Electric Vehicle Range Extender Market Summary

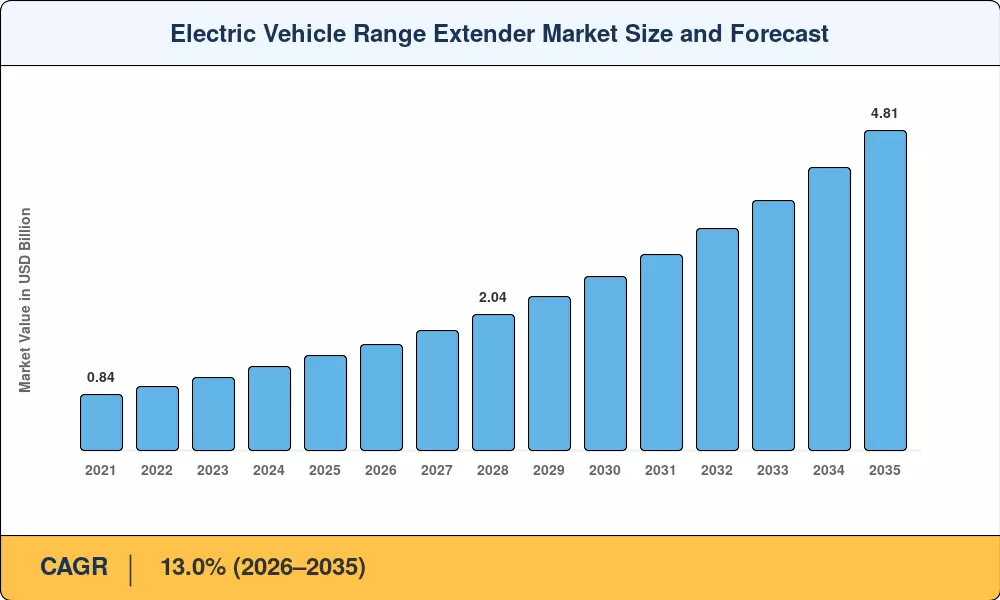

The electric vehicle range extender market reached USD 1.43 billion in 2025 and is projected to grow from USD 1.60 billion in 2026 to USD 4.81 billion by 2035, registering a 13.0% CAGR during the forecast period. This expansion is anchored in two converging forces: tightening fleet CO₂ limits across the EU and China's aggressive subsidies for extended-range electric vehicles (EREVs) [1]. With more than 40 countries committing to zero-emission vehicle sales mandates by 2035, OEMs are turning to onboard auxiliary power units as a cost-effective bridge between legacy combustion drivetrains and pure battery-electric platforms [2].

Battery pack costs declined to roughly USD 139 per kWh in 2024, tracking toward USD 113 per kWh in 2025, which reshapes the economics of hybrid architectures [3]. Pairing a smaller, lighter battery with a compact range-extending generator allows automakers to cut vehicle curb weight by 15–20% compared with a full-size BEV battery, trimming both material costs and energy consumption per kilometer. This engineering trade-off has reignited interest from European premium brands and Chinese mass-market OEMs alike.

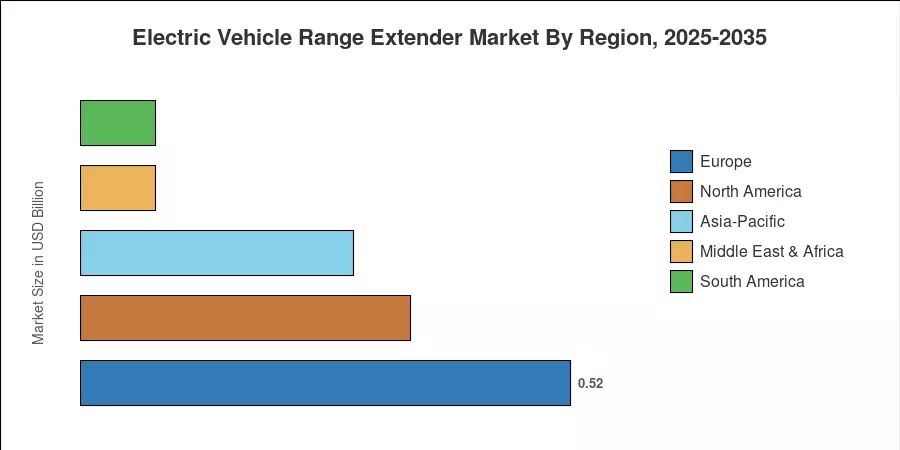

Europe commands a 36.3% revenue share of the electric vehicle range extender market, supported by strict Euro 7 emission norms and clean-air zone enforcement in major cities. Asia-Pacific is the fastest-growing region at a 20.4% CAGR, propelled by China's booming EREV SUV segment and expanding domestic component supply chains. North America holds the second-largest share as U.S. fleet operators evaluate range extenders for medium-duty logistics. The decade ahead will reward suppliers who can deliver modular, multi-fuel generator platforms adaptable to hydrogen and synthetic fuels.

Key Report Takeaways

• By Technology

- ICE-based range extenders captured 71.2% of the electric vehicle range extender market in 2025, reflecting mature engine supply chains and lower per-unit costs.

- Fuel cell range extender variants are forecast to expand at a 23.8% CAGR through 2035, driven by hydrogen corridor buildouts in Europe and South Korea.

• By Component

- Battery packs accounted for 46.1% of component-level value in 2025, underscoring the battery's dual role as primary energy store and buffer for regenerative braking energy.

• By Vehicle Class

- Battery packs accounted for 46.1% of component-level value in 2025, underscoring the battery's dual role as primary energy store and buffer for regenerative braking energy.

- Heavy commercial vehicles are poised to grow at a 22.1% CAGR through 2035 as mining and defense fleets adopt range-extended electric platforms.

• By Region

- Europe generated 36.3% of the electric vehicle range extender market revenue in 2025, led by Germany, France, and the Nordic countries.

- Asia-Pacific is forecast to register a 20.4% CAGR, with China alone accounting for over half of regional unit shipments.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up component shipment analysis with top-down OEM production data, cross-validated against customs trade records, patent filings, and investor disclosures from public-market participants in the electric vehicle range extender market.