Electron Microscope Market Summary

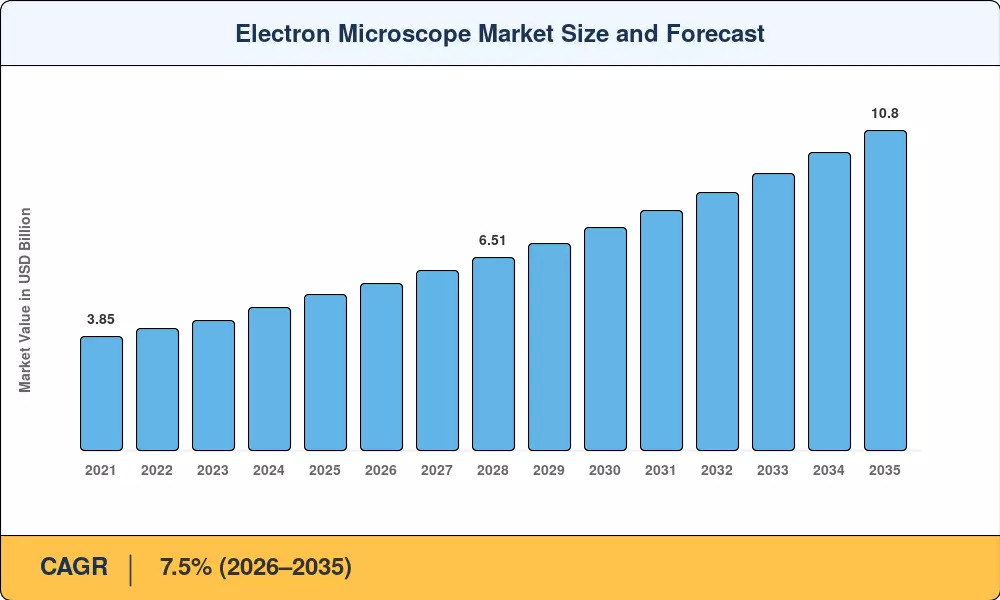

The Global Electron Microscope Market size was valued at USD 5.25 Billion in 2025, and the market is projected to grow from USD 5.64 Billion in 2026 to USD 10.80 Billion by 2035, registering a CAGR of 7.5% during the forecast period 2026–2035. Two forces are pulling this expansion forward: the global semiconductor industry's push toward sub-3nm gate-all-around transistor architectures — catalyzed by the USD 52.7 Billion CHIPS and Science Act in the United States [1] — and a parallel surge in cryo-electron microscopy installations across government-funded life-science campuses. The Electron Microscope Market sits at the intersection of advanced manufacturing and fundamental research, making it uniquely resistant to single-sector downturns.

A technology overhaul is redefining how laboratories and fabs acquire electron microscopy platforms. Legacy thermionic-source instruments are steadily giving way to cold field-emission and Schottky emitter systems capable of sub-angstrom resolution, while artificial-intelligence-driven automation now condenses cryo-EM data-collection runs from multi-day campaigns to overnight sessions. The European Commission committed EUR 13.5 Billion to its Chips Act implementation, and a meaningful share of that funding targets advanced metrology infrastructure, including transmission electron microscopy capabilities at pilot lines in Dresden and Leuven [2].

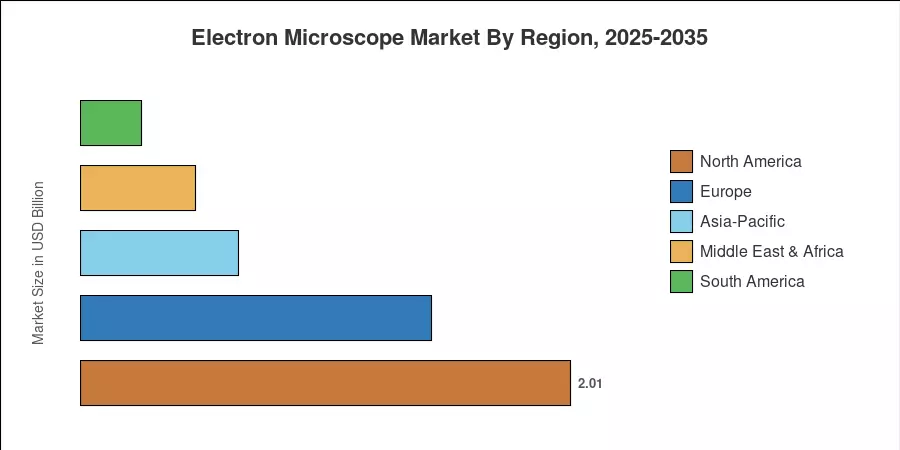

North America accounted for 38.2% of the Electron Microscope Market in 2025, anchored by semiconductor fabrication expansion in Arizona, Texas, and Ohio. Asia-Pacific stands as the fastest-growing region at a projected 12.4% CAGR through 2035, led by national electron-optics capacity programs in China and India. Europe holds the second-largest share at 27.5%, driven by automotive semiconductor demand and academic instrumentation renewal cycles. As national security concerns increasingly shape technology procurement, the Electron Microscope Market is poised for sustained geographic diversification through the decade.

Key Report Takeaways

• By Instrument Type

- SEM platforms commanded a 72.5% share of the Electron Microscope Market in 2025, reflecting their dominance in high-throughput wafer inspection and routine biological screening workflows.

- TEM instruments are forecast to grow at a 12.7% CAGR through 2035 as atomic-resolution defect localization becomes non-negotiable for advanced-node chip manufacturing.

- Dual-beam FIB-SEM systems generated USD 0.38 Billion in 2025 revenue, driven by advanced packaging and failure-analysis demand.

• By Application

- Life sciences and biology represented 22.8% of the Electron Microscope Market in 2025, with structural biology and vaccine research powering instrument procurement.

- Nanotechnology applications are projected to expand at a 10.1% CAGR, fueled by nanoparticle characterization mandates in pharmaceuticals and energy storage.

• By Region

- North America captured 38.2% of global spending in 2025, with the U.S. accounting for over three-quarters of regional revenue.

- Asia-Pacific is forecast to grow at a 12.4% CAGR through 2035 as China and India invest in domestic electron-optics manufacturing.

Market Size and Forecast (2021–2035)

Market Research Future estimates are derived from a combination of bottom-up revenue modeling across instrument OEMs, top-down calibration using national science-funding databases, and triangulation with trade-flow data from customs authorities in major importing nations. Historical figures reflect actual shipment revenues; forecast values incorporate contracted pipeline visibility from leading manufacturers and announced government funding commitments.