Direct Methanol Fuel Cell Market Summary

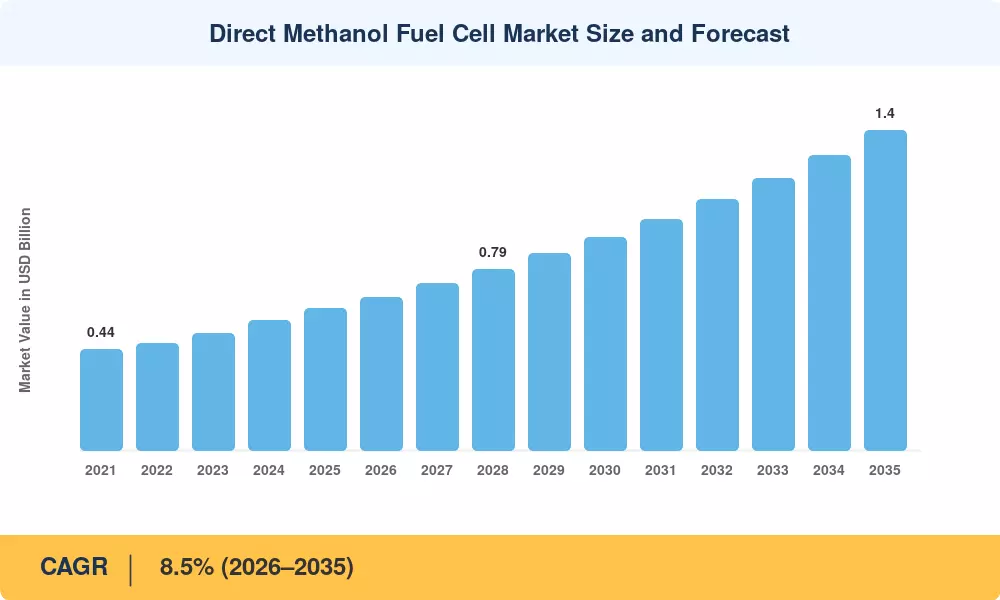

The Direct Methanol Fuel Cell Market reached an estimated USD 0.62 billion in 2025 and is projected to grow from USD 0.67 billion in 2026 to USD 1.40 billion by 2035, registering a CAGR of 8.5% during the forecast period. This expansion is anchored in a global push toward portable, clean power alternatives — a shift catalyzed by programs such as the U.S. Department of Energy's Hydrogen and Fuel Cell Technologies Office, which allocated over USD 150 million toward portable fuel cell R&D between 2022 and 2025 [1]. Military modernization budgets across NATO countries have also redirected investment toward lightweight power solutions for dismounted soldiers, accelerating procurement cycles for DMFC-based systems.

It’s not just lithium-ion batteries in the off-grid and portable space anymore; the technology landscape is changing. DMFCs are an attractive alternative due to the ability to instantly refill using methanol cartridges; they operate silently and have higher energy densities than traditional battery chemistries for longer missions. The European Commission’s Clean Hydrogen Joint Undertaking has invested EUR 200 million for demonstrations of portable and tiny fuel cells[2] through its Horizon Europe work programme. These legislative tailwinds are altering the competitive calculation for OEMs looking at next-generation portable energy designs.

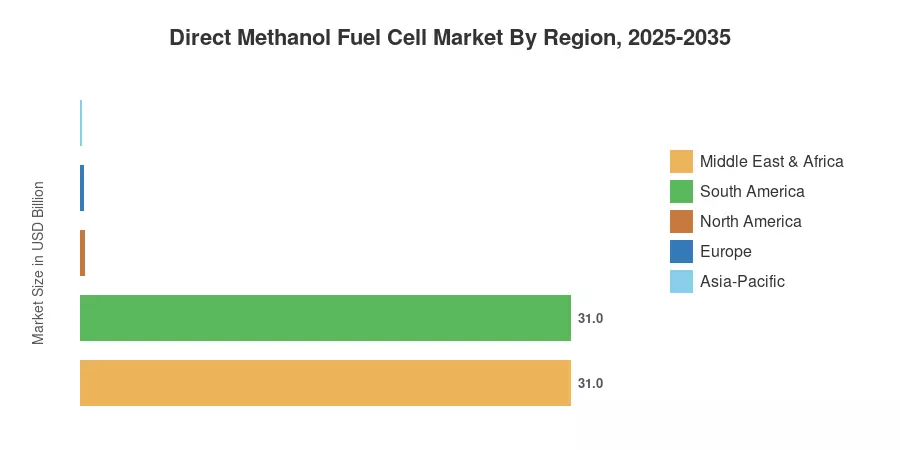

North America is projected to account for around 38% of the Direct Methanol Fuel Cell Market share due to defense procurement and telecom backup power requirements. Asia-Pacific is the fastest-growing area, with an expected CAGR of 10.2% due to aggressive hydrogen economy roadmaps in Japan and South Korea. Europe has a stake of about 27%, with Germany’s fuel cell manufacturing environment leading the way. Falling prices of catalysts and better durability of membranes mean the Direct Methanol Fuel Cell Market should keep growing until 2035.

Key Report Takeaways

• By Type

- Active DMFC systems account for approximately 55% of the Direct Methanol Fuel Cell Market, driven by higher power output capabilities for military and telecom applications.

- Passive DMFC configurations are the fastest-growing type segment at 9.8% CAGR, benefiting from simplified system design for consumer electronics and IoT sensors.

• By Application

- The portable power segment generated an estimated USD 217 million in 2025, reflecting strong demand across defense, emergency response, and recreational markets.

- Military and defense applications represent the second-largest share within the Direct Methanol Fuel Cell Market, valued at approximately 25% of total revenue.

• By Geography

- North America leads with a 38% share, underpinned by DOE-funded demonstrations and U.S. Army portable power procurement contracts.

- Asia-Pacific is projected to grow at 10.2% CAGR through 2035, led by Japan's ENE-FARM successor programs and South Korean hydrogen subsidies.

- Europe holds the second-largest share at approximately 27%, with Germany's SFC Energy and broader EU hydrogen strategy anchoring regional growth.

Market Size and Forecast (2021–2035)

The sizing technique of Market Research Future (MRFR) includes bottom-up revenue modeling of component makers, system integrators and end-user procurement data, which is validated against top-down standards from IEA Hydrogen Tracking Report and DOE Annual Merit Review publications. Historical data (2021-2024) is based on actual shipment data and stated revenues, while the forecast period (2026-2035) assumes a compound annual growth rate of 8.5% based on pipeline analysis and policy commitment schedules.