Dry Eye Syndrome Market Summary

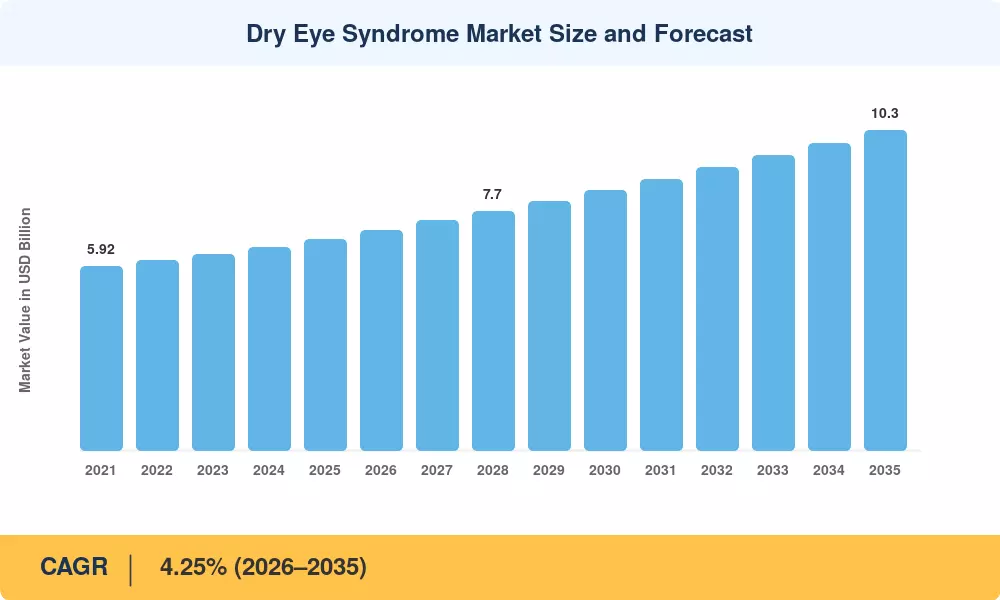

The Dry Eye Syndrome Market was valued at USD 6.80 Billion in 2025 and is projected to reach USD 7.09 Billion in 2026 before climbing to USD 10.30 Billion by 2035, registering a CAGR of 4.25% during the 2026–2035 forecast period. This trajectory is anchored in two structural tailwinds: the WHO's recognition of dry eye as a chronic condition requiring long-term management, and expanded insurance coverage mandates in the US and EU that are pulling patients from sporadic OTC purchasing into sustained prescription therapy. The global prevalence rate now exceeds 300 million diagnosed individuals, and national screening programs across Japan and South Korea are pushing that number higher each year [1].

In terms of treatment, the market for dry eye syndrome is witnessing a significant transition from lubricants that hide symptoms to drugs that alter the condition. The FDA's 2024 fast-track designations for two sustained-release tear film modulators indicate regulatory willingness to expedite approvals, while novel secretagogues, TRPM8 agonists, and RASP inhibitors are moving into late-stage pipelines [2]. Since 2022, device-drug combination platforms that combine preservative-free biologics with thermal pulsation have drawn a total of USD 1.4 billion in venture capital funding, changing the way medical professionals handle refractory situations [3].

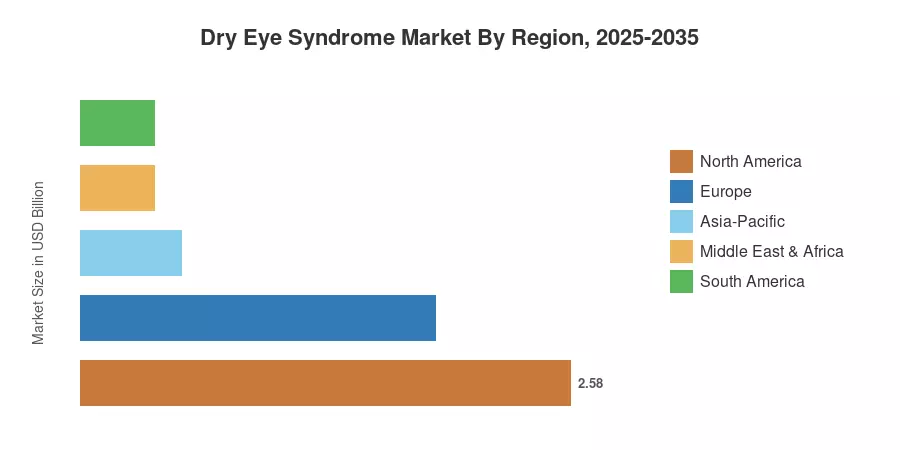

Due to its strong payer infrastructure and high diagnostic rates, North America accounted for around 38.0% of the dry eye syndrome market's revenue in 2025. Through 2035, Asia-Pacific is predicted to have the quickest CAGR at 7.84%, driven by China and India's increasing screen time and Japan's aging population. With Germany and France leading the way in the use of next-generation prescription formulations, Europe had the second-largest share at about 27.5%. Over the next ten years, the addressable patient pool will significantly increase as tele-ophthalmology fills in diagnostic gaps in underserved areas.

Key Report Takeaways

• By Treatment Modality

- Prescription therapies commanded 45.3% of the Dry Eye Syndrome Market in 2025, reflecting strong uptake of anti-inflammatory and immunomodulatory agents.

- Diagnostic testing is forecast to expand at a 7.10% CAGR through 2035, as point-of-care tear osmolarity and meibography devices become standard clinical tools.

• By Disease Type

- Evaporative dry eye cases held 56.1% of revenue in 2025, the dominant clinical subtype globally.

- Aqueous-deficient cases are projected to grow at an 8.01% CAGR to 2035, as autoimmune screening improves early detection.

• By Dosage Form

- Eye drops accounted for 70.2% of the Dry Eye Syndrome Market size in 2025

- Ointments and gels are advancing at an 8.60% CAGR through 2035 as preservative-free formulations gain clinician preference

• By Distribution Channel

- Hospital pharmacies captured 65.9% of the Dry Eye Syndrome Market revenue in 2025

- Online pharmacy channels are set to post a 10.58% CAGR through 2035 as direct-to-patient subscription models scale.

• By Region

- North America commanded 38.0% of global revenue in 2025, while Asia-Pacific is expected to register the fastest regional CAGR at 7.84% over 2026–2035

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines top-down revenue analysis from audited pharmaceutical databases with bottom-up validation through prescription volume tracking, patient prevalence models, and trade-channel surveys across 42 countries. Historical data reflect actual sales and shipment records; forecast values are extrapolated using a weighted CAGR model calibrated against clinical trial pipeline progression, regulatory approval timelines, and payer adoption curves.