Electric Traction Motor Market Summary

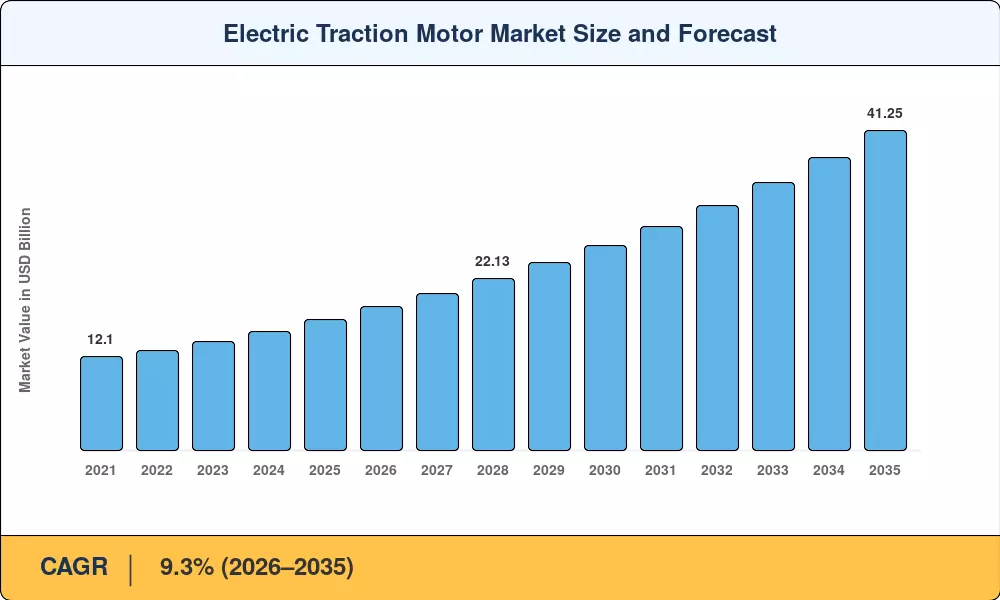

The Electric Traction Motor Market stood at USD 16.95 Billion in 2025 and is projected to reach USD 18.53 Billion by 2026, climbing to USD 41.25 Billion by 2035 at a compound annual growth rate of 9.3% during the forecast period (2026–2035). Government-backed rail modernization programs across India, China, and Southeast Asia have unlocked procurement pipelines worth tens of billions of dollars, while the transition to 800-volt battery architectures in passenger vehicles is pulling automakers toward higher-efficiency propulsion units [1]. These twin catalysts anchor a growth trajectory that outpaces broader industrial motor spending by a wide margin.

A technology shift is well underway. Legacy wound-rotor induction designs are giving way to advanced alternating-current configurations that deliver higher torque density per kilogram, cutting drivetrain weight while pushing peak efficiency above 96% [2]. The European Union's revised Energy Efficiency Directive (2023/1791) now mandates IE4-class minimum standards for new rolling stock traction chains, compelling operators to accelerate fleet renewal. Simultaneously, silicon-carbide power electronics are reshaping inverter-motor integration, enabling designers to shrink motor housings without sacrificing sustained output above 300 kilowatts [3].

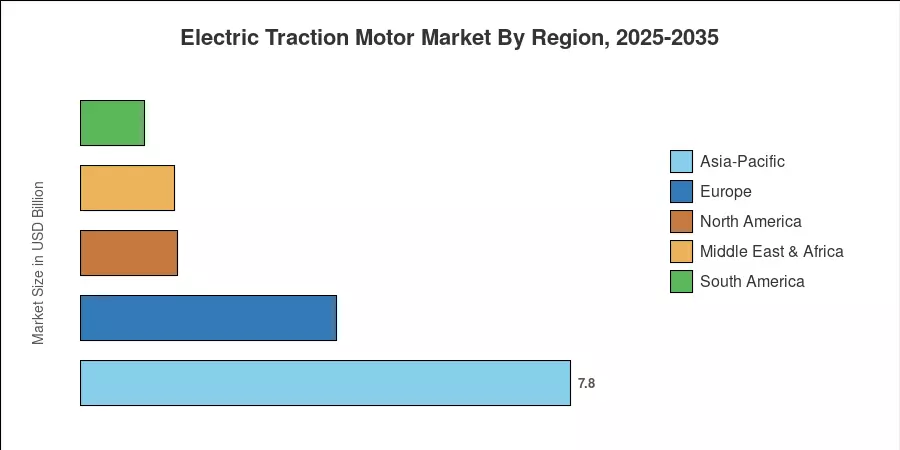

Asia-Pacific commands roughly 46% of the Electric Traction Motor Market, underpinned by China's 14th Five-Year Plan rail investments and India's National Rail Plan targeting full electrification by 2030 [4]. The region also posts the fastest growth at an estimated 10.6% CAGR through 2035. Europe follows as the second-largest region at approximately 24% share, driven by stringent emissions mandates and cross-border high-speed rail corridors. North America accounts for about 18% of global demand, with fresh momentum from the Bipartisan Infrastructure Law's USD 66 Billion passenger rail allocation [5]. As electrified transport scales, the Electric Traction Motor Market is positioned to benefit from converging policy, technology, and capital flows across every major geography.

Key Report Takeaways

By Type

- Alternating-current motors captured approximately 61% of the Electric Traction Motor Market revenue in 2025, reflecting their dominance across rail and automotive platforms.

- Direct-current motors continue to serve legacy metro and mining applications, contributing the remaining share.

By Application

- Railways accounted for a 43% share of the Electric Traction Motor Market in 2025, supported by multi-billion-dollar procurement cycles in Asia and Europe.

- Electric vehicle applications are advancing at a projected 17.0% CAGR through 2035, the fastest among all application segments.

By Geography

- Asia-Pacific leads with 46% of the Electric Traction Motor Market and is forecast to grow at a 10.6% CAGR.

- Europe holds approximately 24% share, while North America contributes about 18%.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model blends bottom-up revenue estimation from component-level shipment tracking with top-down validation against national rail procurement budgets, automotive OEM production plans, and published financial disclosures from the ten largest traction motor suppliers globally. Historical data draws on customs trade databases and verified manufacturer filings; forecast projections apply segment-specific growth curves anchored to policy-driven demand signals.