Fast Food Market Summary

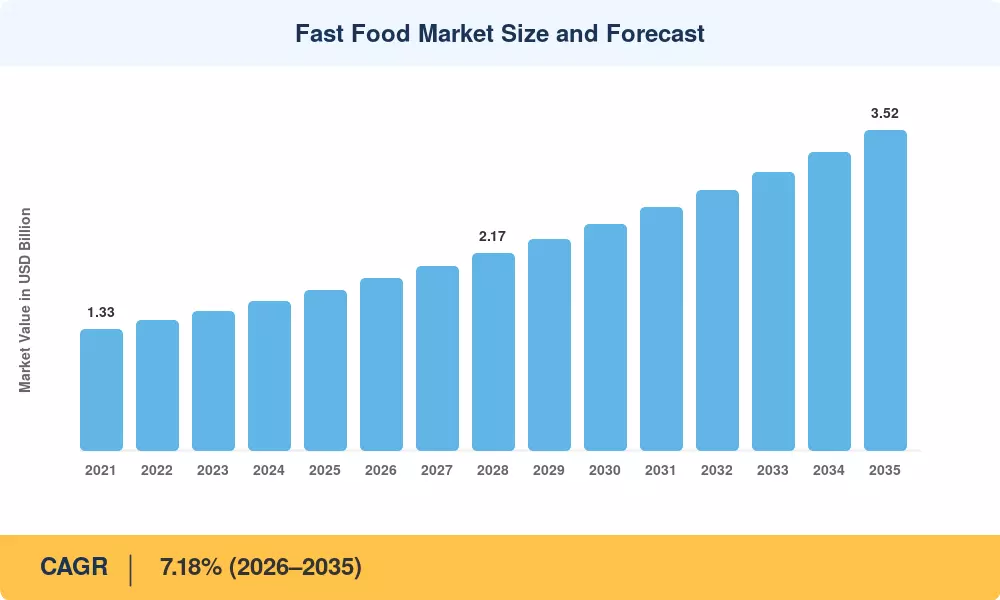

The fast food market reached an estimated USD 1.76 trillion in 2025 and is projected to grow from USD 1.90 trillion in 2026 to approximately USD 3.52 trillion by 2035, registering a CAGR of 7.18% during the forecast period (2026–2035). Rising urbanization rates, dual-income household growth across emerging economies, and an expanding middle class in Asia and Latin America are injecting sustained demand into the fast food market. Governments in several nations have relaxed FDI caps on food-service retail — India's 100% FDI allowance under the automatic route for single-brand food retailers, for example, creating a policy tailwind for quick service restaurants and burger and fried chicken chains looking to scale internationally [2].

A technology-led transformation is reshaping the fast food market at every node of the value chain. Legacy point-of-sale terminals and manual inventory systems are giving way to AI-powered order-taking kiosks, predictive supply-chain algorithms, and cloud-based kitchen management platforms. McDonald's alone committed over USD 300 million between 2023 and 2025 to digital drive-through food service upgrades, including automated order confirmation displays and dynamic menu pricing engines [3]. These investments are compressing average service times below three minutes in high-performing drive-through food service locations, reinforcing why the fast food franchise industry continues to attract franchisee capital.

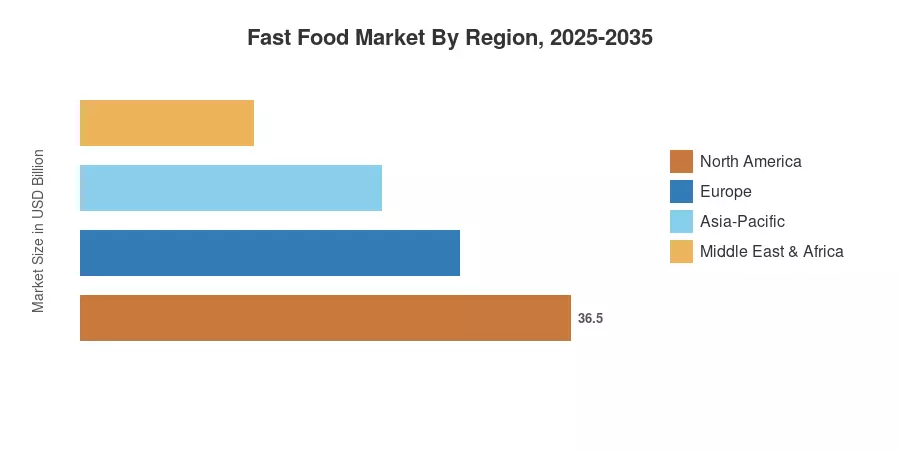

Asia-Pacific commands the largest share of the fast food market at roughly 46.5% of 2025 revenue, driven by China's USD 450 billion-plus food-delivery ecosystem and India's rapidly formalizing street-food sector. The Middle East & Africa region is the fastest-growing corridor, posting a projected CAGR of 9.52% through 2035, fueled by youth demographics and Saudi Arabia's Vision 2030 hospitality investment pipeline. North America remains the second-largest region, contributing around 24% of global revenue, anchored by the dominance of burger and fried chicken chains and a mature fast casual dining chains segment that continues to siphon share from legacy quick service restaurants

Key Report Takeaways

• By Product Type

- Burgers and sandwiches accounted for 41.2% of global fast food market revenue in 2025, driven by deeply entrenched consumer habits in North America and expanding burger and fried chicken chains in Asia

- Pizza is projected to advance at an 8.72% CAGR through 2035, leveraging digital ordering dominance and delivery-first operating models favored by fast casual dining chains

• By Restaurant Format

- Quick service restaurants captured 61.8% of the fast food market in 2025, benefiting from standardized operations and high unit throughput at drive-through food service windows

- Fast-casual formats are growing at an 8.78% CAGR through 2035, reflecting consumer willingness to pay a premium for fresher ingredients within the fast food franchise industry

• By Region

- Asia-Pacific generated USD 818 billion in fast food market revenue in 2025, led by China's platform-driven food delivery infrastructure

- The Middle East & Africa corridor is on track for a 9.52% CAGR through 2035, the fastest across all regions

Fast Food Market Size and Forecast (2021–2035)

MRFR's proprietary sizing model combines top-down revenue data from publicly listed quick service restaurants and fast casual dining chains with bottom-up store-count and average-ticket modeling across 45 countries. Third-party validation sources include Euromonitor, national statistics bureaus, and company annual filings.