Electric Vehicle Motor Controller Market Summary

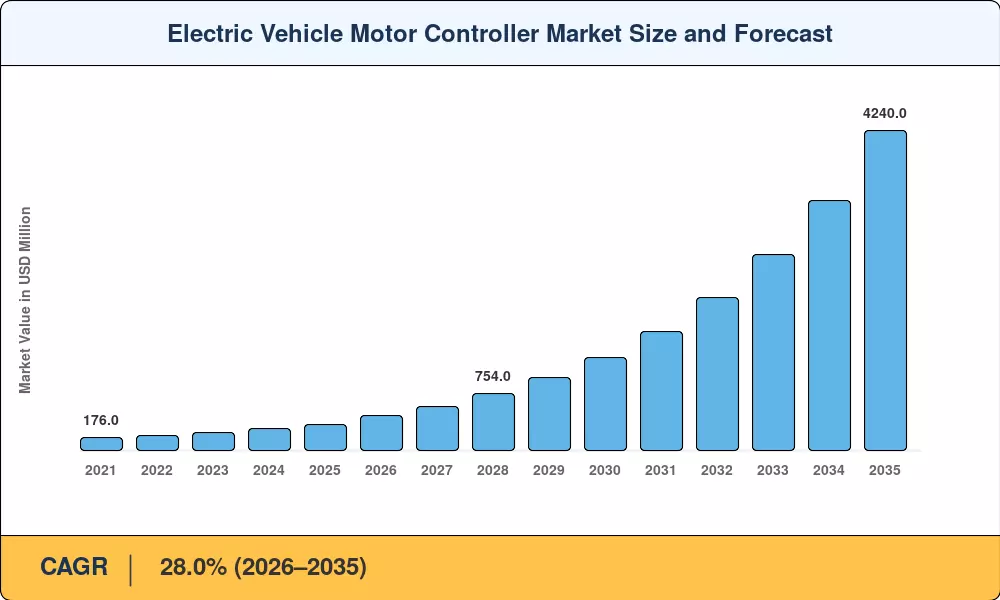

The electric vehicle motor controller market reached an estimated USD 350 Million in 2025 and is projected to grow from USD 460 Million in 2026 to USD 4,240 Million by 2035, registering a compound annual growth rate of 28.0% during the forecast period. Two forces are accelerating demand: governments worldwide have committed over USD 125 billion in combined EV subsidies and charging-infrastructure grants through 2030 [1], while automakers face binding CO₂ fleet-average mandates — the EU's 2035 combustion ban and China's NEV credit system chief among them [2]. These policy triggers translate directly into higher unit volumes of traction inverters and the controllers that manage them.

A technology shift underpins the electric vehicle motor controller market expansion. Legacy low-voltage controller platforms designed for 400 V powertrains are giving way to 800 V-capable architectures built around silicon-carbide (SiC) power modules. The U.S. Department of Energy's Vehicle Technologies Office allocated USD 535 million in 2024 to wide-bandgap semiconductor R&D aimed at pushing inverter power density beyond 100 kW/L [3]. Simultaneously, automakers are migrating from domain-based electrical/electronic (E/E) layouts to zonal architectures, which consolidate motor-control, battery-management, and thermal-management functions into fewer high-compute controllers running safety-critical software stacks.

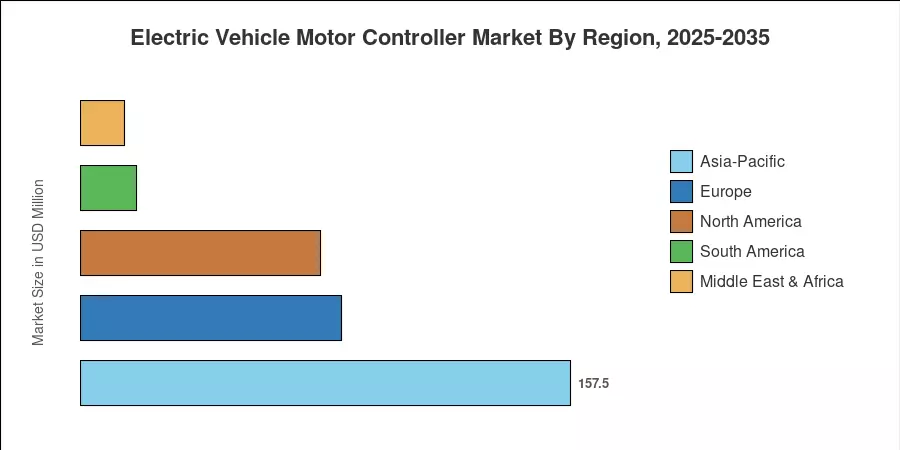

Asia-Pacific commands roughly 45% of the electric vehicle motor controller market, driven by China's dominance in both EV production and semiconductor packaging. Europe holds approximately 24% share, buoyed by stringent Euro 7 standards and OEM investment in next-generation drivetrains. North America accounts for about 22%, with growth anchored in IRA-funded domestic battery and power-electronics manufacturing. As EV penetration crosses 25% of global new-car sales, the electric vehicle motor controller market is poised to transition from a component supplier niche into a platform-level design battleground.

Key Report Takeaways

• By Motor Type

- AC Induction motors represented the largest segment of the electric vehicle motor controller market in 2025, with approximately 65% share, favored for cost-effective designs in high-volume passenger platforms.

- Brushless DC motors are forecast to post the fastest growth at roughly 31.0% CAGR through 2035, propelled by their superior torque density in light commercial applications.

• By Communication Protocol

- CAN 2.0 accounted for USD 202 Million in the electric vehicle motor controller market in 2025, reflecting its entrenched position across legacy platforms.

- Automotive Ethernet is projected to expand at approximately 29.0% CAGR as OEMs adopt bandwidth-intensive over-the-air updating and autonomous-driving data architectures.

• By Vehicle Type

- Passenger cars held roughly 65% of the electric vehicle motor controller market in 2025.

- Medium and heavy commercial vehicles are set to grow at the fastest pace through 2035 at approximately 30.2% CAGR, accelerated by zero-emission freight mandates.

• By Propulsion Type

- Battery Electric Vehicles captured about 67% of the electric vehicle motor controller market in 2025.

- Fuel-Cell Electric Vehicles are anticipated to register the highest CAGR of roughly 28.2% through 2035.

• By Region

- Asia-Pacific captured approximately 45% share of the electric vehicle motor controller market in 2025 and remains the fastest-growing region at around 31.2% CAGR.

- Europe accounted for about USD 84 Million in 2025, supported by regulatory mandates and OEM R&D concentration.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary OEM interviews, Tier-1 supplier revenue disclosures, government subsidy disbursement data, and proprietary demand-modeling across 32 country-level vehicle-production forecasts.

.webp?v=1784802914)