Edge Analytics Market Summary

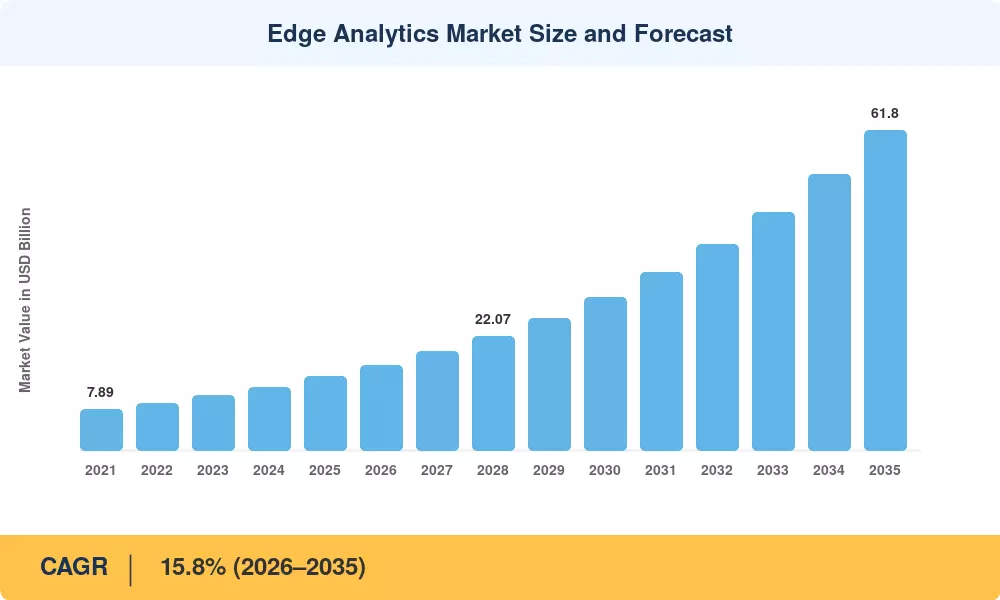

The Edge Analytics Market reached an estimated USD 14.2 billion in 2025 and is projected to grow from USD 16.4 billion in 2026 to USD 61.8 billion by 2035, registering a CAGR of 15.8% during the forecast period (2026–2035). Two catalysts anchor this trajectory: the explosion of IoT-connected devices — expected to surpass 30 billion globally by 2030 [2] — and enterprise mandates for real-time edge data processing solutions that eliminate cloud-round-trip latency. Governments across North America and Europe have earmarked over USD 12 billion in combined digital infrastructure spending through 2028, a significant portion targeting edge computing buildouts [3].

A fundamental technology shift is underway in the Edge Analytics Market. Legacy centralized data-warehouse architectures, which impose 100–500 ms round-trip delays, are giving way to IoT edge analytics software platforms capable of sub-10 ms inference at the device level. Semiconductor firms invested roughly USD 8.5 billion in purpose-built edge AI chipsets in 2024 alone [4]. NVIDIA's Jetson platform, Intel's OpenVINO toolkit, and Qualcomm's AI Engine have collectively re-priced what is possible for low-latency analytics at the network edge, making on-device intelligence accessible even for mid-market manufacturers.

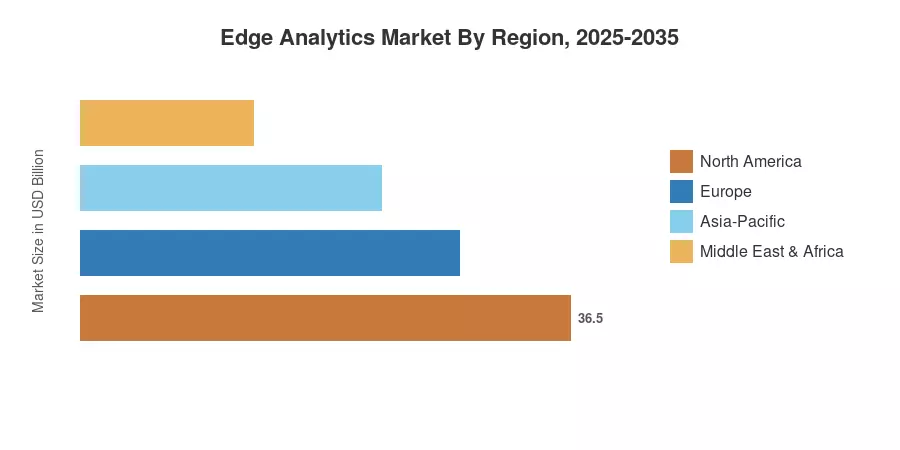

North America commands roughly 37% of the global Edge Analytics Market, driven by hyperscaler edge deployments and advanced 5G rollouts. Asia-Pacific is the fastest-growing region at an 18.4% CAGR, propelled by China's "East Data, West Computing" initiative and India's Smart Cities Mission [5]. Europe holds the second-largest share at approximately 27%, underpinned by the EU Data Act and industrial IoT modernization across Germany's Mittelstand. The decade ahead will reward vendors that can bridge cloud orchestration and edge autonomy into a single analytics fabric.

Key Report Takeaways

• By Component

- Software platforms — including streaming analytics engines and embedded ML runtimes — account for the largest revenue share at approximately 44% of the Edge Analytics Market in 2025

- Professional and managed services are expanding at a CAGR of 17.2%, as enterprises seek turnkey deployments of AI-powered edge analytics for smart devices

- Hardware components, particularly edge gateways and inference accelerators, contributed USD 4.1 billion in 2025

• By Application

- Manufacturing and industrial automation represent the dominant application, reflecting growing demand for edge computing analytics for manufacturing use cases such as predictive maintenance and quality inspection

- Smart cities and transportation hold a combined CAGR of 16.9%, fueled by intelligent traffic management and connected-infrastructure investments

- Retail and customer analytics are growing at 15.3% CAGR as in-store real-time personalization gains traction

• ByRegion

- North America leads the Edge Analytics Market with a 37% share, anchored by the United States' hyperscaler and telecom edge investments

- Asia-Pacific is forecast to reach USD 18.6 billion by 2035, the highest absolute growth of any region

- Europe contributes approximately 27% of global revenue, with Germany and the U.K. together accounting for over half of regional spend

MRFR's market sizing combines bottom-up vendor revenue analysis with top-down macro modeling. Primary data from 220+ enterprise interviews and 45 vendor briefings were triangulated against semiconductor shipment data, cloud-provider edge-node disclosures, and telecom capex filings. All historical figures are validated against publicly reported financials; forecast values apply the 15.8% compound growth rate with adjustments for cyclical investment patterns in the Edge Analytics Market.