Digital Signage Media Player Market Summary

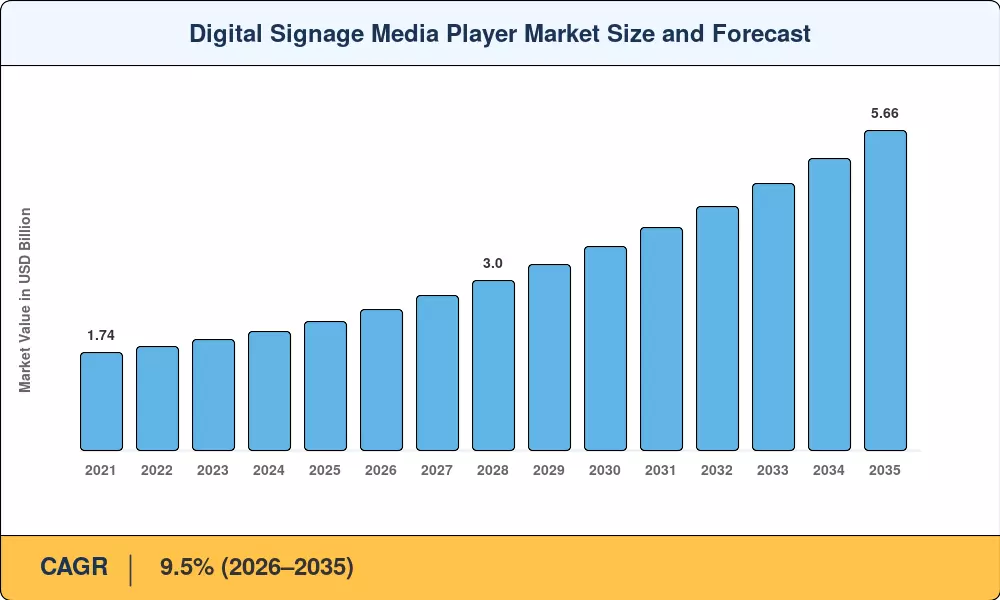

The digital signage media player market reached USD 2.28 billion in 2025, with the forecast period beginning at USD 2.50 billion in 2026 and climbing to USD 5.66 billion by 2035 at a 9.5% CAGR. Two catalysts are accelerating demand: first, retail and transportation operators are under pressure to deliver personalized, data-driven content at the screen level — a shift that demands dedicated media processing hardware and cloud-managed software. Second, government-backed smart-city programs across Asia, Europe, and North America are channeling billions into connected public-information infrastructure, pulling digital signage deployments into transit stations, municipal buildings, and urban wayfinding networks [1].

The technology transformation reshaping the digital signage media player market centers on the migration from legacy PC-based playback systems to compact System-on-Chip (SoC) and ARM-based appliances. These next-generation players integrate 4K and 8K decoding, on-device AI for content triggering, and Wi-Fi 6/6E connectivity into fanless enclosures that fit behind commercial displays. Major display OEMs are embedding playback silicon directly into panels, compressing the value chain and forcing standalone player vendors to compete on software ecosystems, analytics dashboards, and cybersecurity features [2].

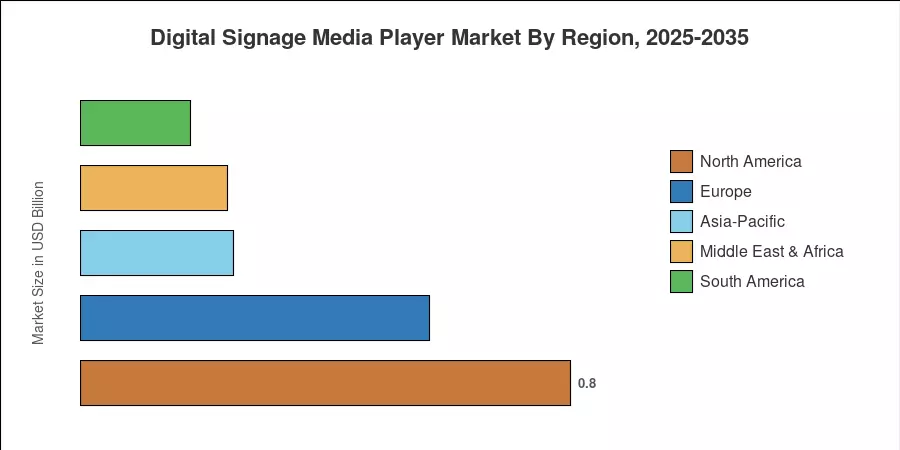

North America commands roughly 35.1% of the digital signage media player market, driven by mature retail chains and corporate campus digitization. Asia-Pacific exhibits the fastest growth trajectory at an 11.1% CAGR, fueled by China's and India's rapid expansion of transit and retail signage networks. Europe holds the second-largest share at approximately 25.0%, with strong demand from hospitality and government verticals. As edge-AI capabilities mature and panel prices continue to fall, the addressable base is widening to small and mid-sized enterprises that previously relied on static signage.

Key Report Takeaways

• By Component

- Hardware accounted for 65.8% of the digital signage media player market in 2025, reflecting the installed base of standalone players and SoC modules.

- Software platforms are expanding at a 10.8% CAGR through 2035, driven by recurring SaaS licensing and cloud-based content management.

• By Product

- Advanced-level units captured 43.1% of revenue in 2025, serving mid-tier retail and corporate deployments.

- Enterprise-level solutions are projected to grow at an 11.0% CAGR as large organizations adopt centralized, analytics-rich platforms.

• By Application

- Retail held 33.8% of the digital signage media player market size in 2025, reflecting point-of-purchase and in-store engagement spending.

- Transportation is rising at a 10.3% CAGR through 2035, accelerated by airport and rail station modernization programs.

• By Region

- North America commanded 35.1% of revenue in 2025, led by U.S. retail and corporate verticals.

- Asia-Pacific exhibits the top CAGR at 11.1%, propelled by smart-city infrastructure rollouts in China and India.

Market Size and Forecast (2021–2035)

Market Research Future employs a blended methodology combining bottom-up revenue tracking of media player shipments, software subscription billings, and top-down validation against macroeconomic indicators, including commercial construction activity, retail capex cycles, and public-infrastructure budgets. Historical figures (2021–2024) reflect audited shipment data; forecast values (2026–2035) apply a calibrated 9.5% CAGR anchored to the 2025 base year.