Edible Flakes Market Summary

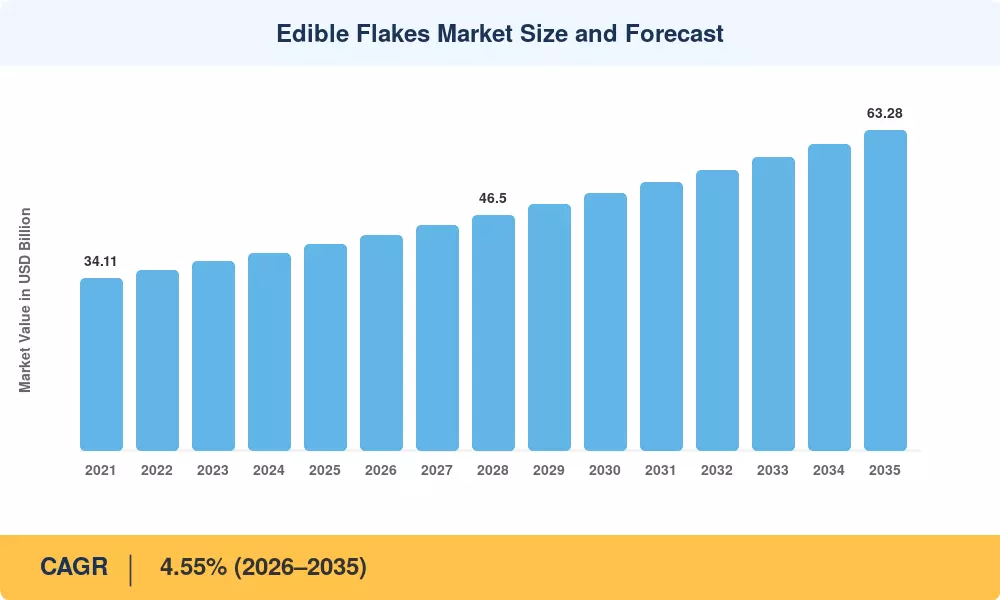

The edible flakes market stood at USD 40.75 billion in 2025 and is projected to reach USD 42.46 billion in 2026 before climbing to USD 63.28 billion by 2035, reflecting a CAGR of 4.55% across the forecast window. This expansion is anchored by rising global breakfast consumption rates and government-backed nutrition fortification programs—India's Food Safety and Standards Authority (FSSAI), for instance, mandated iron and folic acid fortification in staple cereals under its 2024 guidelines, channeling an estimated USD 320 million in compliance-related reformulation investments across the processed cereal sector [2]. Consumers in both mature and emerging economies are gravitating toward fortified breakfast cereal flakes and ready-to-eat cereal products that deliver convenience without sacrificing nutritional value.

A significant change is taking place in the product landscape. Ancient grains like quinoa and amaranth, as well as toasted grain flake products enhanced with plant protein and probiotics, are displacing traditional sugar-coated single-grain formulations. To demonstrate how seriously incumbents are taking the premiumization wave, General Mills alone pledged more than USD 180 million in 2024 to retool three North American production lines for flavored and multigrain flakes [3]. The volumetric core is still corn, oats, and wheat flakes, but innovation is obviously moving toward organic and functional sub-segments.

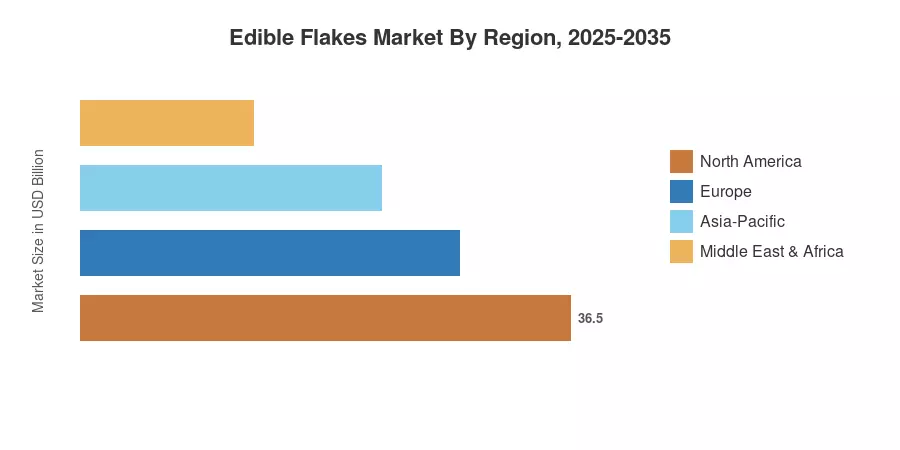

Due to ingrained breakfast traditions and private-label development across major retailers, North America maintained the highest share of the edible flakes market in 2025, with around 40.2%. With a predicted CAGR of 6.92%, Asia-Pacific is the fastest-growing area. This is due to the rising urbanization of China and India, where ready-to-eat cereal products are displacing traditional cooked breakfasts. With over 27% of the world's revenue, Europe is in second place. Intense competition is expected in the next 10 years as companies compete to attract health-conscious consumers at all price points

Key Report Takeaways

• By Product Type

- Corn flakes commanded 48.6% of the edible flakes market share in 2025, underscoring their dominance as the preferred base grain across both mature and developing economies

- Oat flakes are forecast to expand at a 5.42% CAGR through 2035, driven by consumer demand for heart-health-oriented fortified breakfast cereal flakes and beta-glucan-rich formulations

• By Nature

- Conventional variants accounted for USD 29.14 billion of the edible flakes market in 2025, though organic alternatives are gaining traction rapidly at a 6.67% CAGR

• By Format

- Ready-to-eat cold flakes held 68.5% share of format sales, while hot and instant flakes are projected to register a 5.91% CAGR as demand for toasted grain flake products in single-serve sachets grows

• By Regional

- North America retained a 40.2% share of the edible flakes market in 2025, led by the United States' USD 12.8 billion contribution

- Asia-Pacific is set to register the highest CAGR of 6.92% during 2026–2035, propelled by urbanization and rising disposable incomes favoring ready-to-eat cereal products

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s market sizing integrates bottom-up revenue modeling from manufacturer shipment data, retail panel audits, customs trade databases, and proprietary consumer surveys across 32 countries. Historical figures (2021–2024) rely on audited company filings; forecast projections (2026–2035) apply segment-weighted CAGR modeling validated against macroeconomic indicators.

.webp?v=1783425387)