Digital Isolator Market Summary

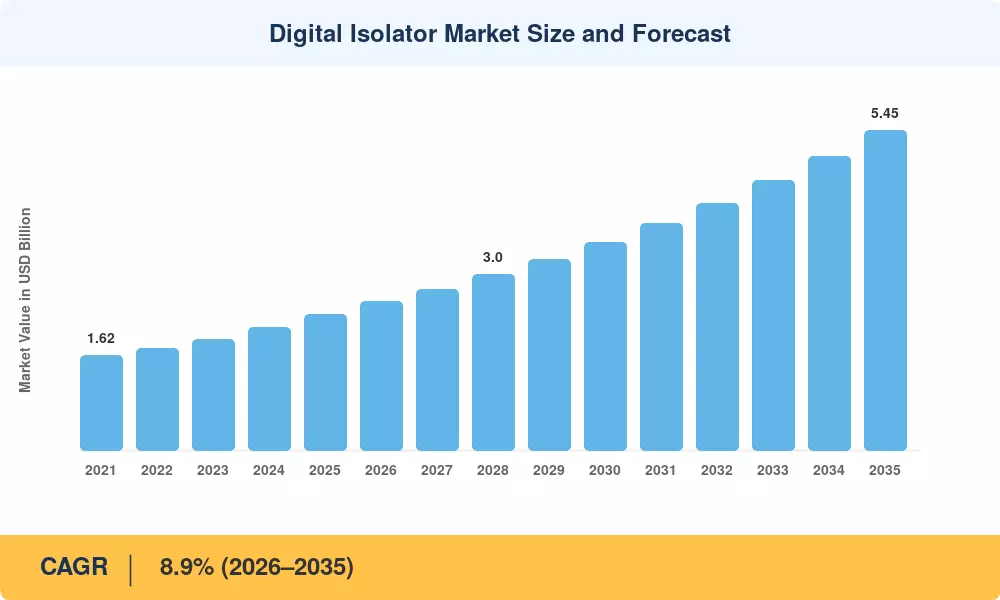

The Digital Isolator Market reached an estimated USD 2.32 Billion in 2025, setting the stage for a forecast trajectory that begins at USD 2.53 Billion in 2026 and climbs to USD 5.45 Billion by 2035 at a CAGR of 8.9%. Two forces are doing the heavy lifting here: the acceleration of Industry 4.0 capital expenditure — which exceeded USD 165 Billion globally in 2024 [1] — and stringent safety mandates across electric vehicle architectures and medical electronics. OEMs building 800 V battery platforms cannot tolerate the speed limitations and aging degradation curves of traditional optocouplers, and that shift is funneling billions into semiconductor-grade isolation.

The technology story is one of displacement. Legacy optical couplers, which have dominated galvanic barrier designs for decades, are steadily giving way to capacitive and magnetic coupling architectures that deliver data rates above 150 Mbps at a fraction of the power draw. IEC 60601-1 revisions and ISO 11452 automotive immunity standards have tightened reinforced isolation requirements, compelling Tier-1 suppliers to qualify polyimide and SiO₂-based barriers rated to 5 kVrms and beyond [2]. The Digital Isolator Market benefits directly from each regulatory revision cycle.

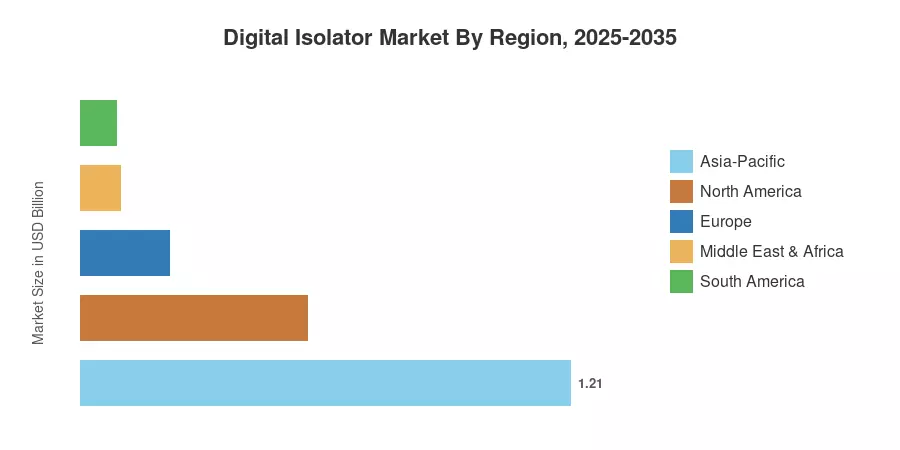

Asia-Pacific commands roughly 52% of global revenue, driven by China's factory automation build-out and India's EV production-linked incentive schemes. North America holds the second-largest share at approximately 24%, anchored by defense electronics procurement and data-center power management. Europe — the fastest-growing developed region — is expanding on the back of the EU Chips Act, which earmarked EUR 43 Billion to bolster domestic semiconductor capacity through 2030 [3]. The Digital Isolator Market is positioned to benefit from each of these regional investment waves over the coming decade.

Key Report Takeaways

• By Isolation Type

- Capacitive coupling held approximately 67% of the Digital Isolator Market revenue share in 2024, reflecting its dominance in industrial and automotive gate-driver designs.

- Giant magnetoresistive (GMR) isolation is projected to expand at a CAGR of 12.3% through 2035, driven by demand for reinforced barriers in high-voltage EV inverters.

• By End-Use Industry

- Industrial automation accounted for roughly 39% of the Digital Isolator Market share in 2024, supported by programmable-logic-controller upgrade cycles.

- Automotive applications are projected to register the highest CAGR of 13.1% through 2035, as 800 V platforms become standard across mid-range EV segments.

• By Region

- Asia-Pacific commanded more than half of global revenue, reinforced by semiconductor localization policies in China, Japan, and South Korea.

- North America retained the second-largest position, supported by defense procurement and data-center expansion.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates bottom-up revenue from isolation-IC shipment volumes against top-down semiconductor TAM benchmarks published by the World Semiconductor Trade Statistics (WSTS) association. All historical figures are reconciled against company-reported analog/mixed-signal revenue disclosures [4].