ESG Software Market Summary

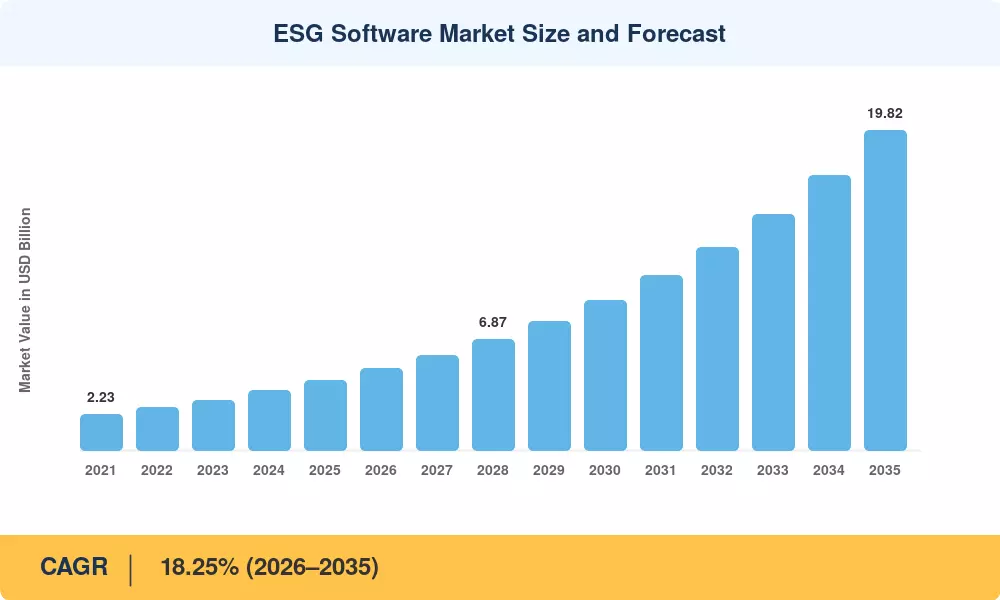

The ESG software market reached an estimated USD 4.36 billion in 2025 and is projected to climb from USD 5.10 billion in 2026 to USD 19.82 billion by 2035, registering an 18.25% CAGR during 2026–2035. Two catalysts dominate this acceleration: Europe's Corporate Sustainability Reporting Directive (CSRD), which now compels roughly 50,000 companies to file structured ESG disclosures [2], and the U.S. SEC's finalized climate-risk reporting rules that mandate Scope 1 and Scope 2 emissions data from public registrants [3]. These twin regulatory forces have turned ESG data collection and reporting platforms from a "nice-to-have" into a compliance imperative for multinational enterprises.

Technology transformation is reshaping the ESG software market at its core. Legacy spreadsheet-based sustainability tracking — still used by an estimated 40% of mid-cap firms as recently as 2023 — is giving way to cloud-native carbon accounting software and AI-driven sustainability performance dashboards that automate data ingestion from hundreds of operational sources [4]. Global ESG-related investment topped USD 35 trillion in 2024 according to the Global Sustainable Investment Alliance, pressuring portfolio managers to adopt ESG rating and benchmark tracking tools capable of real-time scoring across thousands of holdings [5].

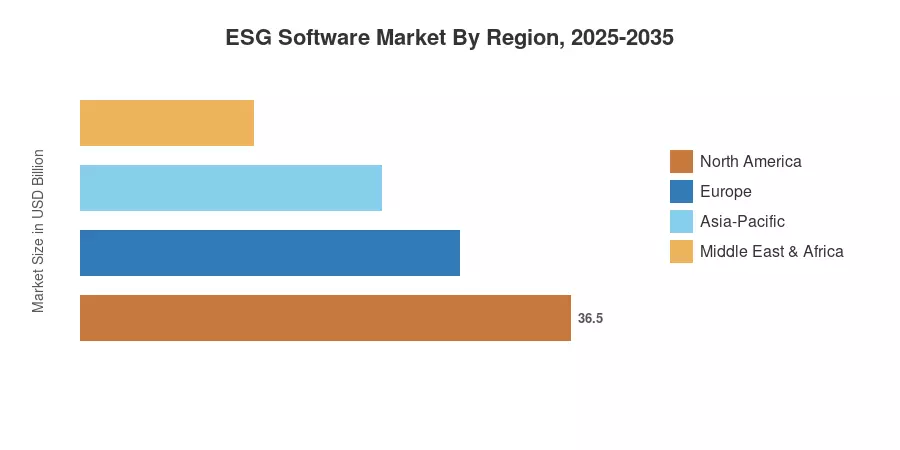

Europe commanded the largest share of the ESG software market in 2025, holding approximately 37.2% of global revenue, driven by CSRD timelines and the EU Taxonomy Regulation. Asia-Pacific is the fastest-growing region at a projected 23.1% CAGR through 2035, fueled by mandatory ESG disclosure frameworks rolling out across India, Japan, and South Korea North America held the second-largest share at roughly 31.5%, anchored by SEC mandates and voluntary state-level carbon reporting programs. As regulatory convergence tightens globally, the ESG software market stands to benefit from a multi-year adoption wave that extends well beyond traditional financial services into manufacturing, energy, and healthcare verticals.

Key Report Takeaways

• By Offering

- Solutions captured 72.8% of the ESG software market revenue in 2025, reflecting enterprise preference for integrated GRI and SASB compliance reporting software over standalone consulting engagements

- Services are forecast to expand at a 19.5% CAGR through 2035 as demand for implementation, training, and managed ESG reporting accelerates among mid-market firms

• By Deployment

- Cloud deployment accounted for 80.2% of the ESG software market share in 2025, benefiting from lower upfront costs and faster time-to-value for carbon accounting software rollouts

- Hybrid deployment models are poised to grow at a 21.4% CAGR to 2035, appealing to regulated industries that require on-premise data residency alongside cloud analytics

• By End-User Industry

- Banking & financial services led the ESG software market with 26.2% share in 2025, driven by ESG rating and benchmark tracking tools required for portfolio compliance

- Energy & utilities will post the fastest segment CAGR of 21.5% through 2035 as carbon accounting software adoption accelerates under emission-reduction mandates

• By Region

- Europe dominated with 37.2% of ESG software market revenue in 2025

- Asia-Pacific is advancing at a 23.1% CAGR between 2026 and 2035, the fastest regional growth rate

MRFR's market sizing integrates bottom-up revenue analysis from vendor financial disclosures, top-down macroeconomic modeling using regulatory adoption curves, and primary interviews with 120+ enterprise buyers and channel partners. All forecast projections apply a compound annual growth methodology calibrated against historical adoption trends and planned regulatory milestones.

.webp?v=1782888033)