Email Security Market Summary

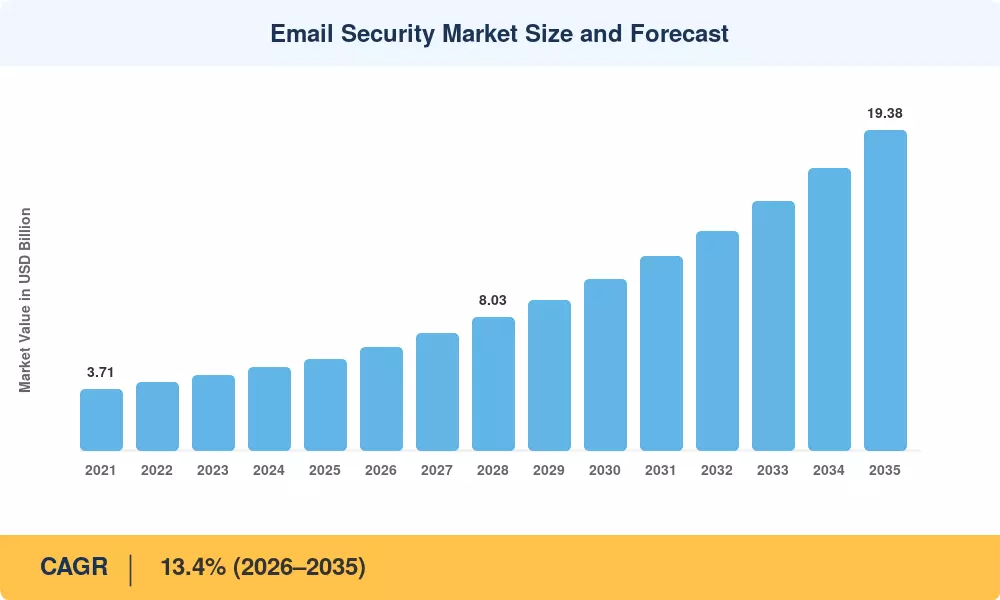

The Email Security Market stood at USD 5.54 billion in 2025 and is set to open the forecast window at roughly USD 6.24 billion in 2026, climbing to USD 19.38 billion by 2035 at a 13.4% CAGR. That trajectory owes a lot to the EU's NIS2 Directive, which pulled thousands of mid-sized firms into mandatory incident-reporting regimes overnight. Boards that once treated email filtering as a checkbox now fund it as a board-level risk line item.

Cloud-native platforms coupled with APIs are replacing legacy secure email gateways developed for on-premises exchange servers, inspecting messages inside Microsoft 365 and Google Workspace instead of the network perimeter. Vendors have put a lot of money into this change, with Cisco’s $28 billion acquisition of Splunk in 2023 specifically positioned around the idea of merging email, endpoint and SIEM telemetry into a single detection fabric. Buyers are rewarding that consolidation by signing longer contracts.

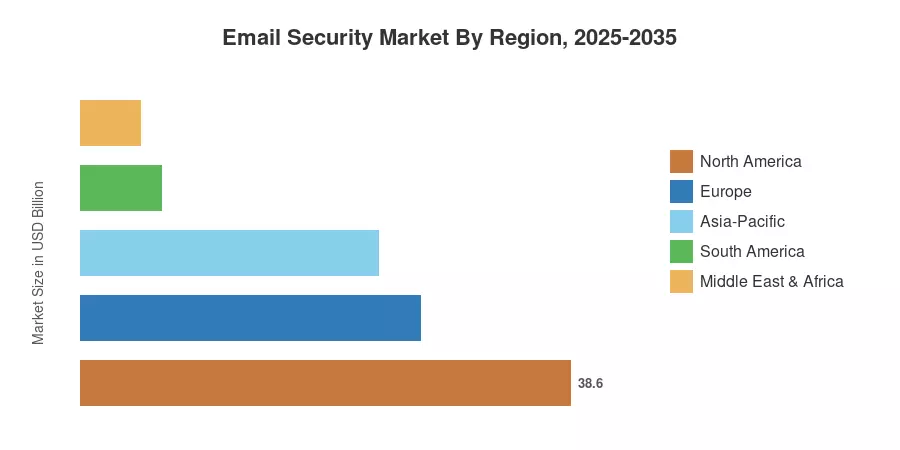

North America continues to lead, accounting for around 38.6% of 2025 revenue, driven by extensive regulatory duties in financial services and healthcare. Asia-Pacific is the fastest growing market with digitization plans in India, China and Southeast Asia driving first-time purchasers to cloud email security. Europe is the second largest, with the push for NIS2 compliance dates. In the coming decade, manufacturers that can integrate detection and response will be differentiated from vendors that still provide single filters.

Key Report Takeaways

• By Technology

- Solutions (as opposed to services) held roughly 65.2% share of the Email Security Market in 2025

- Integrated Cloud Email Security (ICES) is expanding at a 22.5% CAGR, the fastest of any security-type segment.

- Cloud deployment accounted for about 55.0% of the Email Security Market in 2025

• By Ens-Use

- BFSI held roughly 25.4% share of end-user revenue in 2025

- Healthcare is the fastest-growing vertical at an 18.1% CAGR through 2035

- Large enterprises captured about 64.2% share, though SMEs are closing the gap

• By Region

- North America led the Email Security Market with roughly 38.6% revenue share in 2025

- Asia-Pacific is projected to post a 15.4% CAGR through 2035

- Europe holds the second-largest regional position, driven by regulatory mandates

Market Size and Forecast (2021–2035)

Figures below are calibrated from historical vendor disclosures and public market-sizing benchmarks, then projected forward using a consistent compound growth methodology.