Energy Retrofit Systems Market Summary

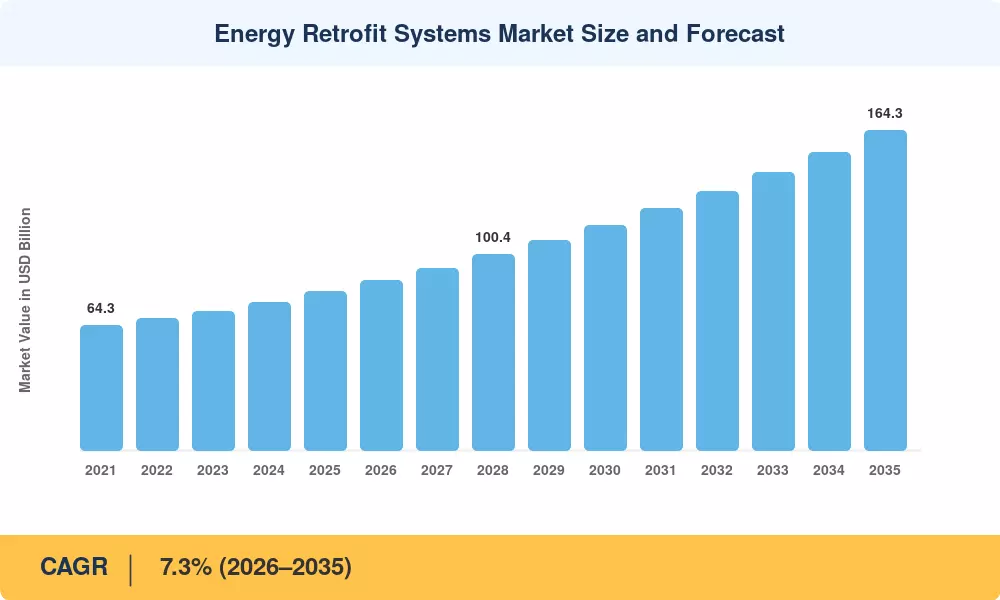

The global Energy Retrofit Systems Market reached an estimated USD 81.4 billion in 2025 and is projected to grow from USD 87.3 billion in 2026 to USD 164.3 billion by 2035, registering a CAGR of 7.3% during the forecast period (2026–2035). Buildings account for roughly 37% of global energy-related CO₂ emissions, and governments from the EU to the United States have responded with aggressive decarbonization mandates that funnel capital directly into retrofit activity [1]. The U.S. Inflation Reduction Act alone earmarked over USD 9 billion in rebates and tax credits for residential and commercial energy upgrades, creating a powerful demand catalyst for the Energy Retrofit Systems Market through 2032 [2].

Legacy heating systems, single-pane windows, outdated lighting, and inefficient building controls represent a global installed base worth trillions of dollars — and much of it is now being replaced. The European Union's Energy Performance of Buildings Directive (EPBD) recast in 2024 mandates that the worst-performing 15% of non-residential buildings undergo renovation by 2030, accelerating the transition from fossil-fuel boilers to heat pumps and from conventional lighting to intelligent LED arrays [3]. Private-sector energy service companies (ESCOs) have scaled their project pipelines by more than 22% year-over-year since 2022, deploying performance-based contracts that remove upfront cost barriers for building owners [4].

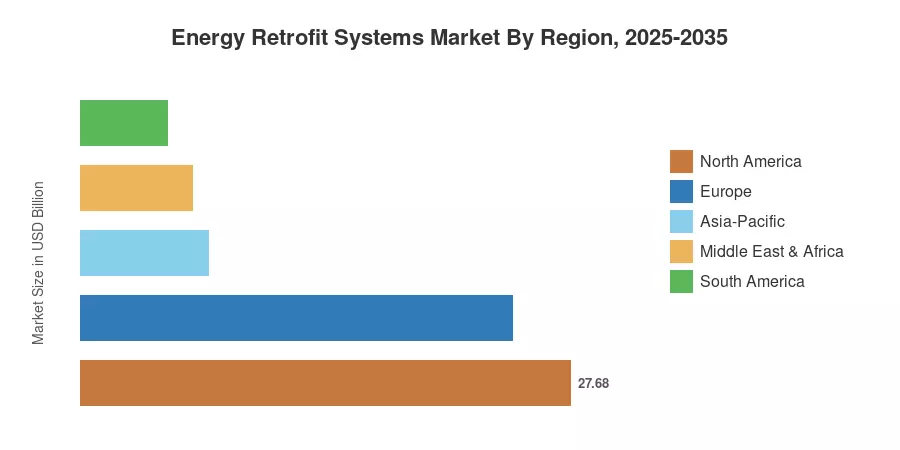

North America commands the largest share of the Energy Retrofit Systems Market at roughly 34% of global revenue, driven by federal incentive programs and stringent state-level building codes in California and New York. Asia-Pacific is the fastest-growing region with a projected CAGR of 8.9%, fueled by China's aggressive building energy efficiency targets and India's Energy Conservation Building Code updates [5]. Europe holds approximately 30% market share, anchored by the EU Renovation Wave strategy targeting 35 million building units by 2030 [6]. As aging building stock across all major economies approaches critical replacement thresholds, the retrofit value chain is poised for sustained double-digit investment growth in several sub-segments through 2035.

Key Report Takeaways

• By Technology

- HVAC system retrofits command the largest technology share at approximately 36% of the Energy Retrofit Systems Market, reflecting the global push to replace fossil-fuel heating with electric heat pump solutions.

- Building envelope upgrades — including insulation, fenestration, and air-sealing — are forecast to grow at a CAGR of 8.4% through 2035, the fastest rate among technology segments.

- Lighting retrofit solutions account for an estimated USD 12.8 billion in 2025 revenue, driven by commercial building conversions to networked LED systems.

• By Application

- Commercial buildings represent the dominant application segment in the Energy Retrofit Systems Market, holding approximately 42% revenue share in 2025.

- Residential retrofit activity is growing at a projected CAGR of 7.8%, supported by government rebate programs in North America and Europe.

- Industrial facility retrofits generated approximately USD 11.4 billion in 2025 as manufacturers pursue ISO 50001 energy management certification.

• By Region

- North America leads the Energy Retrofit Systems Market with a 34% share, anchored by U.S. federal tax credits and utility demand-side management programs.

- Asia-Pacific is forecast to reach a CAGR of 8.9% from 2026 to 2035, led by China, Japan, and India.

- Europe maintains the second-largest revenue share at 30%, underpinned by the EU's Renovation Wave and national building performance standards.

Energy Retrofit Systems Market Size and Forecast (2021–2035)

Market sizing combines bottom-up revenue aggregation across five technology verticals and four building-use categories with top-down cross-validation against IEA building-sector investment data and ESCO industry revenue disclosures. Historical figures (2021–2024) are derived from company filings, national energy agency reports, and trade-association databases. Forecast projections (2026–2035) apply a compound growth model calibrated to policy implementation timelines, technology cost curves, and regional building-stock age distributions [1][4][7].