Display Driver Market Summary

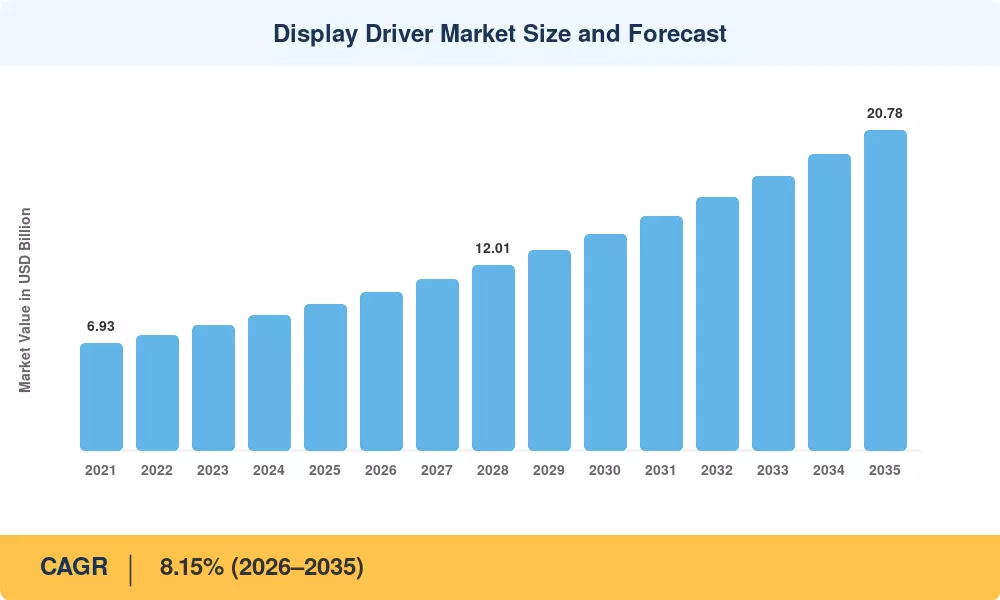

The Display Driver Market reached an estimated USD 9.49 billion in 2025 and is projected to grow from USD 10.26 billion in 2026 to USD 20.78 billion by 2035, registering an 8.15% CAGR during 2026–2035. Government-backed semiconductor self-sufficiency programs — including China's National IC Investment Fund Phase III (USD 47.5 billion committed in 2024) and the EU Chips Act's €43 billion allocation — are channeling unprecedented capital into display driver IC fabrication, anchoring demand across consumer and automotive verticals[2].

A generational technology shift is reshaping the Display Driver Market as legacy LCD gate and source driver chipsets yield ground to advanced OLED display driver IC designs built on sub-28 nm process nodes. Samsung Display and LG Display collectively committed over USD 12 billion toward Gen 8.6 OLED fab expansions between 2023 and 2025, pulling timing controller and AMOLED display driver for wearables architectures into high-volume production faster than analysts anticipated two years ago [3][4]. MicroLED display driver controller chips, though still at an early commercial scale, attracted USD 1.8 billion in venture and corporate R&D spending globally in 2024 alone [5].

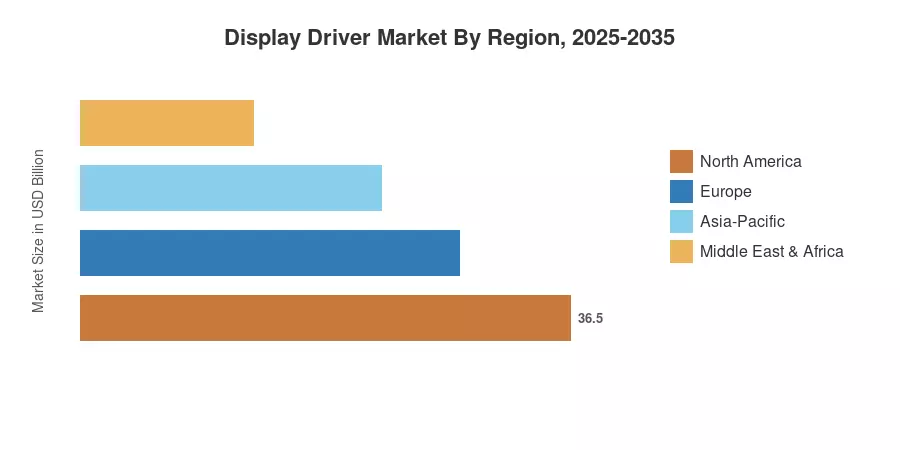

Asia-Pacific dominates the Display Driver Market with approximately 47% of global revenue in 2025, driven by China's panel manufacturing base and South Korea's OLED capacity buildout. North America holds the second-largest share at roughly 19%, buoyed by automotive-grade TFT LCD driver ICs for automotive display integration across Detroit and Silicon Valley OEMs. South America represents the fastest-growing emerging pocket, fueled by Brazil's consumer electronics tariff reforms

Key Report Takeaways

• By Form Factor

- Small- and medium-area DDICs commanded a 60.15% share of the Display Driver Market in 2025, underpinned by smartphone and tablet refresh cycles

- Flexible and foldable DDICs are forecast to expand at a 10.65% CAGR through 2035, tracking the commercial ramp of OLED display driver IC for smartphones in foldable form factors

• By Display Technology

- LCD-based driver ICs accounted for USD 5.67 billion in Display Driver Market revenue in 2025, reflecting the installed base of LCD gate and source driver chipsets across TVs and monitors

- MicroLED display driver controller chips are projected to post an 11.35% CAGR through 2035, the highest among technology segments

• By Application

- Smartphones represented 33.85% of the Display Driver Market in 2025, with OLED display driver IC for smartphones driving average selling price uplift

- Automotive displays are set to grow at a 14.15% CAGR through 2035, propelled by TFT LCD driver ICs for automotive displays in cockpit clusters and head-up displays

• By Region

- China held 47.05% of the Display Driver Market revenue in 2025, supported by BOE, CSOT, and Tianma's vertically integrated panel-driver supply chains

- South Korea is positioned for a 9.15% CAGR through 2035, as Gen 8.6 OLED fabs spur demand for advanced AMOLED display driver for wearables and smartphone panels

Market Size and Forecast (2021–2035)

MARKET RESEARCH FUTURE (MRFR)'s market sizing integrates bottom-up revenue models from 14 Tier-1 display driver IC vendors, cross-validated against foundry wafer-start data from TSMC, UMC, and DB HiTek, and triangulated with downstream panel shipment figures from DSCC and Omdia[6].