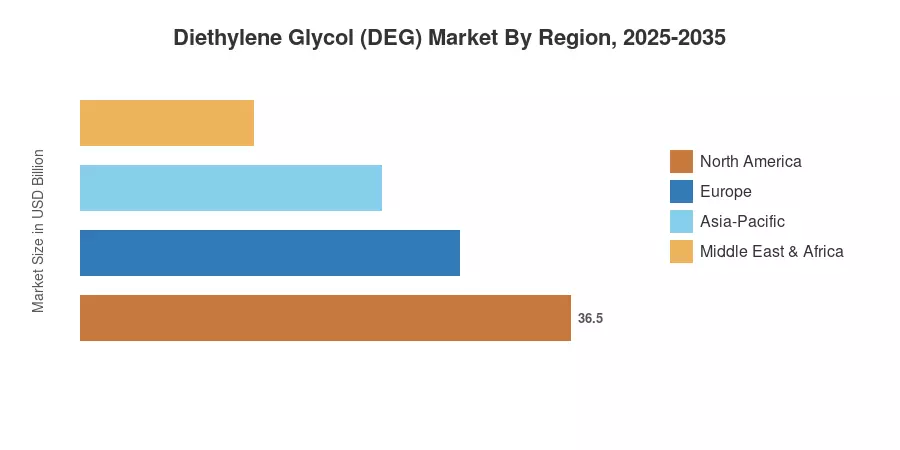

Asia-Pacific commands roughly 48% of the Diethylene Glycol Market, anchored by China and India's combined petrochemical output. The region also leads growth projections with a CAGR of 8.3% through 2035, driven by booming textile and plastics manufacturing. North America holds the second-largest share at approximately 22%, supported by shale-gas feedstock advantages that keep production costs competitive for plasticizer chemicals and related glycol derivatives. As decarbonization mandates tighten globally, the Diethylene Glycol Market stands at an inflection point where sustainability compliance will separate market leaders from laggards.

Key Report Takeaways

• By Application

- Chemical intermediates account for approximately 34% of total Diethylene Glycol Market revenue, fueled by downstream demand in PET resin and textile fiber production

- Plasticizer chemicals applications are expanding at a CAGR of 7.8%, the fastest among all application segments, reflecting rising flexible PVC consumption in construction

- Personal care applications contributed roughly USD 930 million in 2025, as glycol ether materials gained traction in cosmetics formulation

• By End-User Industry

- The plastics industry represents the dominant end-user within the Diethylene Glycol Market, holding a 38% share, driven by unsaturated polyester resins and packaging demand

- Paints and coatings end-users are growing at 7.5% CAGR through 2035, supported by infrastructure buildout across emerging economies

• By Region

- Asia-Pacific leads with 48% of the global Diethylene Glycol Market value, driven by China's petrochemical expansion and India's industrial solvent consumption

- North America captures roughly USD 1,570 million in 2025, underpinned by cost-efficient ethylene oxide feedstock from shale gas operations

- South America registers the second-fastest regional CAGR at 6.8%, as Brazil's agrochemical sector increasingly uses industrial glycol chemicals

Market Size and Forecast (2021–2035)

The market sizing methodology combines bottom-up plant capacity analysis with top-down demand modeling. Historical data (2021–2024) draws on disclosed production volumes from major chemical intermediates producers, cross-referenced with trade flow data from UN Comtrade and national customs records. Forecast projections (2026–2035) apply regression-adjusted demand curves incorporating GDP growth, construction output indices, and downstream polyester resin materials consumption trends across 35 countries.