Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

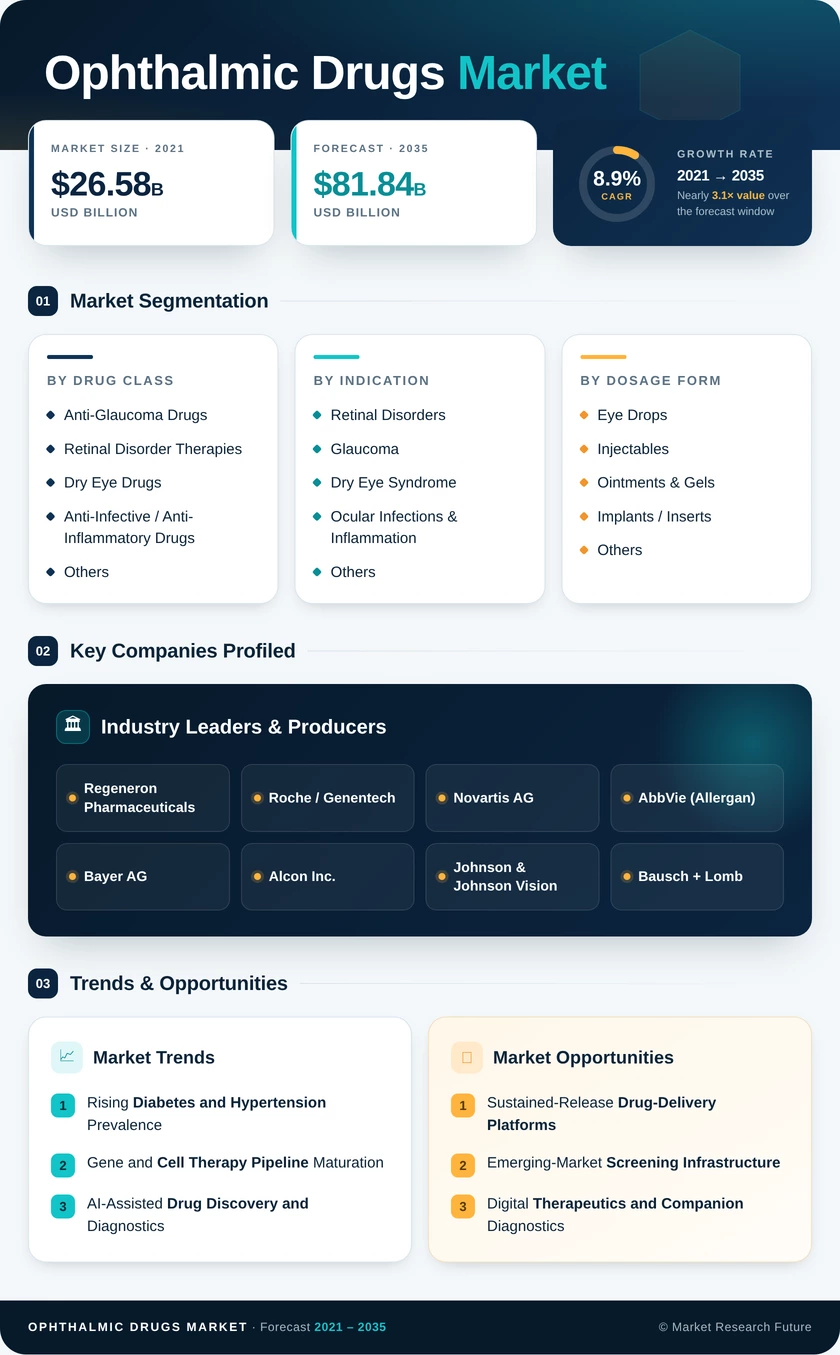

| Drug Class | Anti-Glaucoma Drugs, Retinal Disorder Therapies, Dry Eye Drugs, Anti-Infective / Anti-Inflammatory Drugs, Others | Anti-Glaucoma Drugs | Retinal Disorder Therapies |

| Indication | Retinal Disorders, Glaucoma, Dry Eye Syndrome, Ocular Infections & Inflammation, Others | Retinal Disorders | Ocular Infections & Inflammation |

