Digital Marketing Software Market Summary

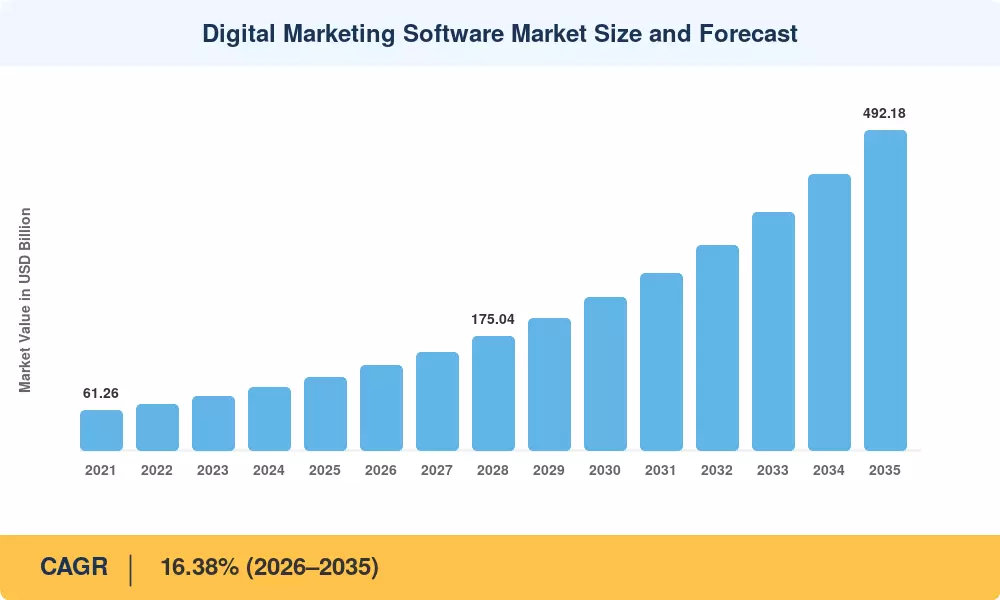

The Digital Marketing Software Market stood at USD 112.39 billion in 2025 and is projected to reach USD 130.07 billion in 2026 before climbing to USD 492.18 billion by 2035, expanding at a 16.38% CAGR across the forecast period. Surging enterprise investment in generative-AI content engines, zero-party data collection frameworks, and embedded marketing modules inside vertical SaaS platforms has propelled the Digital Marketing Software Market into one of the fastest-evolving segments of enterprise technology. Governments across the EU and Asia-Pacific have tightened consent-based data regulations, pushing brands toward first-party data architectures and privacy-centric marketing automation tools that comply with GDPR, India's DPDP Act, and comparable statutes [2].

Legacy on-premise digital campaign management suites are rapidly giving way to cloud-native platforms that unify SEO SEM software, programmatic advertising, and customer-data orchestration in a single workspace. Global enterprise spending on marketing technology surpassed USD 148 billion in 2024, with nearly 63% allocated to cloud-delivered solutions, underscoring the structural shift from capital expenditure to operating expenditure. Multi-channel marketing tools now integrate CRM, commerce, and payment rails, collapsing what once required five or six point solutions into a unified revenue engine.

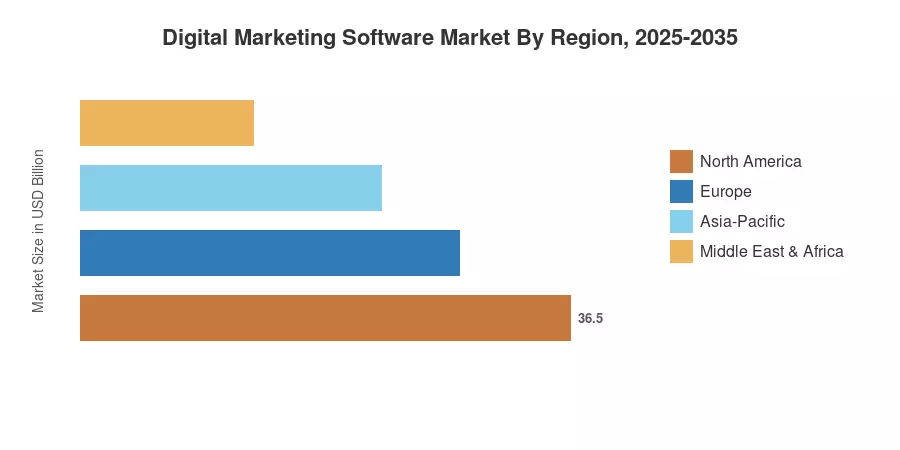

North America commands roughly 38% of the Digital Marketing Software Market revenue, buoyed by the concentration of hyperscale adtech vendors and aggressive programmatic-ad budgets. Asia-Pacific is the fastest-growing region at a 17.41% CAGR, driven by mobile-first commerce adoption in India, Southeast Asia, and China. Europe holds the second-largest share at approximately 26%, with demand anchored by GDPR-driven investment in consent management and online advertising platforms The next decade will reward vendors that embed AI-driven personalization directly into transactional workflows.

Key Report Takeaways

• By Deployment

- Cloud solutions captured a 74.12% share of the Digital Marketing Software Market in 2025, accelerating as enterprises migrate digital campaign management workloads off legacy servers

- On-premise deployments are projected to grow at a 12.47% CAGR through 2035, sustained by regulated industries requiring data residency

• By Component

- Services revenue is advancing at a 17.26% CAGR as organizations budget for implementation, training, and managed-service bundles around marketing automation tools

- The software component represented USD 67.58 billion in 2025, driven by demand for SEO SEM software and real-time analytics dashboards

• By Enterprise Size

- SMEs are forecast to post the fastest growth in the Digital Marketing Software Market at a 16.72% CAGR through 2035, fueled by self-serve onboarding and usage-based pricing

• By End-User Industry

- Retail and e-commerce held a 30.18% revenue share in 2025, the largest single vertical

- Healthcare and life sciences are on track for a 17.24% CAGR, the fastest sectoral growth rate

• By Region

- North America contributed USD 42.71 billion in 2025 revenue

- Asia-Pacific is tracking a 17.41% CAGR on the strength of mobile-first commerce and expanding digital ad spend across India and ASEAN markets

Market Size and Forecast (2021–2035)

MRFR's proprietary sizing model integrates vendor revenue disclosures, enterprise IT spending surveys, ad-platform billing data, and macroeconomic indicators. Historical figures (2021–2024) are triangulated against audited financials; forecast values (2026–2035) apply a calibrated compound growth trajectory anchored to verified base-year demand.