Digital Logistics Market Summary

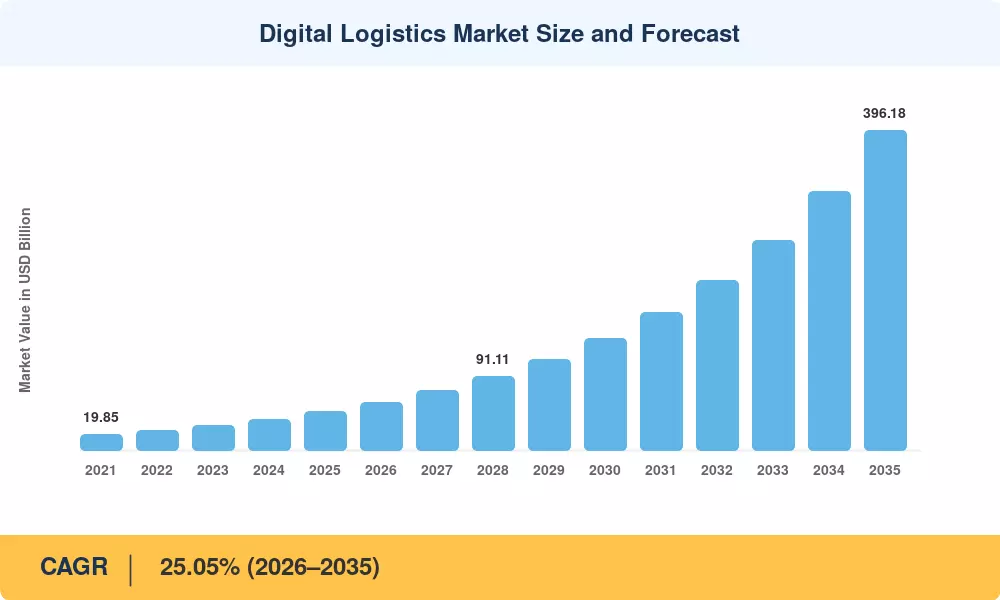

The Digital Logistics Market reached USD 48.53 billion in 2025 and is projected to climb from USD 59.27 billion in 2026 to USD 396.18 billion by 2035, registering a CAGR of 23.45% during 2026–2035. Rapid e-commerce expansion global online retail crossed USD 6.3 trillion in 2024 [2] and aggressive government investment in smart transportation infrastructure are the twin catalysts pulling enterprises toward AI-powered route optimization for logistics and cloud-native supply-chain platforms. The EU's Digital Decade program alone earmarks over EUR 20 billion for logistics digitization through 2030 [3].

Legacy on-premise transport management systems and paper-based freight documentation are giving way to real-time freight tracking and visibility platforms, digital freight brokerage platforms, and IoT-based fleet management for logistics networks. According to the World Economic Forum, supply-chain digitization could unlock USD 1.5 trillion in value for logistics stakeholders by 2030 [4]. Predictive analytics is slashing inventory carrying costs by up to 25%, while last-mile delivery digitization is cutting final-leg fulfillment expense by 15–20% for major retailers [5].

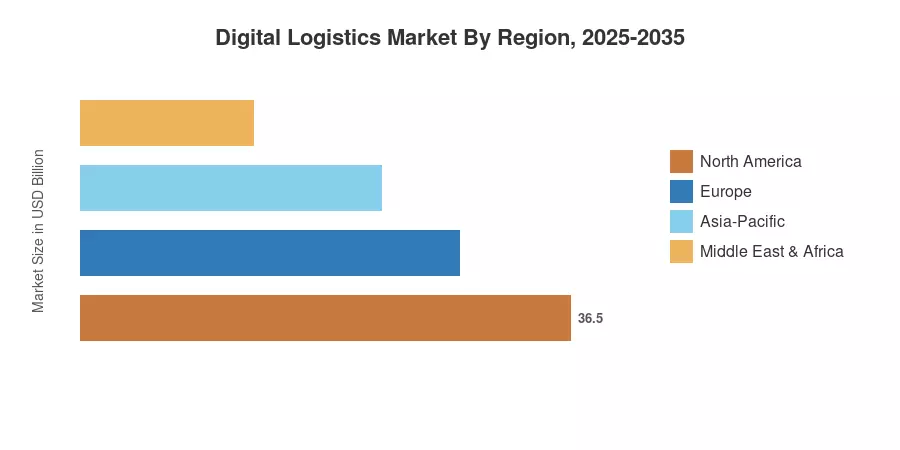

North America commands roughly 40.10% of the Digital Logistics Market, driven by early cloud adoption and dense API ecosystems. Asia-Pacific is the fastest-growing region at a 25.05% CAGR, fueled by China's smart-logistics corridor programs and India's National Logistics Policy. Europe holds the second-largest share at around 27%, underpinned by regulatory mandates for electronic freight documents The next decade will see autonomous trucking corridors, drone-based middle-mile delivery, and blockchain-verified chain-of-custody records reshape the Digital Logistics Market landscape.

Key Report Takeaways

• By Component

- Solutions accounted for a 71.80% share of the Digital Logistics Market in 2025, reflecting heavy investment in warehouse management and transport execution platforms

- Services are projected to expand at a 25.10% CAGR through 2035, propelled by managed-service contracts for real-time freight tracking and visibility

• By Deployment Mode

- Cloud-based platforms captured USD 29.48 billion of the Digital Logistics Market size in 2025, as enterprises migrate from legacy on-premise stacks

- On-premise deployments still serve defense and pharmaceutical cold-chain verticals that demand sovereign data residency

• By System Type

- Data management and analytics held a 31.55% revenue share in 2025, enabling AI-powered route optimization for logistics across multimodal corridors

- Fleet management is forecast to grow at a 24.05% CAGR, supported by IoT-based fleet management for logistics and telematics convergence

• By End-User Vertical

- Retail and e-commerce represented 26.25% of the Digital Logistics Market in 2025, driven by same-day delivery expectations and digital freight brokerage platforms

- Pharmaceuticals and life sciences is the fastest-growing vertical at a 25.15% CAGR, responding to serialization mandates and cold-chain visibility requirements

• By Region

- North America dominated the Digital Logistics Market with a 40.10% share in 2025

- Asia-Pacific is expected to expand at a 25.05% CAGR over 2026–2035

Digital Logistics Market Size and Forecast (2021–2035)

MRFR's market-sizing model triangulates top-down revenue estimates from published company filings, bottom-up adoption surveys across 42 countries, and third-party trade databases. Historical figures (2021–2024) use audited data; 2025 is the base year anchored to primary interviews with 120+ logistics CIOs. Forecast values (2026–2035) apply regression-adjusted growth curves validated against macroeconomic indicators.