Encryption Software Market Summary

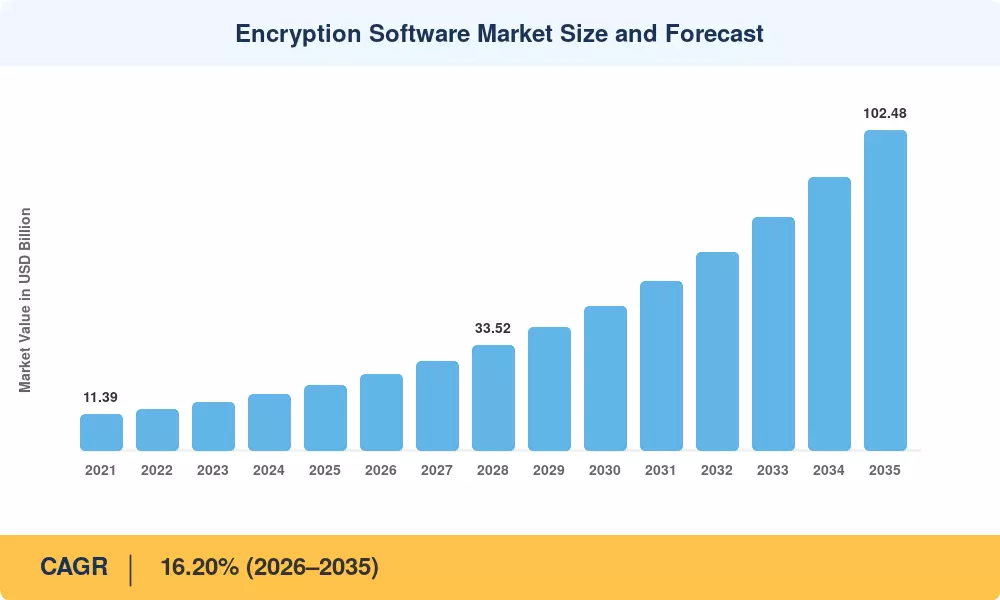

The Encryption Software Market reached USD 20.76 billion in 2025 and is projected to grow from USD 24.39 billion in 2026 to USD 102.48 billion by 2035, registering a CAGR of 16.20% across the forecast window. Two catalysts are reshaping procurement cycles: the August 2024 release of NIST's first three post-quantum cryptography standards (FIPS 203, 204, and 205) and the accompanying 2035 federal deadline for quantum-resistant encryption migration, which together have converted planning-phase budgets into active spending commitments [1]. U.S. Executive Order 14028's zero-trust architecture mandate continues to channel enterprise security budgets toward AES-256 end-to-end data encryption and distributed key-management platforms.

A structural shift is underway as organizations retire legacy perimeter-focused defenses in favor of data-centric protection. File and disk encryption for enterprise data now sits at the center of zero-trust strategies, replacing standalone VPN tunnels and static firewall rules. MRFR estimates that global information-security spending surpassed USD 215 billion in 2024, and a growing share of that total flows into email and communication encryption solutions designed for hybrid workforces. Cloud-native deployment models are accelerating this transition, enabling enterprises to manage cryptographic keys across distributed environments without maintaining on-premise hardware.

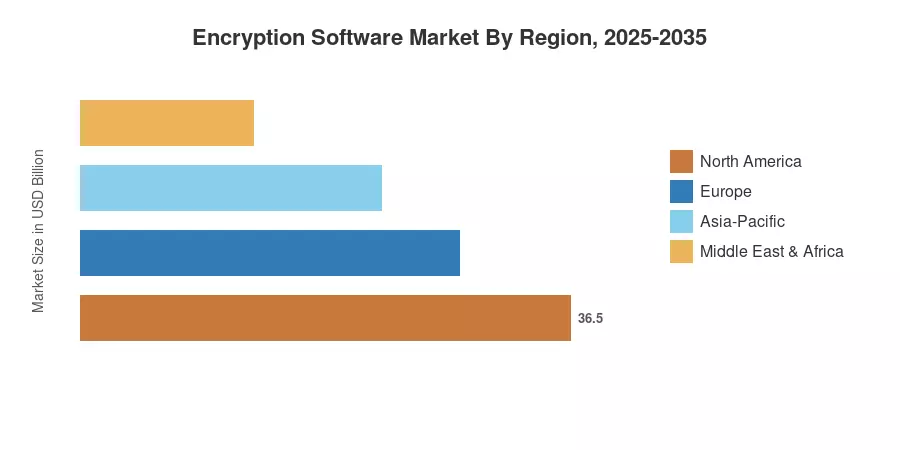

North America commanded roughly 45.60% of the global Encryption Software Market revenue in 2025, anchored by federal procurement cycles and a dense concentration of hyperscale cloud providers Asia-Pacific stands as the fastest-growing region at an estimated 21.30% CAGR, driven by India's Digital Personal Data Protection Act and China's expanding cybersecurity regulatory framework. Europe holds the second-largest share at approximately 26.80%, with the EU's NIS2 Directive pushing encryption adoption across critical-infrastructure operators. The Encryption Software Market trajectory points toward sustained double-digit expansion as quantum-resistant encryption algorithms move from pilot to production deployments over the next decade.

Key Report Takeaways

• By Component

- Software held the dominant share of the Encryption Software Market in 2025, accounting for roughly 61.20% of revenue

- Services are projected to expand at a 22.10% CAGR through 2035, driven by managed encryption and consulting engagements

• By Deployment Model

- On-premise deployment captured approximately 65.40% of the Encryption Software Market size in 2025

- Cloud deployment is advancing at a 25.80% CAGR, reflecting enterprise migration to SaaS-based encryption platforms

• By Function

- Disk encryption accounted for 35.10% of the Encryption Software Market in 2025

- Cloud encryption is growing fastest at a 28.70% CAGR as organizations embed cryptographic controls into multi-cloud architectures

• By Industry Vertical

- BFSI led with USD 6.45 billion in revenue during 2025, driven by PCI-DSS and SOX compliance mandates

- Healthcare is poised to grow at a 22.00% CAGR through 2035, fueled by HIPAA enforcement and telehealth expansion

• By Region

- North America captured the largest share of the Encryption Software Market in 2025

- Asia-Pacific is set to climb at a 21.30% CAGR, making it the fastest-growing region through 2035

Encryption Software Market Size and Forecast (2021–2035)

MRFR's sizing framework triangulates top-down revenue estimates from vendor filings with bottom-up license, subscription, and service tallies across 42 countries. Historical data (2021–2024) draws on audited annual reports and verified industry disclosures; forecast values (2026–2035) apply a compounded growth model calibrated to the 16.20% CAGR established through primary interviews and demand-side modeling.

.webp?v=1784639464)