Pharmaceutical Isolator Market Summary

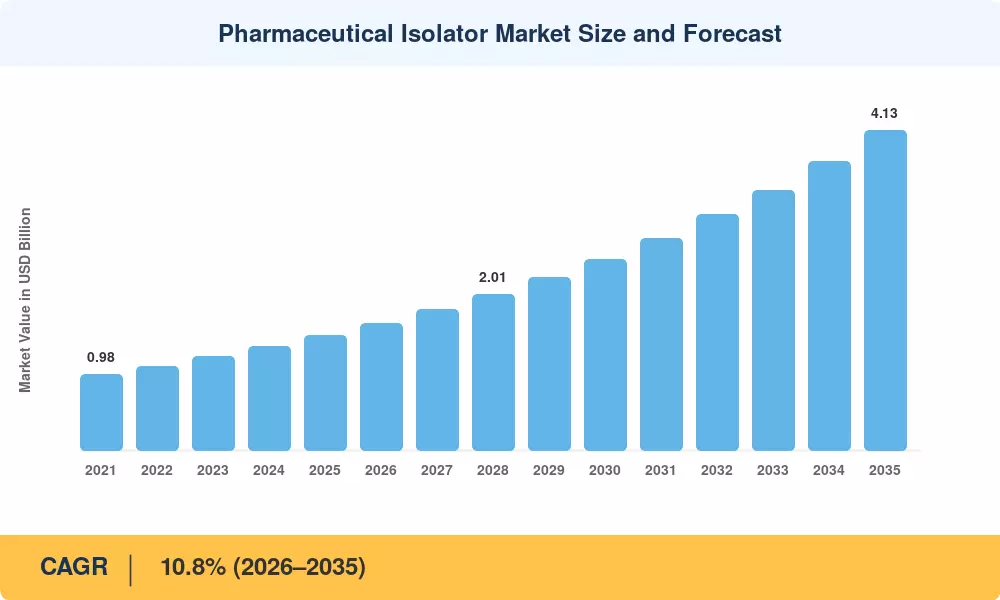

The Global Pharmaceutical Isolator Market size was valued at USD 1.48 Billion in 2025, and the market is projected to reach USD 4.13 Billion by 2035, registering a CAGR of 10.8% during the forecast period 2026–2035. This growth trajectory reflects the pharmaceutical industry's accelerating shift toward contamination-free manufacturing environments, underpinned by tightening global regulatory frameworks. The revised EU GMP Annex 1, which took effect in August 2023, mandates enhanced contamination control strategies for sterile product manufacturing — a regulatory catalyst that has driven capital expenditure toward isolator-based production lines across both established and emerging drug manufacturers [1].

A pronounced technology transition is reshaping this space. Legacy open-architecture cleanroom setups — long the industry default — are giving way to closed and restricted-access barrier systems that deliver Grade A environments within smaller footprints and at lower operating costs. The Pharmaceutical Research and Manufacturers of America (PhRMA) reported that its member companies invested USD 102.3 billion in R&D during 2021 alone, with cumulative investment exceeding USD 1.1 Trillion since 2000 [2]. A meaningful share of these R&D dollars now flows into sterile processing infrastructure, including isolator procurement.

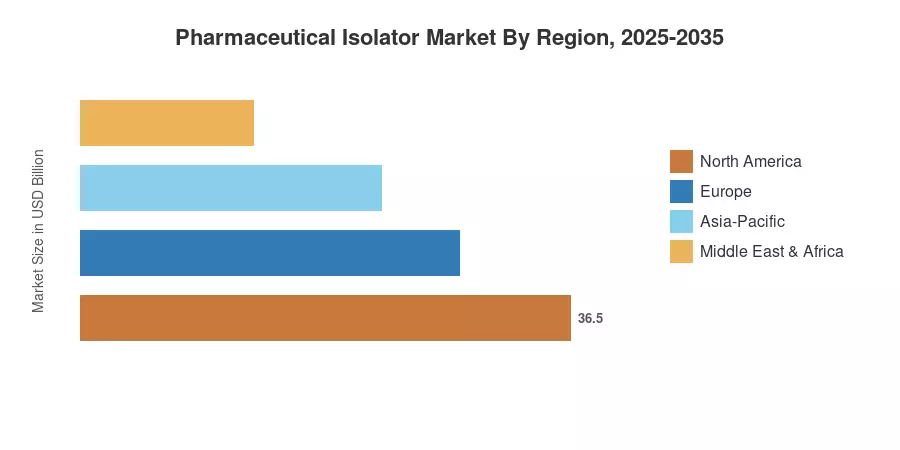

North America commands the largest share of the Pharmaceutical Isolator Market at approximately 38% of global revenue, driven by stringent FDA sterility standards and a concentrated base of biologics manufacturers. Asia-Pacific represents the fastest-growing region with a CAGR exceeding 12.4%, fueled by expanding contract manufacturing capacity in China and India. Europe holds the second-largest position, contributing roughly 29% of market revenue through its robust generic and biosimilar production ecosystem. The Pharmaceutical Isolator Market is set for sustained double-digit expansion as regulatory pressure, biologics pipelines, and facility modernization converge through 2035.

Key Report Takeaways

• By Type

- Closed Isolator Systems account for the dominant share of the Pharmaceutical Isolator Market, representing approximately 62% of global revenue in 2025 — reflecting industry preference for superior containment assurance.

- Open Isolator Systems are projected to register a CAGR of 9.6% through 2035, gaining traction in non-sterile weighing and dispensing applications.

• By Application

- Aseptic Isolators represent the largest application segment, valued at USD 0.67 Billion in 2025, driven by biologics and injectable drug manufacturing demand.

- Containment Isolators are expanding at the fastest pace within this dimension, underpinned by the rising production of high-potency active pharmaceutical ingredients (HPAPIs).

• By Region

- North America leads the Pharmaceutical Isolator Market with a 38% revenue share, anchored by FDA regulatory rigor and a high concentration of biopharmaceutical fill-finish facilities.

- Asia-Pacific is the fastest-growing regional market, expected to surpass USD 1.08 billion by 2035 as contract development and manufacturing organizations (CDMOs) scale capacity.

Pharmaceutical Isolator Market Size and Forecast (2021–2035)

Market sizing is based on a triangulated methodology combining bottom-up revenue estimates from key isolator manufacturers, top-down validation against pharmaceutical capital expenditure benchmarks, and cross-referencing with industry data from the sources. All forecast projections use a compound annual growth rate model calibrated to the 2026–2035 window.