EV Power Inverter Market Summary

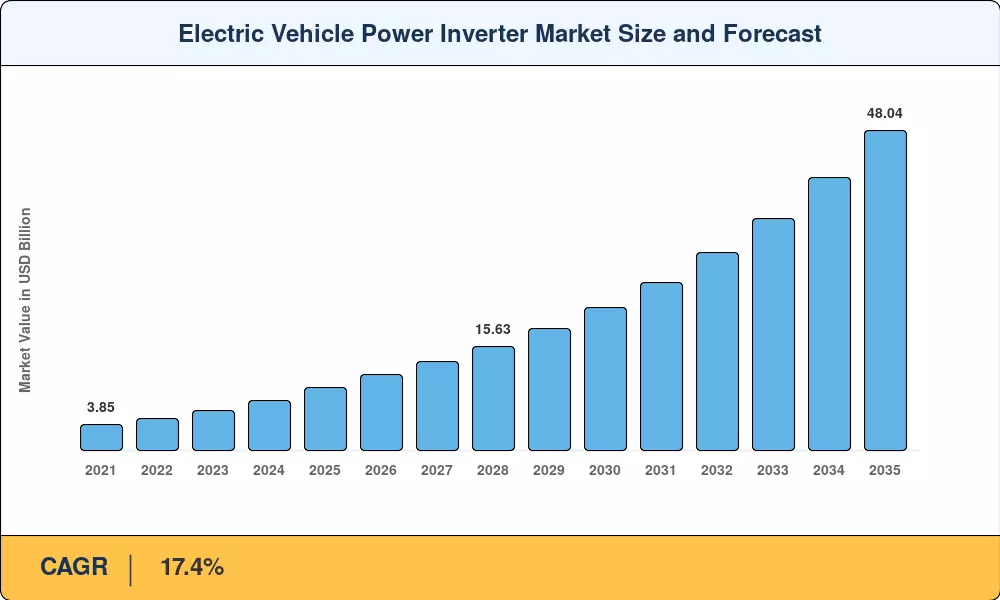

The electric vehicle power inverter market reached USD 9.53 billion in 2025 and is projected to grow from USD 11.34 billion in 2026 to USD 48.04 billion by 2035, registering a CAGR of 17.4% across the forecast period. This expansion is anchored to two catalysts that have moved from policy debate to concrete spending: the European Union's 2035 ban on new internal-combustion passenger vehicles and China's dual-credit policy, which now penalizes automakers whose new-energy vehicle mix falls below 28% of annual production. Together, these mandates guarantee baseline demand for power electronics in every major auto-producing economy [1][2].

The technology story driving the electric vehicle power inverter market centers on a generational shift in semiconductor architecture. Silicon insulated-gate bipolar transistors, the workhorse of early EV inverters, are steadily ceding ground to wide-bandgap devices that cut switching losses by up to 50% and enable higher-frequency operation in compact housings. Wolfspeed's USD 5 billion Mohawk Valley fab and Infineon's planned EUR 5 billion expansion in Dresden reflect the capital being committed to this transition [3][4].

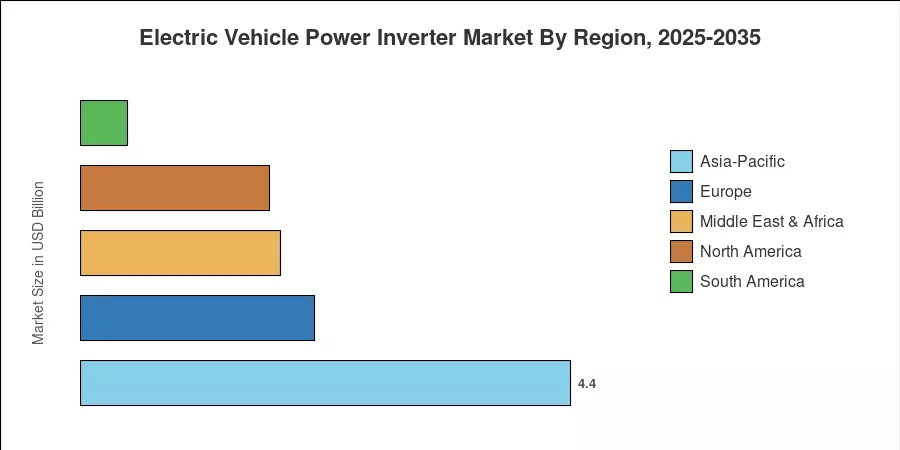

Asia-Pacific commands roughly 46% of the electric vehicle power inverter market, led by China's unmatched battery-electric production volumes and Japan's dominance in power-module packaging. North America holds an estimated 24% share, buoyed by the Inflation Reduction Act incentives for domestically manufactured drivetrain components. Europe, at about 22%, remains the regulatory pace-setter, and its Fit-for-55 framework keeps OEM procurement cycles tilted toward next-generation inverters through the decade's end [5][6].

Key Report Takeaways

• By Propulsion Type

- Battery-electric vehicles accounted for approximately 57.9% of the electric vehicle power inverter market in 2025, reflecting their dominance across passenger and light-commercial platforms.

- Fuel-cell electric vehicles are forecast to post the fastest CAGR of 20.9% through 2035, driven by heavy-truck hydrogen programs in Europe and South Korea.

• By Vehicle Type

- Passenger cars led the electric vehicle power inverter market with a 67.7% share in 2025, as consumer BEV adoption outpaces commercial segments.

- Heavy commercial vehicles and buses are projected to register a 20.8% CAGR to 2035, supported by urban zero-emission zones.

• By Region

- Asia-Pacific generated the largest revenue share in the electric vehicle power inverter market, underpinned by Chinese OEM scale and Japanese supplier technology.

- North America's electric vehicle power inverter market is expanding at a 17.8% CAGR, with IRA-linked domestic manufacturing incentives accelerating capacity build-outs.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down policy-driven demand models with bottom-up OEM production forecasts and Tier-1 supplier revenue disclosures. Historical data are calibrated against public filings, while forecast-period figures reflect announced capacity expansions, regulatory phase-in schedules, and semiconductor supply roadmaps.