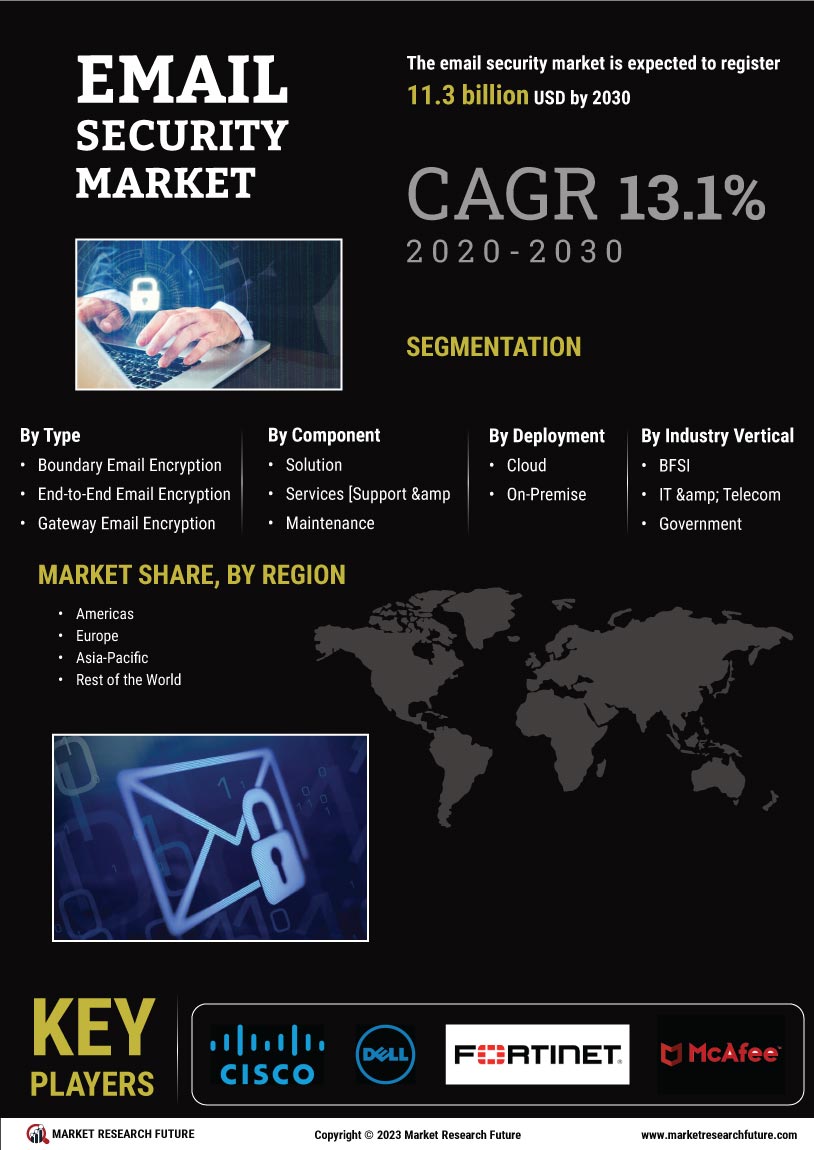

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Component | Solutions, Services | Solutions | Services |

| By Deployment Mode | Cloud, On-Premises | Cloud | Cloud |

| By Enterprise Size | Large Enterprises, SMEs | Large Enterprises | SMEs |

| By Security Type | Secure Email Gateways, Integrated Cloud Email Security, Email Encryption & Other | Secure Email Gateways | Integrated Cloud Email Security |

| By End-User Industry | BFSI, Email Security Market, IT and Telecom, Government and Defense, Retail and E-Commerce, Manufacturing, Energy and Utilities, Other | BFSI | Email Security Market |

| By Region | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Component

| Sub-Segment | Key Trend |

| Solutions | Core detection platform licensing remains the dominant revenue line |

| Services | Outsourced SOC and managed-detection demand growing fastest |

Solutions dominate the revenue base, but the services line is where net-new growth is concentrating as mid-market buyers increasingly outsource operations rather than staff in-house teams.

By Deployment Mode

| Sub-Segment | Key Trend |

| Cloud | The majority of new bookings are tied to workspace migration |

| On-Premises | Sustained by regulated industry data-residency needs |

Cloud has crossed the majority threshold of new deployments, though on-premises retains a durable base in banking and government, where data-residency rules apply.

By Enterprise Size

| Sub-Segment | Key Trend |

| Large Enterprises | Compliance-driven, multi-year platform contracts |

| SMEs | Fastest-growing, cloud-delivered, affordable entry points |

SMEs are the structural growth story of this segmentation dimension, closing the adoption gap as cloud delivery removes the infrastructure cost barrier that historically excluded them.

By Security Type

| Sub-Segment | Key Trend |

| Secure Email Gateways | Legacy install-base renewal, slower growth |

| Integrated Cloud Email Security | API-native, fastest-growing sub-segment |

| Email Encryption & Other | Compliance-driven, steady demand |

Integrated Cloud Email Security is where nearly all net-new enterprise spend is landing, reflecting the broader shift from perimeter-based to API-native inspection architectures.

By End-User Industry

| Sub-Segment | Key Trend |

| BFSI | Largest vertical, audit-driven procurement |

| Email Security Market | Fastest-growing, ransomware and PHI exposure |

| IT and Telecom | Client-mandated certification requirements |

| Government and Defense | National cybersecurity mandate compliance |

| Retail and E-Commerce | Payment data protection focus |

| Manufacturing | OT/IT convergence risk driving new spend. |

| Energy and Utilities | Critical-infrastructure protection mandates |

Email Security Market's rapid growth reflects tightening breach-notification timelines that turn detection speed into a direct compliance requirement rather than a discretionary security upgrade.

By Region

| Sub-Segment | Key Trend |

| North America | Dominant, compliance-driven platform consolidation |

| Europe | NIS2-driven procurement acceleration |

| Asia-Pacific | Fastest-growing, SME and digitization-led adoption |

| South America | LGPD-driven enterprise adoption in Brazil |

| Middle East & Africa | Government digital-transformation programs leading growth |

North America's regulatory density keeps it dominant, while Asia-Pacific's combination of first-time SME buyers and national digitization programs makes it the clearest growth engine over the 2026–2035 window.