| Dosage Form | Eye Drops, Injectables, Ointments & Gels, Implants / Inserts, Others | Eye Drops | Implants / Inserts |

| Product Type | Prescription Drugs, OTC Drugs | Prescription Drugs | OTC Drugs |

| Distribution Channel | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies | Hospital Pharmacies | Online Pharmacies |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Drug Class

| Sub-Segment | Key Trend |

| Anti-Glaucoma Drugs | Shift from beta-blockers to Rho-kinase inhibitors and fixed-combination therapies. |

| Retinal Disorder Therapies | Extended-interval anti-VEGF biologics and complement-pathway inhibitors are gaining traction. |

| Dry Eye Drugs | Biologic immunomodulators replacing legacy cyclosporine formulations. |

| Anti-Infective / Anti-Inflammatory Drugs | Corticosteroid-sparing NSAID combinations and antibiotic stewardship protocols |

| Others | Neuroprotective agents and mydriatic reformulations for diagnostic procedures |

Anti-glaucoma drugs continue to anchor the largest share of the ophthalmic therapeutics landscape, driven by the chronic, lifelong nature of intraocular-pressure management. Prostaglandin analogs remain the first-line standard, but newer mechanisms, including Rho-kinase inhibition and nitric-oxide donation, are capturing patients with inadequate monotherapy response, adding clinical and commercial complexity to formulary decisions.

By Indication

| Sub-Segment | Key Trend |

| Retinal Disorders | Anti-VEGF expanded indications and geographic atrophy complement inhibitors. |

| Glaucoma | Fixed-dose combinations and minimally invasive surgical adjuncts |

| Dry Eye Syndrome | Shift to anti-inflammatory biologics and neurostimulation devices. |

| Ocular Infections & Inflammation | Post-cataract prophylaxis volume growth and antibiotic stewardship |

| Others | Allergic conjunctivitis OTC growth and uveitis biologic pipeline |

Retinal disorders represent the highest-value indication, reflecting the premium pricing of intravitreal biologics and the expanding diabetic retinopathy patient pool linked to global metabolic-disease trends. Glaucoma remains the highest-volume indication, generating consistent prescription refills across decades of chronic management.

By Dosage Form

| Sub-Segment | Key Trend |

| Eye Drops | Preservative-free unit-dose systems replacing multi-dose bottles |

| Injectables | Pre-filled syringe formats improving clinic workflow efficiency |

| Ointments & Gels | Overnight sustained-release formulations for dry eye |

| Implants / Inserts | Bioerodible polymer platforms extending dosing intervals to six months |

| Others | Ocular sprays and dissolving films are entering niche segments |

Eye drops dominate by volume due to patient self-administration convenience and broad applicability across glaucoma, dry eye, allergy, and infection indications. Implants and inserts are the fastest-growing dosage form, reflecting strong clinical demand for reduced injection burden in retinal disease and growing regulatory acceptance of sustained-release drug-delivery devices.

By Product Type

| Sub-Segment | Key Trend |

| Prescription Drugs | Biologic share rising within the prescription tier |

| OTC Drugs | Consumer self-care for dry eye and allergy is driving pharmacy-channel growth |

Prescription drugs command the majority of market value, reflecting the specialist-driven nature of high-cost retinal and glaucoma therapies. The OTC segment is expanding at a faster pace as consumer awareness of digital eye strain increases and pharmacy retailers expand dedicated eye-care aisles.

By Distribution Channel

| Sub-Segment | Key Trend |

| Hospital Pharmacies | In-clinic biologics dispensing anchoring hospital share |

| Retail Pharmacies | Chronic-therapy refills and OTC shelf expansion |

| Online Pharmacies | Telehealth integration and auto-refill subscription models |

Hospital pharmacies maintain the largest distribution share because intravitreal injections and sustained-release implants are administered in clinical settings, requiring hospital-based dispensing. Online pharmacies represent the fastest-growing channel as telehealth prescriptions for chronic conditions like glaucoma and dry eye increasingly route through digital dispensing platforms with home-delivery logistics.