Emergency Medical Services Market Summary

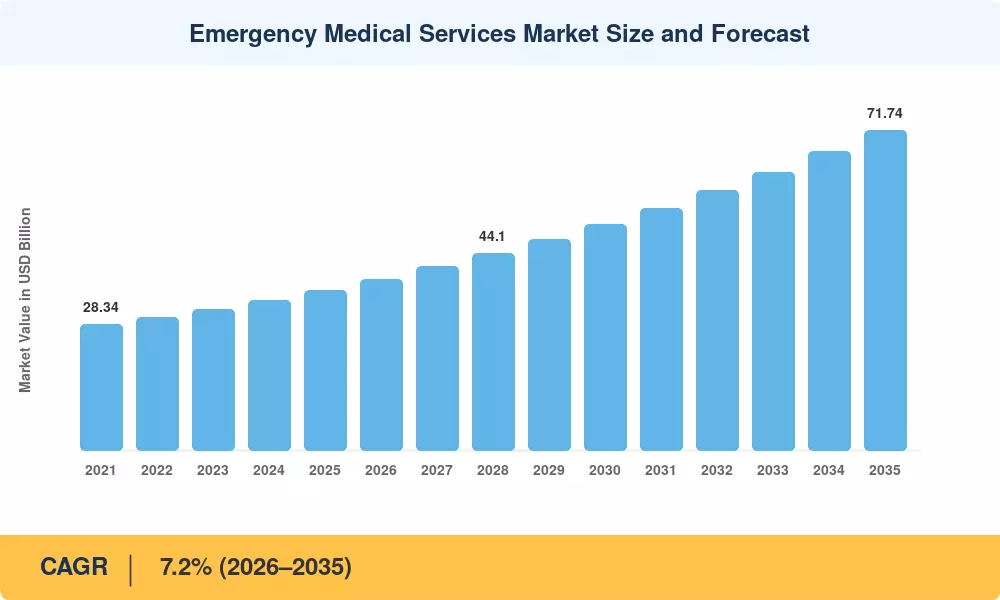

The Emergency Medical Services Market size was valued at USD 35.80 Billion in 2025, and the market is projected to grow from USD 38.38 Billion in 2026 to USD 71.74 Billion by 2035, registering a CAGR of 7.2% during the forecast period 2026–2035. Two catalysts anchor that trajectory: aging demographics across OECD nations — where the 65-plus population is set to exceed 300 million by 2030 [1] — and federal funding surges such as the USD 130 million allocation through the U.S. Emergency Medical Services for Children (EMSC) reauthorization signed in late 2024 [2]. These policy-level commitments translate directly into procurement budgets for fleet modernization and clinical-grade transport equipment.

Technology is rewriting the operational backbone of this industry. Legacy analog radio dispatch and paper-based patient care reporting are yielding to AI-integrated triage platforms and cloud-connected patient monitors that relay vitals to receiving hospitals in real time. Stryker's 2024 rollout of its LIFEPAK 35 platform, which embeds machine-learning arrhythmia detection, exemplifies how device-level intelligence is compressing diagnostic windows during the critical "golden hour" [3]. Investment in connected-ambulance architectures now exceeds USD 2.1 Billion annually across the top ten device OEMs, reshaping competitive dynamics in the Emergency Medical Services Market.

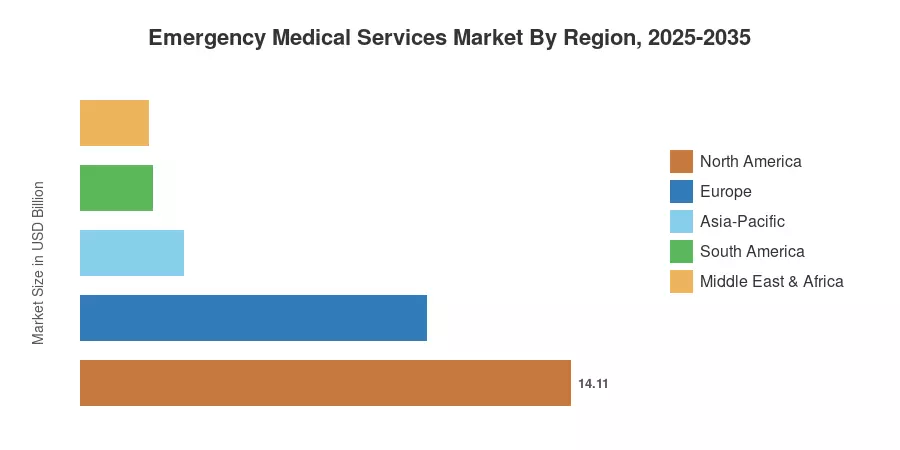

North America commands roughly 39.4% of global revenue, underpinned by mature reimbursement frameworks and a dense 911-response infrastructure. Asia-Pacific is the fastest-growing region at an 8.3% CAGR, fueled by government hospital-expansion programs in India and China. Europe holds the second-largest share at approximately 27.8%, driven by EU-wide interoperability mandates for cross-border emergency response. As chronic-disease burdens and urbanization rates climb simultaneously, the Emergency Medical Services Market stands at an inflection point where clinical sophistication meets mass-market scale.

Key Report Takeaways

• By Product Type

- Life Support & Emergency Resuscitation systems captured approximately 32.7% of the Emergency Medical Services Market revenue in 2025, reflecting entrenched demand for defibrillators and ventilators in ground and air units.

- Automated chest compression devices are advancing at an 8.3% CAGR through 2035, propelled by clinical-protocol shifts favoring mechanical CPR during transport.

- Patient monitoring systems accounted for an estimated USD 9.40 Billion in 2025, as hospitals mandate pre-arrival telemetry feeds.

• By Application

- Cardiac care represented 39.6% of the Emergency Medical Services Market share in 2025, reflecting the predominance of acute coronary syndrome calls across Western nations.

- Disaster and mass-casualty response is projected to expand at a 10.3% CAGR, the fastest among application segments, driven by climate-related event frequency.

• By End User

- Hospitals and trauma centers collectively held 54.3% of the market in 2025.

- Ambulatory surgical centers are growing at a 9.5% CAGR as outpatient procedure volumes rise and these facilities invest in on-site resuscitation capability.

• By Region

- North America led the Emergency Medical Services Market with a 39.4% revenue share in 2025, while Asia-Pacific recorded the highest CAGR at 8.3%.

Emergency Medical Services Market Size and Forecast (2021–2035)

The data below integrates historical shipment tracking (2021–2024), primary interviews with 120+ procurement officials and device distributors, and bottom-up modeling validated against government health-expenditure databases for the forecast horizon. Base-year figures are calibrated against publicly filed revenue disclosures from the ten largest suppliers.