Eyewear Market Summary

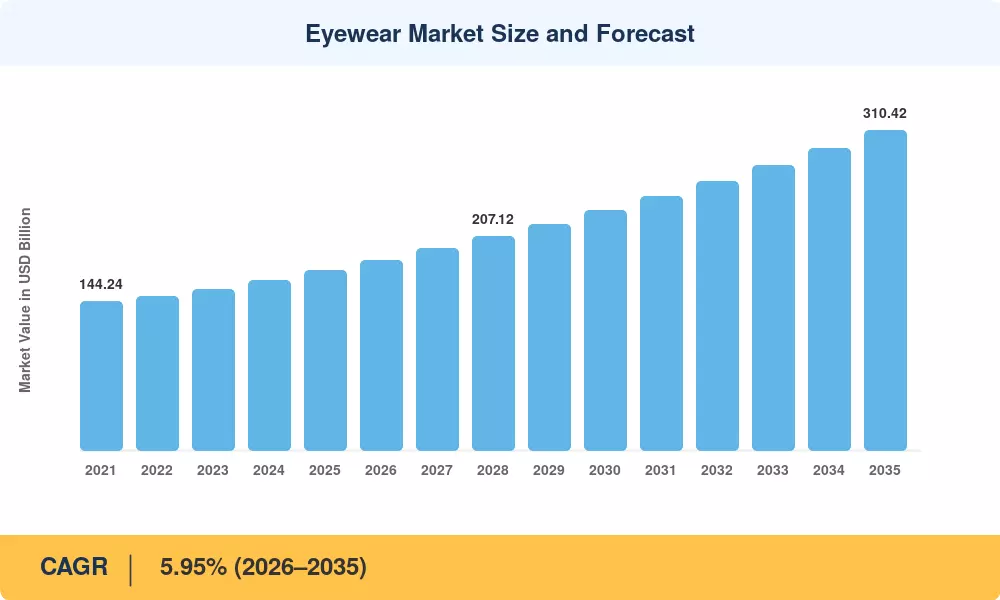

The global Eyewear Market reached an estimated USD 174.15 billion in 2025 and is projected to expand from USD 184.51 billion in 2026 to USD 310.42 billion by 2035, registering a CAGR of 5.95% during the forecast period. This growth is anchored in a convergence of clinical need and consumer preference — the World Health Organization estimates that over 2.2 billion people globally live with some form of vision impairment, and national health programs in countries like India (Rashtriya Netra Jyoti Yojana) and China have accelerated subsidized corrective lens distribution [1]. Workplace safety mandates in the EU and North America, which increasingly require protective and screen-optimized eyewear, are adding a regulatory tailwind to an already strong demand base [2].

The eyewear market is witnessing a technology-led change that is changing production and retail. “Advanced polymer and photochromic materials are displacing traditional glass-based lenses, while 3D-printed frames and AI-based virtual try-on platforms are reducing design-to-shelf lead times. EssilorLuxottica also committed over EUR 700 million in R&D in 2024, focused on smart lens integration and individualized vision solutions [3]. The Ray-Ban Meta cooperation highlights the way wearables are blurring the lines between functional eyeglasses and consumer electronics, bringing up brand new revenue sources.

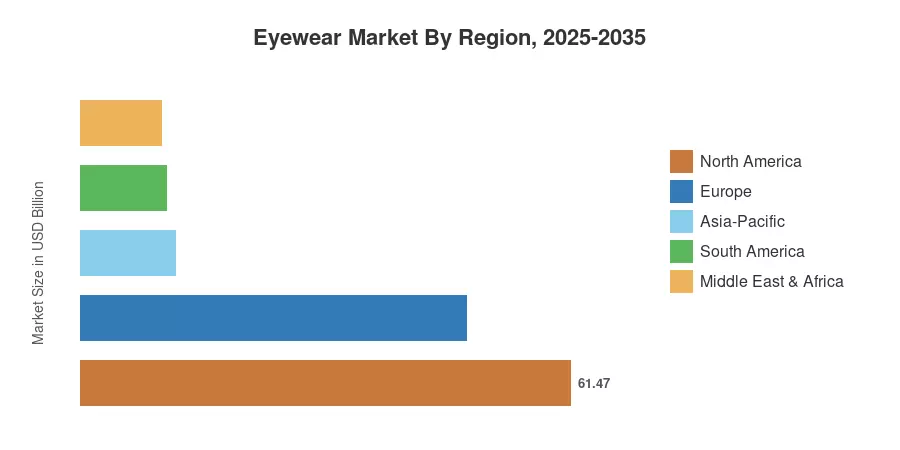

High per-capita spending and insurance-covered vision care are predicted to boost the North American eyewear market at 35.3% in 2025. Asia-Pacific is expected to be the fastest-growing area with a CAGR of around 6.8% till 2035. Factors such as the increasing prevalence of myopia among school age population and the growing organized retail would drive the growth. Europe is the second largest market with a share of roughly 27.8%. The region has a high demand for luxury eyeglasses in countries such as France, Italy and Germany. Digital screen penetration across all demographics continues to grow, providing a decade of stable growth for the Eyewear Market.

Key Report Takeaways

• By Product Type

- Spectacles accounted for approximately 70.8% of Eyewear Market revenue in 2025, reinforced by rising refractive error diagnoses and aging populations across developed economies.

- Sunglasses are expected to expand at a CAGR of 7.18% through 2035, driven by UV-awareness campaigns and fashion-driven replacement cycles.

• By Category

- The mass segment represented around 72.2% of the Eyewear Market in 2025, underpinned by affordable optical chains and government-subsidized vision programs in emerging economies.

- Premium eyewear is projected to grow at a 6.54% CAGR to 2035 as luxury branding and designer collaborations attract younger consumers.

• By End User

- Unisex frames captured an estimated 44.5% of Eyewear Market share in 2025, reflecting gender-neutral design trends.

- Women's eyewear is advancing at a CAGR of 6.29% through 2035, propelled by social media influence and expanding product assortments.

• By Distribution Channel

- Offline stores represented approximately 77.3% of Eyewear Market sales in 2025, anchored by the need for in-person fitting and prescription verification.

- Online channels are forecast to post a CAGR of 7.33% to 2035, accelerated by virtual try-on technology and direct-to-consumer brands.

• By Geography

- North America led the Eyewear Market with a 35.3% revenue share in 2025, backed by robust vision insurance coverage.

- Asia-Pacific is poised for the fastest expansion, driven by surging myopia prevalence and rising disposable incomes across China, India, and Southeast Asia.

Eyewear Market Size and Forecast (2021–2035)

MRFR’s size technique is a combination of bottom-up and top-down approaches that includes the use of optometry rates, retail sell-through data, and trade statistics cross-validated with top-down macroeconomic factors and company-reported revenues. Historical numbers (2021–2024) are sourced from audited financials and customs data; future values (2026–2035) use a calibrated CAGR with adjustments for projected regulatory and demographic developments.