Ophthalmic Drugs Market Summary

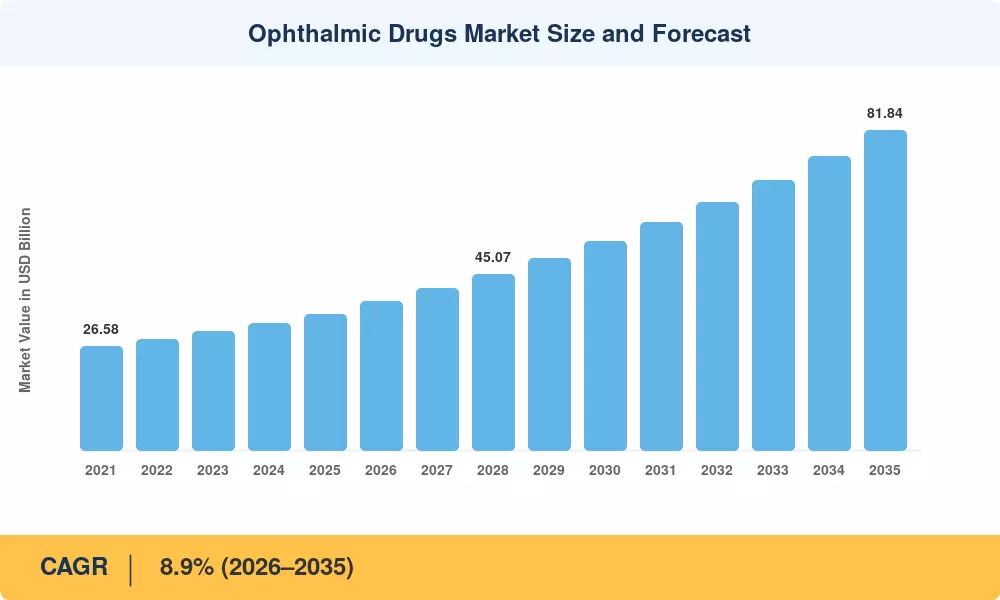

The Ophthalmic Drugs Market size was valued at USD 34.90 Billion in 2025, and the market is projected to grow from USD 38.01 Billion in 2026 to USD 81.84 Billion by 2035, registering a CAGR of 8.9% during the forecast period 2026–2035. Population aging across developed economies and a global diabetes prevalence surpassing 537 million adults are anchoring demand for chronic ocular therapies, while the US Inflation Reduction Act's drug-pricing provisions are reshaping manufacturer strategies around premium sustained-release formulations and extended-interval biologics [1].

Therapeutic innovation is revolutionizing the landscape of the Ophthalmic Drugs Market. Preservative-free unit dose systems are replacing legacy multi-dose preserved eye drops, gene treatments are being developed for inherited retinal dystrophies, and sustained release implants are moving from monthly to bi-annual injections. The FDA’s first approval of an optogenetic therapy occurred in 2024, and global ophthalmic R&D expenditure hit USD 9.2 billion, demonstrating confidence in the next-generation pipeline candidates, including complement inhibitors and RNA interference platforms [2][3].

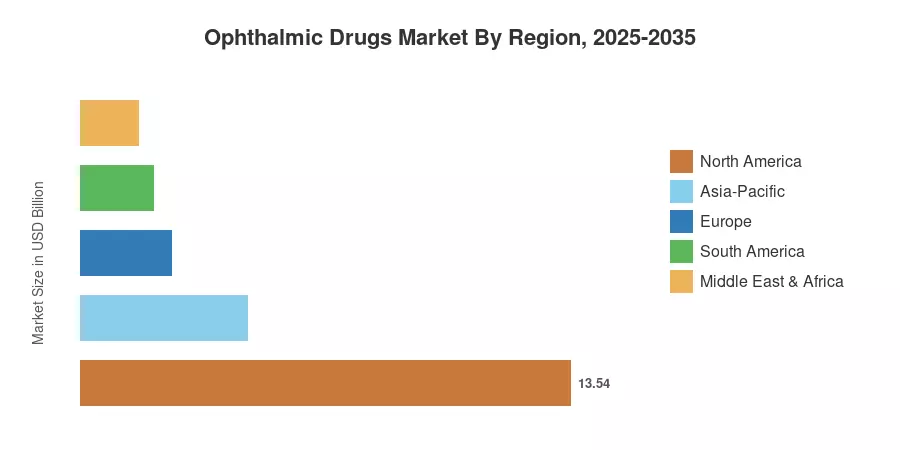

Around 38.8% of the Ophthalmic Drugs Market was contributed by North America in 2025. The region is driven by wide insurance coverage and a high density of retinal specialty clinics. Asia-Pacific is the fastest-growing area, expected to increase at a CAGR of 13.2% through 2035, with national screening initiatives in China and India uncovering vast pools of undiagnosed patients. Europe accounted for the second-highest share, aided by biosimilar entrants enabled by the EMA that are increasing access to high-cost biologics. When treatment is initiated in all locations will depend on how quickly AI-guided diagnostics are adopted in the actual world in the coming decade.

Key Report Takeaways

• By Drug Class

- Anti-glaucoma agents accounted for 25.3% of the Ophthalmic Drugs Market share in 2025, reflecting the chronic nature of intraocular-pressure management worldwide.

- Retinal disorder therapies are forecast to register a 17.6% CAGR through 2035, fueled by expanded indications for complement-pathway inhibitors.

• By Indication

- Retinal disorders captured 32.7% of the Ophthalmic Drugs Market size in 2025, as wet age-related macular degeneration and diabetic retinopathy dominate treatment spending.

• By Dosage Form

- Eye drops represented 58.7% of the Ophthalmic Drugs Market in 2025, although implants and inserts are set to grow at a 12.8% CAGR through 2035.

• By Region

- North America led the Ophthalmic Drugs Market with a 38.8% share in 2025, underpinned by robust Part B Medicare reimbursement for intravitreal injections.

- Asia-Pacific is advancing at a 13.2% CAGR, with China's National Reimbursement Drug List expansions accelerating biologics uptake.

Market Size and Forecast (2021–2035)

Market Research Future's estimates integrate primary interviews with retinal specialists and pharmacy-benefit managers, triangulated against company filings, WHO epidemiological databases, and national prescription-volume registries. Historical figures (2021–2024) reflect audited sales data; forecast figures (2026–2035) are modeled on disease-incidence trajectories, pipeline launch timelines, and regional reimbursement dynamics.