Digital Banking Platform Market Summary

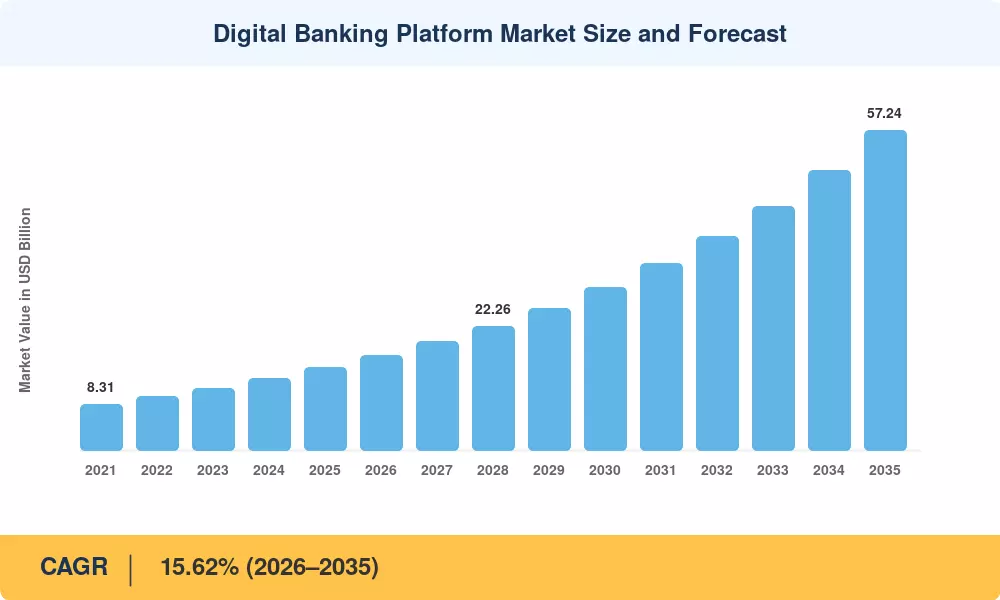

The digital banking platform market reached USD 14.85 billion in 2025 and is projected to grow from USD 17.14 billion in 2026 to USD 57.24 billion by 2035, registering a CAGR of 15.62% during the forecast period (2026–2035). Accelerating open banking mandates across the EU, UK, and Asia-Pacific — combined with over USD 35 billion in cumulative fintech venture funding since 2022 — have compressed platform refresh cycles for both retail and corporate banking segments [2]. Governments from India's Digital India initiative to Brazil's Pix instant-payments infrastructure continue to push regulatory frameworks that reward cloud-native digital banking core platforms and penalize legacy inertia.

A generational technology shift is underway. Monolithic core banking systems built in the 1990s and 2000s are giving way to API-first, microservices-based architectures that support digital onboarding and eKYC for banking alongside real-time payment rails. The European Banking Authority's 2024 guidelines on operational resilience and the U.S. OCC's fintech charter framework have jointly catalyzed an estimated USD 9.2 billion in platform modernization spending during 2024 alone [4]. AI-powered digital banking personalization engines now process behavioral data at sub-second latency, enabling hyper-targeted product recommendations that lift cross-sell conversion rates by 18–22% according to recent McKinsey benchmarks [5].

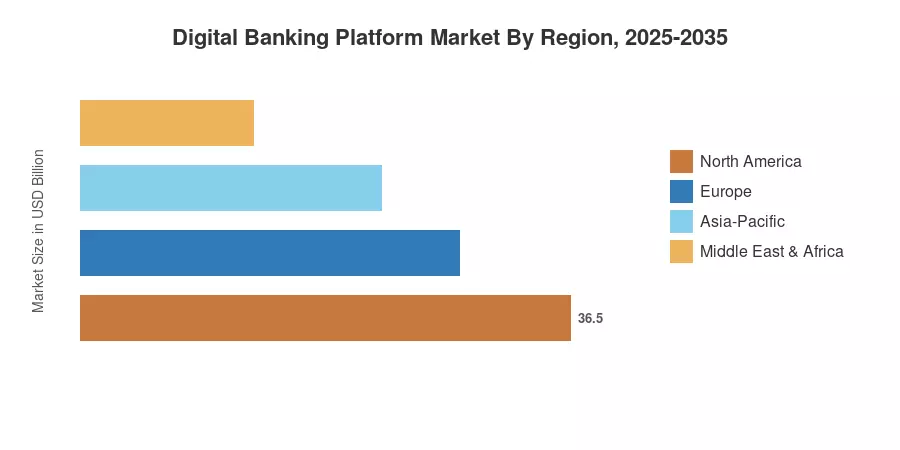

North America commands roughly 34.5% of the digital banking platform market, anchored by the depth of its neobank and challenger bank technology stack ecosystem and the density of SaaS-native vendors headquartered in the region Asia-Pacific is the fastest-growing region at a projected 17.58% CAGR, fueled by smartphone-first consumer behavior and government-led financial inclusion programs in India, Indonesia, and the Philippines. Europe holds the second-largest share at approximately 27%, driven by PSD2/PSD3 compliance requirements and open banking API for digital financial services adoption. The digital banking platform market is poised for sustained double-digit expansion as embedded finance, generative AI, and real-time payments converge into unified platform propositions.

Key Report Takeaways

• By Deployment & Component

- Cloud deployment captured 56.8% of the digital banking platform market in 2025, as institutions accelerate migration away from on-premises infrastructure toward scalable subscription models

- Platform software accounted for USD 10.17 billion in 2025, though services are expanding at the fastest pace as banks outsource integration and managed operations

- The digital banking platform market sees Banking-as-a-Service (BaaS) growing at a 17.95% CAGR, the highest among all service model segments

• By Banking Type & Access Mode

- Retail banking held a 58.6% revenue share in 2025, reflecting consumer demand for seamless digital onboarding and eKYC for banking workflows

- Mobile banking access is accelerating at an 18.32% CAGR through 2035, outpacing online/web banking as consumers shift to location-agnostic interactions

• By Region

- North America represented USD 5.12 billion in 2025 within the digital banking platform market, with the US accounting for the dominant share

- Asia-Pacific records the strongest regional CAGR at 17.58%, driven by cloud-native digital banking core platforms adoption and mobile-first populations

MRFR's market sizing employs a triangulated approach combining top-down revenue analysis from vendor financial disclosures, bottom-up adoption modeling across deployment types and banking segments, and cross-validation against central bank digitization reports and fintech investment databases.