Digital Trust Market Summary

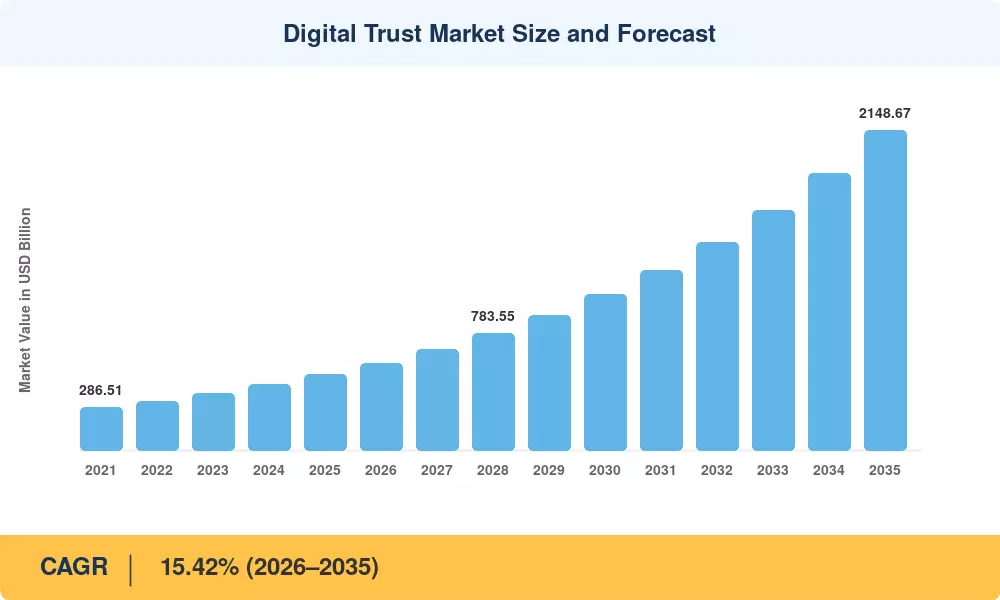

The Digital Trust Market reached an estimated USD 508.52 Billion in 2025 and is projected to grow from USD 590.14 Billion in 2026 to USD 2,148.67 Billion by 2035, registering a CAGR of 15.42% during the forecast period (2026–2035). This acceleration is anchored in a regulatory groundswell — the EU's Digital Operational Resilience Act (DORA) enforcement timeline and the U.S. SEC's four-business-day cyber-disclosure mandate have made identity-centric controls a boardroom imperative [1]. Enterprise spending on cybersecurity compliance for digital trust surpassed USD 68 Billion globally in 2024, reflecting how deeply governance mandates now shape procurement cycles.

Legacy perimeter-based security architectures are giving way to continuous authentication frameworks built around a zero-trust security framework for enterprises. Over 78% of breaches in 2024 involved compromised credentials, pushing organizations toward public key infrastructure PKI for digital trust and passwordless access models [2]. Cloud migration has consolidated identity providers, and AI-powered threat detection is reshaping vendor roadmaps — Gartner estimates that 60% of large enterprises will have adopted ML-driven identity analytics by 2027. The Digital Trust Market is evolving from point-product procurement to platform-led managed services integrating threat intelligence, digital signature and certificate authority trust issuance and automated compliance reporting.

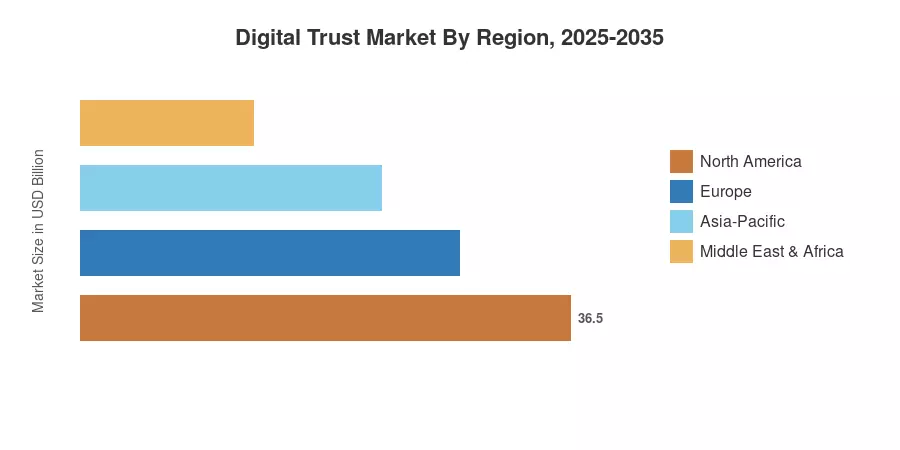

North America commands roughly 41% of the global Digital Trust Market revenue, driven by mature regulatory frameworks and Fortune 500 security budgets. Asia-Pacific stands as the fastest-growing region with a CAGR exceeding 16.3%, propelled by India's Digital Personal Data Protection Act and China's expanding cybersecurity standards regime [4]. Europe holds the second-largest share at approximately 27%, underpinned by GDPR enforcement momentum and the eIDAS 2.0 digital identity wallet rollout. As blockchain-based digital trust verification gains enterprise traction and quantum-safe cryptography moves from labs to production, the Digital Trust Market is poised for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Component

- Solutions captured approximately 62% of Digital Trust Market revenue in 2025, reflecting strong demand for integrated identity platforms and public key infrastructure PKI for digital trust deployments

- Services are advancing at a 16.18% CAGR through 2035, as managed security offerings that bundle cybersecurity compliance for digital trust with threat intelligence gain traction among mid-market buyers

• By Deployment Mode

- Cloud-based deployments commanded over USD 375 Billion of the 2025 Digital Trust Market spending, driven by hybrid-workforce identity orchestration needs

- On-premises solutions continue to serve regulated verticals requiring data sovereignty, particularly government and defense environments

• By Organization Size

- Large enterprises accounted for a 15.07% CAGR through the forecast period, scaling a zero-trust security framework for enterprises across distributed cloud estates

- Small and medium-sized enterprises are the fastest-adopting cohort at a 16.05% CAGR, fueled by affordable SaaS-delivered digital signature and certificate authority trust solutions

• By End-User Industry

- BFSI led with approximately 35% of the 2025 Digital Trust Market demand, reflecting stringent KYC/AML identity verification mandates

- Retail and e-commerce is the quickest-growing vertical, driven by consumer-facing digital identity and blockchain-based digital trust verification for supply-chain provenance

• By Region

- North America captured the largest share of the Digital Trust Market in 2025, underpinned by federal zero-trust mandates and enterprise cloud maturity

- Asia-Pacific is scaling at a 16.32% CAGR, with India, China, and ASEAN markets channeling billions into national digital identity frameworks

MRFR's proprietary sizing framework triangulates bottom-up vendor revenue tracking, top-down TAM modeling, and primary interviews with 120+ CISOs and identity-security procurement leads across 14 countries. Historical figures (2021–2024) use reported spending; the 2025 base year blends actuals with Q4 estimates; and 2026–2035 values apply the calibrated 15.42% CAGR adjusted for adoption-curve inflection points.