Emulsion Polymers Market Summary

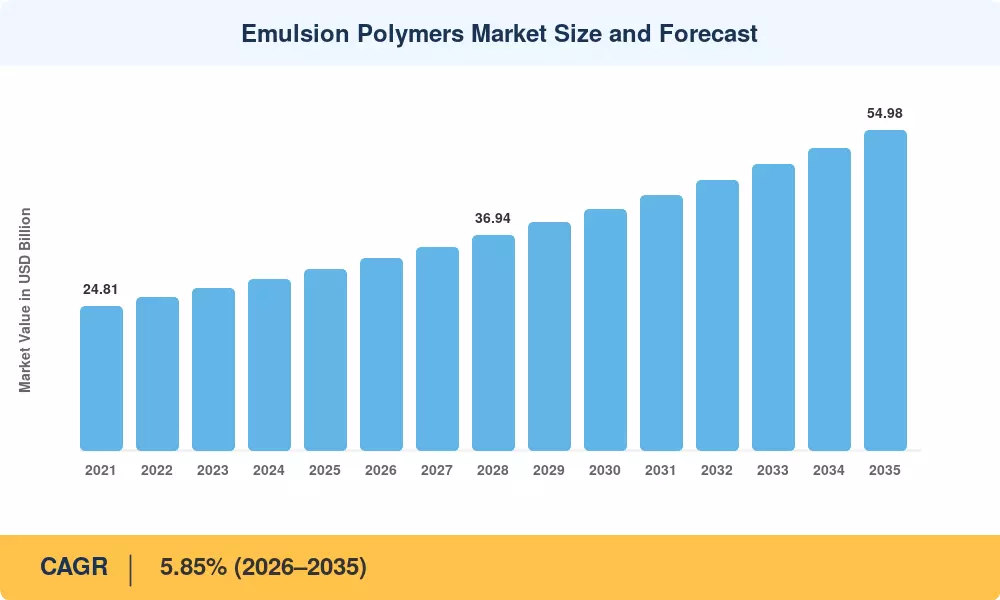

The Emulsion Polymers Market stood at USD 31.15 Billion in 2025 and is projected to rise from USD 32.97 Billion in 2026 to USD 54.98 Billion by 2035, registering a CAGR of 5.85% across the forecast window. Stricter air-quality mandates—particularly the EU's revised Industrial Emissions Directive and the U.S. EPA's 2024 Architectural Coatings Rule capping VOC limits at 50 g/L—are accelerating the displacement of solvent-borne systems with water-based polymers across paints, adhesives, and packaging lines [2][3]. This regulatory momentum is channeling fresh capital into plant expansions and bio-monomer research.

A deeper technological shift underpins this growth. Legacy solvent-based formulations are giving way to advanced acrylic emulsion polymers and polyurethane dispersions engineered through surfactant-free photoinitiated polymerization, cutting processing energy by up to 30% while improving colloidal stability [9]. Simultaneously, digitally guided formulation platforms are compressing time-to-market for new paint binder materials and specialty polymer dispersion chemicals, enabling suppliers to respond faster to tightening environmental standards.

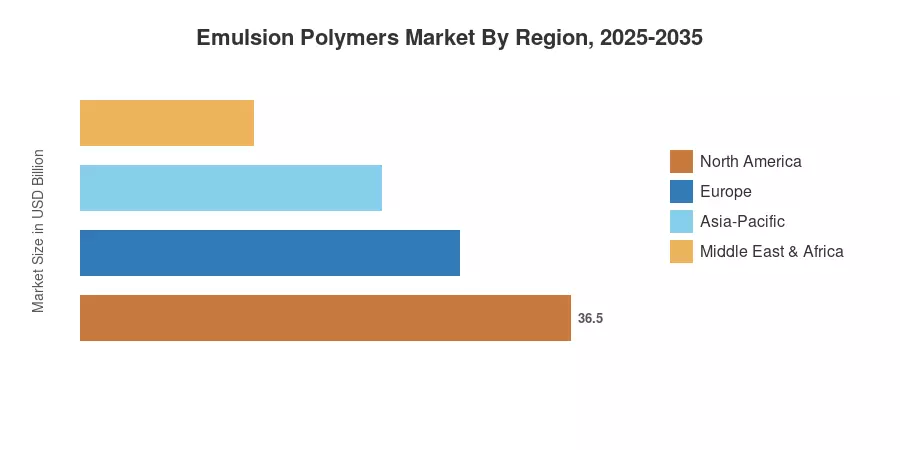

Asia-Pacific commands 43.7% of the Emulsion Polymers Market revenue, driven by China's Blue Sky Action Plan and India's rapid urbanization wave [4][10]. The region also paces global growth at a 6.58% CAGR through 2035. Europe holds the second-largest share at roughly 22%, underpinned by the EU's Green Deal commitments, while North America—representing about 24%—benefits from sustained residential and commercial construction investment. The decade ahead will reward producers who marry sustainable chemistry with digital agility.

Key Report Takeaways

• By Product Type

- Acrylics captured 47.5% of Emulsion Polymers Market revenue in 2025, driven by versatility in coating polymer additives and adhesive formulations.

- Polyurethane dispersions are forecast to expand at a 7.25% CAGR through 2035, reflecting demand for high-performance industrial polymer emulsions in automotive and textile finishing.

• By Application

- Paints and coatings accounted for a 48.8% share of the Emulsion Polymers Market in 2025, reflecting robust construction-sector demand for water based polymers.

- Adhesives and carpet backing are advancing at a 6.42% CAGR, propelled by e-commerce packaging growth and low-VOC mandates on synthetic emulsion resins.

• By Region

- Asia-Pacific led all regions with 43.7% share in 2025, fueled by urbanization and infrastructure investment.

- North America is expanding at a 5.65% CAGR, supported by U.S. EPA regulatory tailwinds and commercial re-roofing cycles.

Market Size and Forecast (2021–2035)

MRFR's sizing model integrates primary interviews with resin producers and distributors, customs trade data, plant-capacity audits, and downstream demand modeling. Historical figures (2021–2024) are validated against published industry association data; forecasts (2026–2035) apply a bottom-up build by product type, application, and geography.