Sunglasses Market Summary

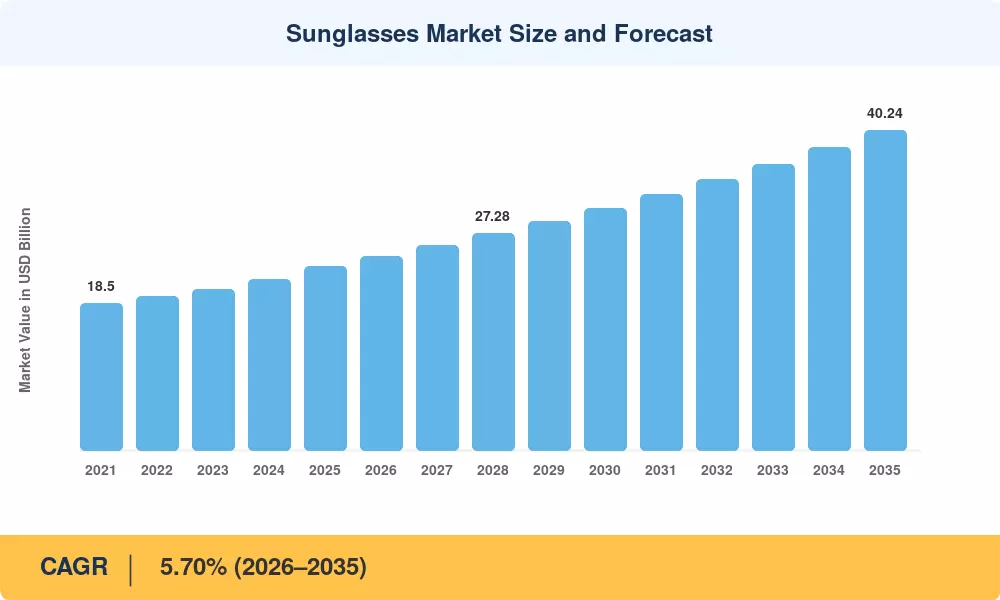

The global Sunglasses Market reached an estimated USD 23.10 Billion in 2025, driven by a convergence of rising health awareness, fashion-forward consumer behavior, and expanding retail digitization. Entering the forecast window at USD 24.42 Billion in 2026, the Sunglasses Market is projected to climb to USD 40.24 Billion by 2035, registering a CAGR of 5.70% across the period. Growing awareness around ultraviolet radiation risks — reinforced by dermatology associations and public-health campaigns in over 40 countries — has elevated sunglasses from a seasonal accessory to a year-round wellness essential [1]. Government-backed eye-health programs in India, Brazil, and several ASEAN nations have further expanded addressable demand among first-time buyers.

A technology transformation is reshaping the Sunglasses Market from the lens outward. Legacy CR-39 polymer lenses are steadily giving way to advanced photochromic, electrochromic, and blue-light-filtering substrates. EssilorLuxottica's USD 150 million R&D commitment through 2027 signals the scale of investment flowing into smart eyewear platforms that pair audio, heads-up display, and adaptive tinting into a single frame [2]. Bio-based acetate and recycled ocean-plastic frames have moved beyond niche positioning; leading producers now allocate 12–18% of new SKUs to sustainable materials, responding to EU Ecodesign Directive extensions expected to cover eyewear accessories by 2028 [3].

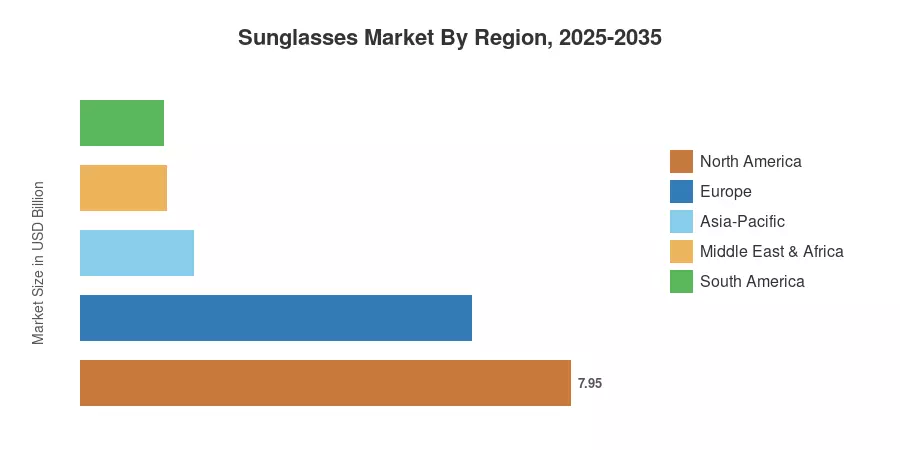

North America commands approximately 34.4% of the global Sunglasses Market, anchored by high per-capita spending and a mature optician-retail network across the United States and Canada. Asia-Pacific is the fastest-growing region with a projected 7.98% CAGR, fueled by middle-class expansion in China and India. Europe holds the second-largest share at roughly 27.5%, supported by luxury-house brand portfolios and strong tourism-driven seasonal demand. As premiumization accelerates and digital channels gain share, the Sunglasses Market is poised for sustained double-digit revenue gains in several emerging corridors through 2035.

Key Report Takeaways

• By Product Type

- Polarized sunglasses captured approximately 75.4% of the Sunglasses Market in 2025, reflecting consumer preference for glare reduction in driving and outdoor recreation segments.

- Non-polarized variants are forecast to expand at a 7.15% CAGR through 2035, propelled by fashion-oriented buyers prioritizing style versatility over technical lens performance.

• By End User

- Women represented an estimated 57.2% of the Sunglasses Market in 2025, driven by higher purchase frequency and broader style repertoires across mass and premium tiers.

- The kids segment is on track to register a 6.72% CAGR through 2035, supported by pediatric eye-care awareness and character-licensed collections from major brand houses.

• By Region

- North America led the Sunglasses Market with a 34.4% revenue share in 2025, underpinned by strong retail infrastructure and high brand penetration.

- Asia-Pacific is projected to grow at a 7.98% CAGR through 2035, driven by urbanization, rising disposable incomes, and an expanding e-commerce ecosystem across China, India, and Southeast Asia.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining top-down revenue modeling from manufacturer filings, bottom-up unit-volume analysis from distributor and retail-channel data, and demand-side calibration through consumer surveys across 25 countries. Historical figures reflect actual shipment and sell-through data; forecast values apply the calibrated 5.70% CAGR with adjustments for macroeconomic, regulatory, and technology-adoption variables.

.webp?v=1784721199)