District Heating Market Summary

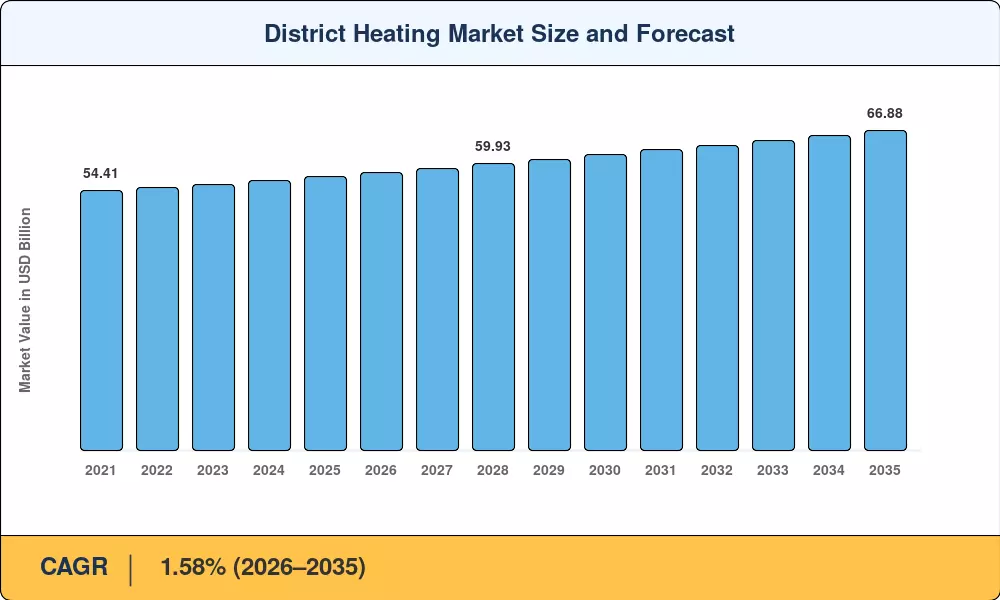

The District Heating Market was valued at USD 57.18 billion in 2025 and is projected to grow from USD 58.08 billion in 2026 to USD 66.88 billion by 2035, registering a CAGR of 1.58% during the forecast period (2026–2035). This steady expansion is rooted in two converging forces: the European Union's revised Energy Efficiency Directive mandating that member states develop national heating and cooling plans by 2026, and accelerating urbanization across Asia-Pacific cities where centralized thermal infrastructure displaces fragmented boiler installations [1]. Clean-heat mandates in Denmark, Sweden, and Finland — which collectively channel over USD 3.2 billion annually into heat-network upgrades — continue to anchor policy-driven demand [2].

A generational change in technology is taking place in the District Heating Market. The legacy high-temperature steam networks built around coal-fired boilers are being replaced by lower temperature hot water systems linked with waste-heat recovery, large-scale heat pumps and solar thermal arrays. In its 2024 World Energy Outlook, the IEA estimated that the total global investment in district energy infrastructure was over USD 18 billion in that year, with around 40% of the expenditure going towards renewable heat integration and digital load-balancing platforms [3]. This is not a change of degree but a change in the way operators monetize thermal assets.

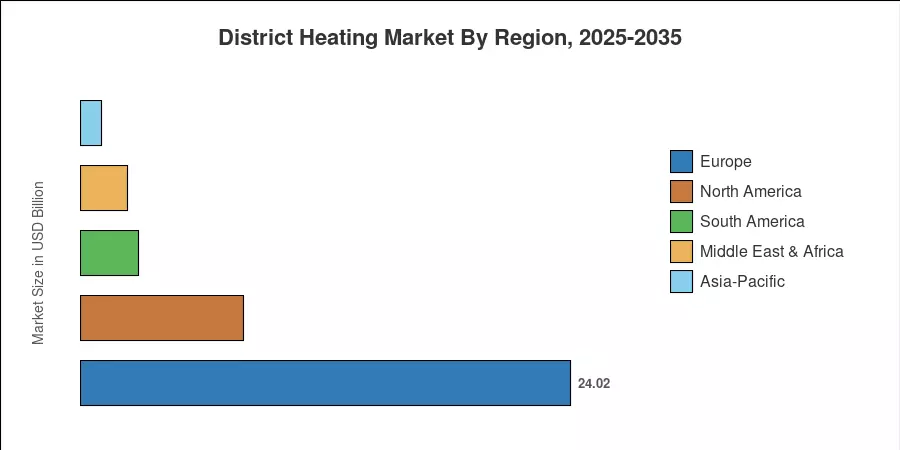

The District Heating Market in Europe took the highest share in 2025 with about 42% of the worldwide revenue, led by the established Scandinavian networks and the increasing refurbishments in Eastern Europe. Asia-Pacific is the fastest-growing market, with demand fuelled by urbanisation in China, South Korea and Japan, bringing heat-network building to new residential corridors. North America accounted for over 14% of the District Heating Market worldwide, with campus-scale systems and data-center heat-reuse pilots gaining momentum across the northern United States and Canada [4].

Key Report Takeaways

• By Plant Type

- Combined Heat and Power (CHP) plants held approximately 57.1% of the District Heating Market share in 2025, reflecting the continued dominance of cogeneration assets in European and Chinese networks.

- Waste-heat recovery units are forecast to register the fastest growth at a 4.89% CAGR through 2035, driven by industrial symbiosis programs and data-center heat capture.

• By Application

- The residential segment captured roughly 57.4% of the District Heating Market in 2025, supported by mandatory connection policies in Nordic countries.

- The industrial application segment is projected to grow at a 2.70% CAGR to 2035, fueled by process-heat electrification and decarbonization mandates in heavy industry.

• By Geography

- Europe dominated the District Heating Market with the largest revenue share in 2025, underpinned by mature regulatory frameworks and extensive pipeline networks.

- Asia-Pacific is forecast to register the quickest growth rate through 2035, led by large-scale urban heating projects in China and district cooling expansion in Southeast Asia.

Market Size and Forecast (2021–2035)

MRFR’s proprietary estimation framework combines firsthand interviews with utility operators and equipment OEMs, regulatory filings from national energy authorities and secondary statistics from IEA, Eurostat and BloombergNEF. Historical statistics (2021–2024) are reconciled against reported capital expenditures and linked building floor area; forecast figures (2026–2035) apply regression-adjusted demand modeling calibrated to national heating plans and fuel-price scenarios.