Digital Signage Market Summary

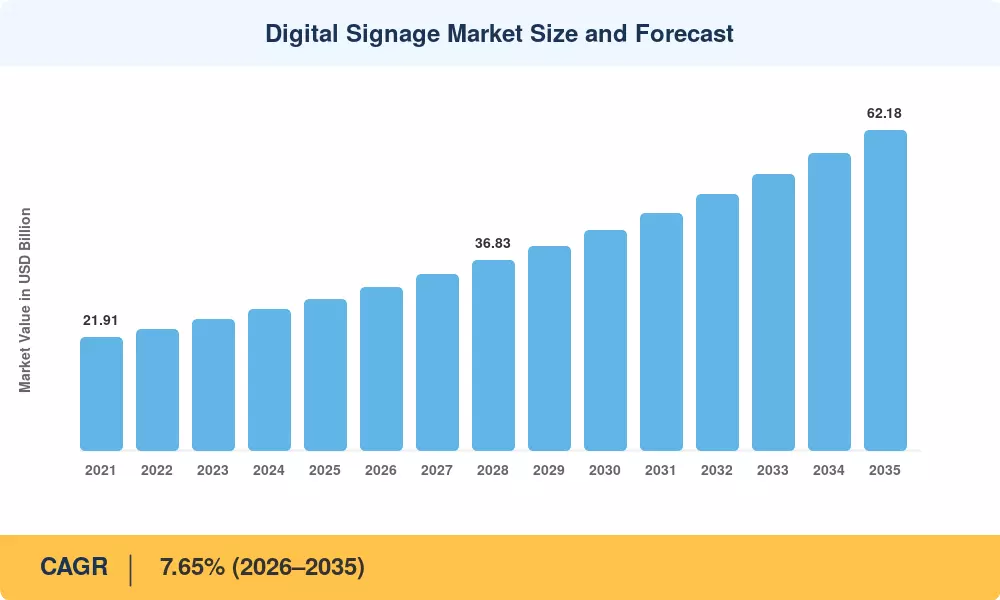

The Digital Signage Market was valued at USD 29.42 billion in 2025 and is projected to reach USD 31.85 billion in 2026 before climbing to USD 62.18 billion by 2035, registering a CAGR of 7.65% during 2026–2035. Accelerating smart-city budgets — the U.S. Bipartisan Infrastructure Law alone earmarked over USD 65 billion for broadband and digital infrastructure through 2026 — have made outdoor LED digital signage displays a core component of urban mobility and public-safety networks [2]. Retailers, meanwhile, are channeling capital into interactive touchscreen digital signage that doubles as a retail-media revenue stream, turning passive screens into programmatic content for digital signage ad exchanges [3].

The Digital Signage Market is being revolutionized by a technology pivot from hardware replacing static posters to AI-driven, cloud-managed digital signage networks. Legacy single-loop USB players are replaced with edge-compute media players with computer-vision analytics. MicroLED and fine-pitch LED panels replace LCD video walls in high-ambient-light corridors. Samsung’s USD 1.7 billion display-fab expansion in Vietnam highlights the supply-side commitment to next-gen panel capacity [4]. Direct-view LED arrays are now 40% more power-efficient than comparable LCD-backlit systems, enabling capital budgets to meet ESG reporting requirements.

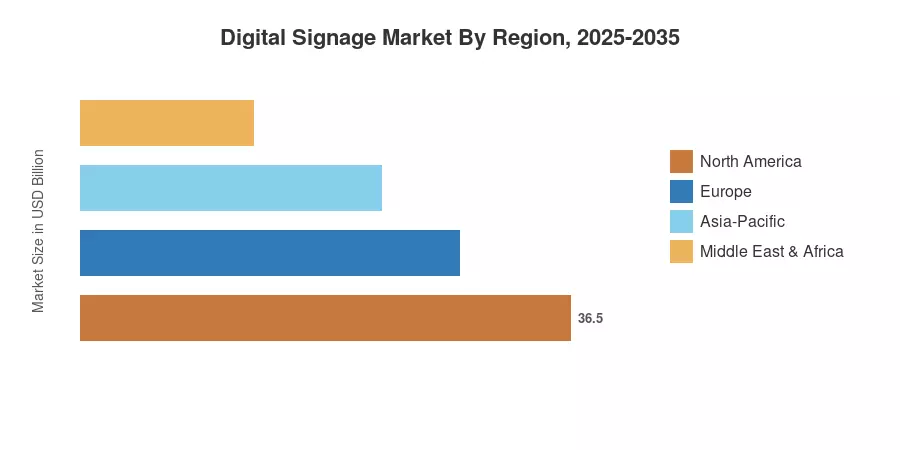

North America accounted for ~35% of the 2025 Digital Signage Market revenue, led by dense retail-media ecosystems and corporate workspace modernization Asia-Pacific is expected to witness the highest growth rate of 7.78% during the forecast period, owing to the national program of “Smart Transportation” in China and Digital India in India. Europe had the second greatest proportion, at over 26 %, driven by the EU’s Digital Decade ambitions for connected public places. The Digital Signage Market is set for continued double-digit investment inflows far into the 2030s, driven by the confluence of 5G rollout, AI-powered audience analytics, and sustainability regulation.

Key Report Takeaways

• By Component

- Hardware accounted for roughly 64% of the 2025 Digital Signage Market revenue, reflecting the capital intensity of outdoor LED digital signage displays and large-format video walls

- Software platforms — including cloud-managed digital signage networks and CMS suites — are expanding at a 9.58% CAGR through 2035, the fastest among component segments

• By Type

- Video walls represented approximately USD 8.12 billion in 2025, while kiosks featuring interactive touchscreen digital signage are tracking a 8.42% annual growth rate

• By Deployment

- On-premise deployments led the Digital Signage Market with a 73% revenue share in 2025. Yet, cloud-based platforms are registering a 11.58% CAGR as operators shift to programmatic content for digital signage delivery

• By End-Use

- Retail remained the top end-use vertical at roughly 23% of 2025 revenue, leveraging digital signage for retail wayfinding and promotions

- Transportation displays are growing at a 8.49% CAGR, fueled by real-time passenger-information mandates across metro systems worldwide

• By Regional

- North America generated approximately USD 10.30 billion in 2025 Digital Signage Market spend

- Asia-Pacific leads growth at a 7.78% CAGR, with China and India collectively accounting for over 55% of regional revenue

- The Middle East & Africa represent the smallest share but are expanding rapidly as Gulf states invest in smart-tourism signage infrastructure

Market Size and Forecast (2021–2035)

The market-size series below combines MRFR primary surveys, vendor revenue disclosures, and secondary validation against industry association shipment data. Historical figures (2021–2024) reflect actual reported values; 2025 is the base year; 2026–2035 values are forecast using a calibrated compound growth model at a 7.65% CAGR.

.webp?v=1785759181)